Some of the hidden costs of taking credit and debit card payments are fraud and chargebacks — areas where a card is used in a criminal way, or where a customer disputes a transaction. Left unchecked, these can be very expensive for retailers and merchants, with $8 billion in money lost to credit card fraud in 2016.

Left unchecked, these can be very expensive for retailers and merchants, with billions lost to card fraud every year.

The minFraud service from MAXMIND aims to reduce or eliminate these risks and costs. It uses data points from over a billion transactions to create a risk score for any cards you’re processing. It can then combine that risk score with rules and thresholds you set so you can automatically decide whether to accept or reject a particular transaction.

We’ll explore how the service works, what you can do with it, pricing, and more to help you decide if it’s a useful addition for your transaction monitoring and credit card processing.

Background: Understanding Chargebacks.

MinFraud Services in its Own Words

“Reduce chargebacks and increase profitability with real-time fraud analysis. The minFraud service provides real-time fraud analysis, post-query alerts, and data points to inform manual review and custom rule creation.”

Examining MinFraud’s Services

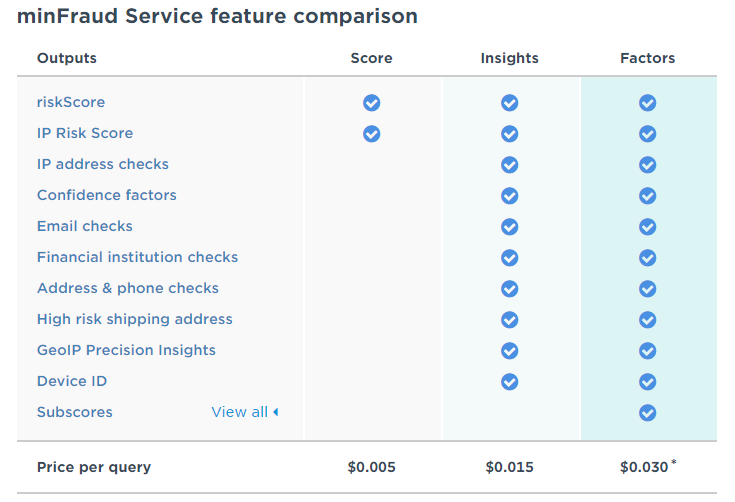

MinFraud provides a number of closely related services, called MinFraud Score, Insights, and Factors.

MinFraud Score

Firstly, the minFraud Score provides an overall risk score for every transaction you process. It uses two key features to provide this — a “transaction risk assessment” and an “IP address risk.” This score can then feed into your credit card and transaction processing rules so you can accept or reject each transaction, based on likely risk.

MinFraud Insights

This service expands on the overall risk score by providing analysis and broader understanding of the key factors minFraud uses to create that score. minFraud Insights gives you more detail for each transaction including geolocation, IP and email risk assessment, and Issuer Identification Number (IIN) checks.

MinFraud Factors

MinFraud Factors provides deeper insight into all the subscores that contribute to the overall risk score. These contributing factors help you to understand how risk scores are calculated and can feed into your overall acceptance / rejection rules. For example, you could find out if a transaction was rejected due to unusual activity on a card, issues with the IP address, or an email address associated with previous fraudulent activity. minFraud Factors also provides access to minFraud insights.

MAXMIND offers a comparison chart showing the differences between the services and what features are included with each:

Key Benefits

The main benefits minFraud provides are:

- Significantly reduce or eliminate the number of fraudulent transactions your business processes.

- Significantly reduce or eliminate chargebacks from customers (e.g. if they have been the victim of identity theft and their card has been used in a criminal way).

MinFraud works quickly and invisible behind the scenes. It does not slow down transaction processing, and won’t be noticed by the end user. The service can work by itself or alongside other fraud detection and prevention systems and allows for simple or complex rules in place to accept or reject transactions automatically. MinFraud reduces the time and resources manually reviewing questionable transactions.

How It Works

MinFraud uses a combination of data points across over a billion transactions to provide an accurate risk score for every credit or debit card payment you process. Several variables go into the assessment and scoring, including geolocation, IIN information, reputation checks, IP checks, and device tracking.

Geolocation

Geolocation refers to checking the location of card use against the IP address of the user’s device to identify suspicious pairings. This includes finding high-risk countries and issues with billing, shipping, and IP address locations.

IIN Information

IIN involves checking that the issue identification number (IIN) on a card is valid. MinFraud can find issues between card information provided by the user and the issuer identification data on file.

Reputation Checks

MinFraud’s reputation checks involve identifying previous fraudulent or questionable use for email addresses, street addresses, devices, phone numbers, and more. This lets minFraud find transactions associated with higher risk devices or email addresses.

High-Risk IP Addresses and Proxies

MinFraud is able to identify IP addresses and ranges associated with fraudulent transactions, including users who rely on proxy networks. This includes identifying high-risk IPs, virtual private networks (VPNs), anonymizers, and compromised devices.

Device Tracking

MinFraud tracks individual devices and builds up a transaction history for each one, so if a device has been associated with a fraudulent transaction before, it will naturally get a much higher risk score.

Automatic Rules, Reviews, and Fraud Avoidance

MAXMIND’s minFraud system offers a number of customizable options like automatic rules that can accept or reject transactions based on the rule criteria. The fully featured API will provide information back to your credit card processing systems, and based on the risk score, you can set up rules designed to reject high-risk transactions, accept low-risk ones, and flag others for manual review. This reduces the resources you need to devote to manually analyzing transactions.

Identifying Different Types of Fraud

In addition to identifying “standard” fraud, where a user makes payment with a stolen, cloned, or otherwise compromised card, minFraud can help in other ways. You can also track transactions sent through affiliate marketing to identify and reduce affiliate fraud. You can combine the risk score with shopping cart transaction values to identify high-value transactions, and you can track gift purchases to deal with “triangulation fraud.”

The minFraud API

Transactions are analyzed by minFraud and provided back to your card processing rules and payments using minFraud’s API. The minFraud API is available in several programming languages including .NET, C#, Java, Perl, PHP, and Python. Additionally, minFraud provides complete support documentation for developers on exactly how to integrate their services with your payment acceptance processes.

MinFraud Pricing

As far as costs, MinFraud operates on a “pay as you go” model, charging a small fee for each transaction it analyzes. You buy minFraud credits of between $25 and $250 at a time. MinFraud then charges a fee for every query the API returns. These fees vary depending on the minFraud service you use, as follows:

Score — $0.005 per query.

Insights — $0.015 per query.

Factors — $0.02 per query.

That means that if you process 10,000 transactions per month, you could expect to pay $50 for Score, $150 for Insights, or $300 for Factors.

These costs are on top of your credit card processing rates and fees, which MAXMIND does not set.

Is minFraud Right for Your Business?

If chargebacks and fraud are causing issues for your business, minFraud is a comprehensive, low-cost way to identify and reject suspicious transactions. You will need a developer to integrate minFraud into your credit card rules and processing. However, it may be an effective way of reducing or eliminating fraudulent transactions, saving you money, time, and anxiety.

See also: Choosing a Chargeback Management Company.