Several recent lawsuits have put the spotlight on a whole series of alleged schemes by processors to collect junk charges disguised as legitimate fees.

Update: 1/3/2020

I originally wrote about Worldpay’s questionable practice described in the article below back in May of 2019. Then, I spent a good deal of time helping the folks at Reuters understand what was happening in order to expose the deceptive billing tactic. Reuters published its article on the topic in August of 2019. I wish the article had more of a bite, and I’m not thrilled about being referred to as someone “who writes about the industry and makes money selling processing services for selected Worldpay competitors,” but I’ll bear the label in the interest of advancing the greater good.

The article from Reuters did cause Worldpay to make a couple subtle changes on its billing statement. It’s not much, but Worldpay now alludes to the fact that the pricing shown is not actually interchange-plus.

As shown below, Worldpay changed the title of the fee section to “Interchange & Worldpay Surcharge,” and it added the following qualifying statement: The ‘Interchange & Worldpay Surcharge’ section is inclusive of interchange pass through as well as Worldpay non-qualified surcharge.

The original article begins here:

Wells Fargo is currently being sued for charging deceptive fees, North American Bancard is currently being sued for charging deceptive fees, Mercury Payments lost a lawsuit (with a $72.5 million payout) for charging deceptive fees, and Worldpay is being sued for similar allegations.

While the outcome of those lawsuits is beyond the scope of this post, CardFellow has paid attention to the alleged schemes as it relates to processing. In fact, after reviewing the details of the claims in these lawsuits, it appears that Worldpay, formerly Vantiv, is using similar hidden fees– only on a grander scale. Worldpay as the largest payment processor in the United States is actively engaging in behavior that’s very similar to that which other processors have been sued for in the past. The difference this time is there’s way more money involved. So much so that small businesses may be losing hundreds of millions of dollars in hidden fees. So far, the tactics seem to have gone unnoticed, but CardFellow can shed some light on what appears to be happening.

Here’s a General Overview

Every time a business accepts a credit card as payment for products or services it must pay a fee to a credit card processor. The fees are outlined in a contract the business signs with the processor.

The business owner expects that the processor will abide by the agreement when charging fees. Instead, there have been many instances alleged in lawsuits where a processor uses a specific type of pricing model to disguise significant additional charges.

With excessive charges shielded by opaque billing, even the savviest business people don’t notice the overage, so this dubious billing practice goes unnoticed.

The ability to have longevity with unnoticed fees combined with the sheer volume of income it generates make it an attractive profit center. So much so that profits likely far exceed any potential losses the processor would face if caught.

To support this point, I’ve listed current and past lawsuits below related to these various billing schemes, along with a summary of each complaint.

Legal Action Related to This Scheme

You’ll notice the processor Global Payments Direct is listed multiple times. It lost one lawsuit, but allegedly engaged in the same scheme again and is now the plaintiff in the most recent lawsuit. This supports the assumption that even when a processor loses in court, it still makes a profit after paying losses.

- Champs Sports Bar & Grill Co. et al v. Mercury Payment Systems, LLC and Global Payments Direct, Inc.

“Defendants were inflating the fees that should have been passed through at cost and collecting other unauthorized charges.”

- The final Settlement has a value of $72.5 million

- Patti’s Pitas, LLC et al v. Wells Fargo Merchant Services, LLC

“Defendant has assessed other fees in the guise of pass-through fees from the card networks which are actually retained by Defendant.” - S. KAO, Inc. d/b/a Lucky 7 Chinese Food et al v. North American Bancard, LLC and Global Payments Direct, Inc.

“Merchants that have been overcharged and billed for unauthorized junk fees and inflated assessments and access fees in contravention of the Merchant Service Agreement…”

How the Plaintiffs Allege the Scheme Works: The Basics

Essentially, processors leverage the complexity of processing fees to keep businesses in the dark as to how fees are charged, and what costs should really be. Then, in the confusion, the processor sneaks in additional charges, or in this case, simply overcharges for various fees.

Before we explain the intricacies of the scheme itself, we must first pull back the curtain by summarizing the fundamentals of processing fees.

Where the Money Goes

The fees a business pays to accept credit cards are divided into three separate components called interchange, assessments, and markup.

Interchange fees are collected by the bank that issues a customer’s credit card. Assessment fees are paid to the card brand (Visa, MasterCard, Discover) whose logo is on a customer’s credit card, and markup is paid to the business’s credit card processor.

The reason it’s important to conceptualize processing fees in terms of components is because not all components are negotiable. In fact, only the markup will – or should – differ among processors. As we’ll explain later, a key piece of Worldpay’s billing involves overcharging for interchange fees.

Wholesale

The interchange and assessment components of cost are processor-independent. Meaning, these fees are consistent regardless of the processor a business uses. For this reason, it’s helpful to think of interchange and assessments collectively as wholesale, or as a processor’s real cost.

Interchange Fees

Interchange fees are the most complex component of processing cost. There are a lot of them, and the amount of the fee changes based on the details of an individual transaction.

For example, if a business swipes or “dips” a Visa reward card, the interchange fee is calculated as 1.65% of the transaction amount, plus a flat $0.10 fee.

If an online business accepts a MasterCard World Elite card, the interchange fee is calculated as 2.50% of the transaction amount, plus a flat $0.10 fee.

If a business swipes or “dips” a debit card issued by a large bank, the interchange fee is calculated as 0.05% of the transaction amount, plus a flat $0.22 fee.

There are several hundred different interchange fee categories among all the card brands. Check out the Visa and MasterCard Web sites to see the current interchange tables and rates.

Overcharging Interchange – the Heart of the Hidden Fees

Processors don’t set the interchange rates and fees. The Visa rewards card noted above would cost 1.65% + $0.10 no matter which processor a business uses.

But that doesn’t mean processors don’t add to the interchange fee, padding it to increase their profit without disclosing it as a markup. I’ll come back to this after a look at what constitutes “processor markup.”

Markup

The markup is where the credit card processor makes its money. Since interchange and assessments comprise a processor’s cost, any revenue generated beyond this cost is the processor’s markup.

The closer a business pays to the base costs of interchange and assessments, the less money a processor makes as its markup. So, naturally, processors use various tactics to maximize markup. One of the most effective ways processors do this is by utilizing different pricing models.

Pricing Models

Processors use different pricing models to manipulate the way in which they bill the costs of interchange, assessments, and markup to businesses. Although there are multiple variations, pricing models fall into one of two categories: tiered or interchange plus.

Interchange-plus is regarded as the more competitive and transparent of the two pricing models, and it’s the one Worldpay is manipulating in its billing scheme.

Interchange Plus

Using the interchange-plus pricing model, a processor takes the actual interchange cost of a transaction and bills it directly to a business. Then, the processor applies one fixed percentage and one fixed transaction fee as its markup.

For example, a processor may bill a business interchange, plus 0.20% of sales volume, plus a flat $0.10 for each transaction. This means that the processor will pass along the real cost of interchange fees, plus the markup percentage and transaction fee.

Using an example from the Interchange Fees section above and the markup example in this section, let’s pretend a business accepts a Visa reward card as payment for services.

In this case, the processor would pass along the interchange fee of 1.65% of the transaction amount, plus a flat $0.10 fee. Then, the processor would bill an additional 0.20% of sales volume, plus a flat $0.10 as its markup.

As you can see, the processor’s markup remains independent of interchange, which is what enables the interchange-plus pricing model to be transparent.

For this reason, many business people have begun requesting the interchange-plus pricing model from processors. However, the average business person is not well versed in the intricacies of interchange, so they’re left to rely on the contract signed with a processor to guarantee interchange fees will be billed at true cost.

This is where Worldpay seems to have thrown out the rulebook: by not readily disclosing markups within charges that appear as the real cost of interchange.

Connecting the Dots: The Scheme in Action

The definition of interchange-plus pricing dictates that a processor bill the true cost of interchange separate from a fixed markup. Therefore, under this pricing model, a business person has no cause to assume that interchange will be inflated. But Worldpay seems to be doing exactly that.

Worldpay is representing to businesses that it will bill using interchange-plus pricing. However, it then inflates select interchange categories to significantly increase processing costs. This allows Worldpay’s pricing to appear competitive while it’s actually charging significantly more than many of its small business clients are likely to realize.

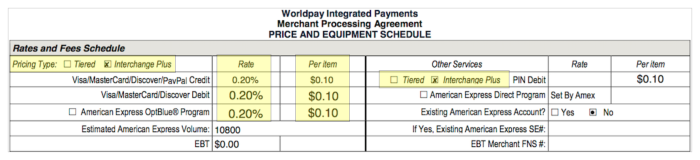

Below is a copy of a Worldpay processing agreement that clearly states the business will be charged 0.20% of sales volume, plus a transaction fee of $0.10, using an interchange-plus pricing model.

Below is a statement snippet from this same business showing the 0.20% of sales volume, plus a transaction fee of $0.10 being assessed.

To the average business person, this looks correct. The markup is being charged at 0.20% and $0.10, just as the agreement states.

But what about the interchange fees?

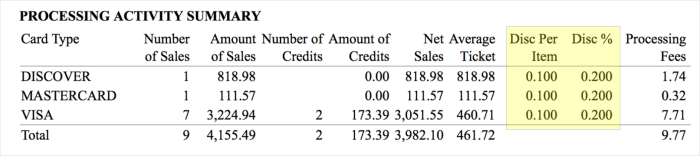

Below is a snippet from the same statement showing an itemized list of interchange charges the business incurred. The percentage and transaction fee for each interchange category are not disclosed on the statement. So, some knowledge of interchange and some quick math is necessary to determine if Worldpay billed interchange at real cost.

The table we’ve created below shows the real interchange rates, transaction fees, and cost for this business’s volume. What becomes clear is that Worldpay has undisclosed fees and appears to have applied a 0.40% markup that is not disclosed in the business’s contract.

| Actual Interchange Fees | |||||||

| Sales | # Trans. | Int. % | Int. $ | Total Interchange | Worldpay’s Fee | Over-Charge | |

| VS CPS E-Commerce Basic | $1,037.99 | 1 | 1.80% | $0.10 | $18.78 | $22.94 | 0.40% |

| VS CPS Rewards 2 | $1,003.97 | 2 | 1.95% | $0.10 | $19.78 | $23.80 | 0.40% |

| VS Signature Preferred CNP | $1,182.98 | 4 | 2.40% | $0.10 | $28.79 | $33.54 | 0.40% |

| MC Merit I | $111.57 | 1 | 1.89% | $0.10 | $2.21 | $2.66 | 0.40% |

| DS PSL E-commerce Rewards | $818.98 | 1 | 1.97% | $0.10 | $16.23 | $19.52 | 0.40% |

The interchange pricing we used to uncover Worldpay’s hidden charges comes directly from Visa’s and Mastercard’s published interchange tables. These fees are listed as “Int. %” and “Int. $” in the table above.

The sales figures and number of transactions come directly from the business’s statement, above.

The actual interchange cost is listed it in the “total interchange” column, and “Worldpay’s Fee” is taken from the statement above. As you can see, Worldpay appears to have charged more than the actual interchange cost, and there is nothing in the document that discloses it. Instead, it padded interchange to inflate charges, making its markup of 0.20% seem lower than it is. In reality, if there is no further explanation or detail, Worldpay appears to have charged this business a 0.60% markup, not the 0.20% markup outlined in the contract.

The Variations

This article shows Worldpay applying this undisclosed markup to all sales volume, but it’s not always that apparent. We have analyzed Worldpay statements showing this used selectively, where Worldpay pads some interchange categories and not others. The amount of the hidden charge also varies. We have statements showing the hidden markup ranging from 0.30% all the way up to 1.45%.

The Revenue

0.40% may not sound like a lot until you put the numbers into perspective.

Vantiv merged with Worldpay in 2017, making it the largest merchant acquirer, and has annual processing volume in excess of $1 trillion. At this point, there’s no way to tell how many businesses Worldpay is billing using interchange-plus, and of those, how many are being over-charged. But it doesn’t take much to make the numbers add up.

Let’s be conservative. For example, if Worldpay uses these hidden fees on just 10% of its clients and over-bills by the same 0.40% shown above, it would take in an additional $400,000,000 in annual revenue from its small business clients.

Enough is Enough

The sales pressure and general dissemination of erroneous information about processing keeps most people chasing their tails in the quest to secure a competitive, ethical processing solution.

For those that do make some headway in pushing back against abuse in the processing industry, processors simply come up with another way to rewrite the rules in their favor.

Even the legal system doesn’t seem to be a deterrent with all of these lawsuits and no changes. It’s simple economics. Why not make a few hundred million dollars fleecing small business when the only cost is a loss in the courts and a blow to an already poor reputation?

Processors fly under the radar and out of sight of public scrutiny, and as long as that happens, this nonsense will continue. Enough is enough.