We expect money transfers between buyers and sellers to take days, not minutes. But is that reasonable in a world where so much of what we do is instant?

When we can get customer support, social media updates, responses, or communications within moments of our requests, why do payments take so long? Fortunately, this could be about to change. There’s increasing interest in fintech to move towards faster payment processing, perhaps even to get to the holy grail of “instant payments.” Let’s take a look at the current state of the instant payment trend.

- NACHA and Same Day ACH Payments

- Drivers Behind Instant Payments

- Traditional Banks vs. Other Payment Providers

- Benefits of Moving to Instant Payment Systems

- Challenges of Moving to Instant Payment Systems

NACHA and Same Day ACH Payments

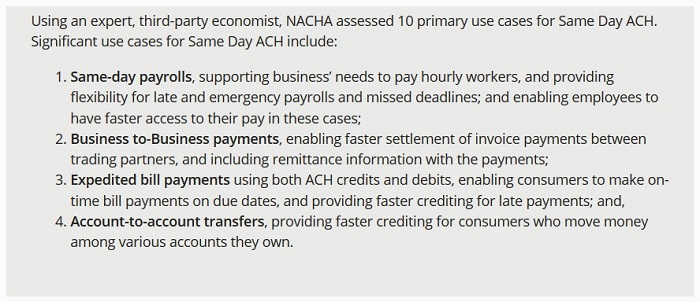

Instant payments are closer than ever, and “same-day ACH” has been paving the way. From September 2016, NACHA — The Electronic Payments Association – had adopted a new rule to allow same-day Automated Clearing House (ACH) payments. ACH transactions are very similar to direct debits and bank drafts, allowing for transfer of money between different bank accounts.

Typically, most ACH payments are settled on the next business day, but NACHA has recognized that some vendors and consumers want payments processed more quickly. The change they have introduced means that organizations can opt-in to same day ACH processing, levying a small fee to cover the ACH fast processing costs.

Same day ACH transactions will settle within two hours and make funds available the same day. This will be very beneficial for payroll, bill payments, and B2B payments.

Drivers Behind Instant Payments

There are several major reasons for why the finance industry is getting more interested in instant payments, including demand (both consumer and vendor), possibilities for risk reduction through advanced security tools, and more.

Consumer Demand

Customers want to get services and make payments immediately. If they request money from others, they expect it in the same timescales as being handed a ten dollar bill, i.e. right away. Once they pay for products and services, they want them immediately. Providing instant payments is one way to increase customer satisfaction. However, as mentioned later in this article, consumers may be unwilling to opt for instant payment services if there’s a cost associated.

Vendor, Merchant, and Supplier Demand

Suppliers want certainty around payments. If they are going to release goods and services, there’s a clear assumption they will be paid. Faster payments to suppliers frees up the flow of money through the system. With instant payments, vendors wouldn’t have to worry about waiting for a payment to clear before they ship goods to the purchaser. Businesses may be more willing to pay a little extra for instant payments.

Instant Payments Necessitates Risk Reduction

Together with increasing value for customers and offering attractive instant payment services, this new trend demands greater security and more fraud prevention. The traditional ACH, bank draft, or card payment is based on finance technology that can be years out of date. Just as physical infrastructure needs to be enhanced for the safety of people who use the roads, so financial infrastructure should be optimized to enhance accuracy, reduce fraud, and serve the consumers and banks better. Instant payments are one of the incentives to do that. Additionally, regulatory bodies have long wanted to see modernization of the payment system’s legacy infrastructure, so are embracing the idea of instant payments.

That’s ultimately better for everyone and reduces overall risk in the payment system as all parties implement tools to manage the risks.

However, this only works if fraud tools are actively developed and used by businesses; sluggish adoption of some anti-fraud tools, like 3D Secure, indicate that instant payments may come with just as many risks.

Read more about 3D Secure anti-fraud tools.

Traditional Banks vs. Other Payment Providers

Traditionally, the banks and card networks have held all the power when it comes to payments. That’s all changing — the rise of apps like Venmo or cryptocurrency like Bitcoin demonstrates that other considerations like speed and privacy are as important to some consumers as accuracy and security. In 25 countries around the world, many banks already offer almost immediate ACH transfers, bank drafts, and direct debits.

Now, American banks are being forced to play catch up. They want to retain dominance in the financial world, so they have to offer the same convenience, quality, accuracy, and speed that consumers are demanding whenever they interact with businesses.

In the UK, introducing a “faster payments” system has led to a significant reduction in check usage and a big increase in the adoption of non-cash payments.

Encouraging Free Market Competition and Reducing Monopolies

Along those lines, the possibility of instant payments could provide fintech companies with the opportunity to disrupt the traditional banking industry. Regulators have a desire to see a level playing field where new businesses can compete effectively with the entrenched, traditional banks.

One Option — US Banks Using a Third-Party Instant Payments System

To start, the banks are taking baby steps and choosing to integrate with existing services. Many of the big banks are offering instant payments through the Zelle instant payments network. It’s a service that will integrate with the bank’s online account management portals or mobile apps, letting consumers quickly transfer money between accounts.

Of course, it’s vital to do this with minimal disruption. The 20 banks initially offering this service have over 100 million customers between them. Zelle has to work well alongside traditional ACH and bank draft options, together with other ways consumers move their money around. Zelle also offers other features to get consumers on board with instant payments; for example, the ability to split bills and send requests to other Zelle users makes it similar to one of Venmo’s main use cases.

A Second Option — US Banks Developing Fast Payment Technologies Themselves

It’s not just third-party providers offering faster payment options. JPMorgan introduced a “Quick Pay” option that integrates with Zelle. Adoption has been rapid, too, with over $7 billion sent through the platform in Q3 2016, up 36% on the previous year.

Benefits of Moving to Instant Payments Systems

Aside from speed, what benefits can banks, consumers, and others expect from a move towards an instant payments system?

- Customer and supplier satisfaction — having more money in accounts makes everyone happier.

- Freeing up cash flow — more available funds in the system means greater transfer of money between parties, meaning more liquidity.

- Non-reversible transactions — once payments are made, they are final, reducing the risk of refund, chargeback, or fraud. (Note that this is not necessarily the case with all instant payments.)

- New business opportunities — startups and established fintech businesses can take advantage and create new product and service offerings.

- Broader market appeal — as consumer demands increase, they are likely to gravitate towards providers who offer faster payments.

- Revenue stream — if instant payments are offered as a premium service, this provides new revenue streams to businesses offering these services.

Challenges of Moving to Instant Payments Systems

Although there’s a strong drive and desire for instant payments, evolution can have downsides. When moving to an instant payments system, it’s important to consider key factors. Will customers will pay for it? Is the investment is worth it? How will systems work together? Can it be made secure?

Will Consumers Want to Pay?

It’s likely that instant payments will be a premium service. There’s no clear indication that consumers will want to pay for that privilege. Suppliers or businesses may be willing to pay a small premium to get their money faster. This is the case with Square’s instant deposit.

The company charges an additional 1% of the transaction for the option to have funds deposited immediately instead of waiting the 1-2 business days most card transactions take. Some businesses feel this extra fee is worthwhile.

Is the Investment Cost Worth It?

The banks will need to pay the cost and make an investment in faster infrastructure, and that cost is likely to be significant. Is there a good business case for investing that money if there’s not a clear way to recoup it? The implementation will be challenging. Tthe instant payments system will need to integrate with and work alongside traditional payment systems.

Will Faster Systems Work with Other Payment Systems and Countries?

Instant payment systems will need to work with other payment infrastructure and across international borders. Standardization will be a necessary part of delivering instant payments in an increasingly global financial system. But standardization isn’t always a given, and there’s no reason to think that it would come automatically with instant payments.

Can Banks Provide Fast, Secure Risk Reduction and Fraud Prevention Technologies?

Fraud already costs banks, businesses, and card processors dearly. Alongside instant payments, there needs to be more investment in robust fraud detection capabilities to reduce risks to banks, consumers, and businesses. However, many businesses don’t take advantage of all the existing anti-fraud tools, and it’s likely that trend would continue with instant payments.

It’s a Case of “When” Not “If” for Instant Payments

Despite the possible drawbacks, the impetus behind instant payments is already here. Over the next few years we’ll see adoption across the whole financial industry. Instant payments are a huge technical challenge, but the drivers behind them and the desire for everything to move faster makes the adoption almost inevitable.