What is Buy Now, Pay Later?

Buy Now, Pay Later or BNPL is any option for a customer to make a “purchase” and take possession of goods while agreeing to terms to pay at a future date, typically with several payments staggered across a specific time period. There are companies that offer BNPL options and facilitate the process for businesses. Afterpay is one such company.What is Afterpay?

Afterpay (now called Cash App Afterpay) is a Buy Now, Pay Later platform that allows your customers to make purchases online or in-store and pay for them in 4 installments or more. If the customer pays according to the terms, the installments are interest-free, making them an attractive option for customers. Typically, the payments are spread out over 6 weeks for the main "pay in 4" option, but there are also monthly repayment plans spread across 6-12 months. Afterpay is widely accepted by retailers in a variety of industries, including home goods, electronics, fashion, and more. It’s particularly appealing in industries with high average transaction amounts, as it makes the total purchase price seem more palatable to customers. As a BNPL platform, Afterpay offers instant approval to customers and does not require a “hard” credit check, which is helpful for customers with limited credit history. The company also boasts no hidden fees. As long as customers pay on time according to the terms, there is no interest. (There is a late fee if customers miss a payment.)How Afterpay Works for Consumers

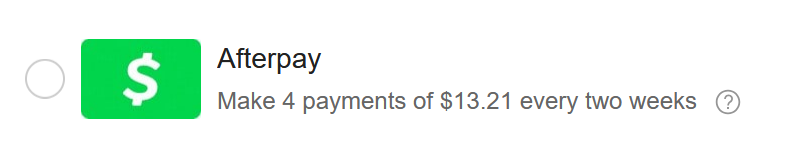

From a consumer’s perspective, the process is straightforward. When the consumer shops with a business that offers Afterpay, they can select it as their payment option at checkout. Above is an example of Afterpay as a choice from a range of payment options on an ecommerce site. It dynamically displays the amount of the installment payment based on the total of the items in my cart. (Note that some businesses may have a minimum purchase amount to be eligible for Afterpay or other BNPL purchases.)

Clicking the ? next to the Afterpay option brings up a page that explains more about the BNPL option.

Above is an example of Afterpay as a choice from a range of payment options on an ecommerce site. It dynamically displays the amount of the installment payment based on the total of the items in my cart. (Note that some businesses may have a minimum purchase amount to be eligible for Afterpay or other BNPL purchases.)

Clicking the ? next to the Afterpay option brings up a page that explains more about the BNPL option.

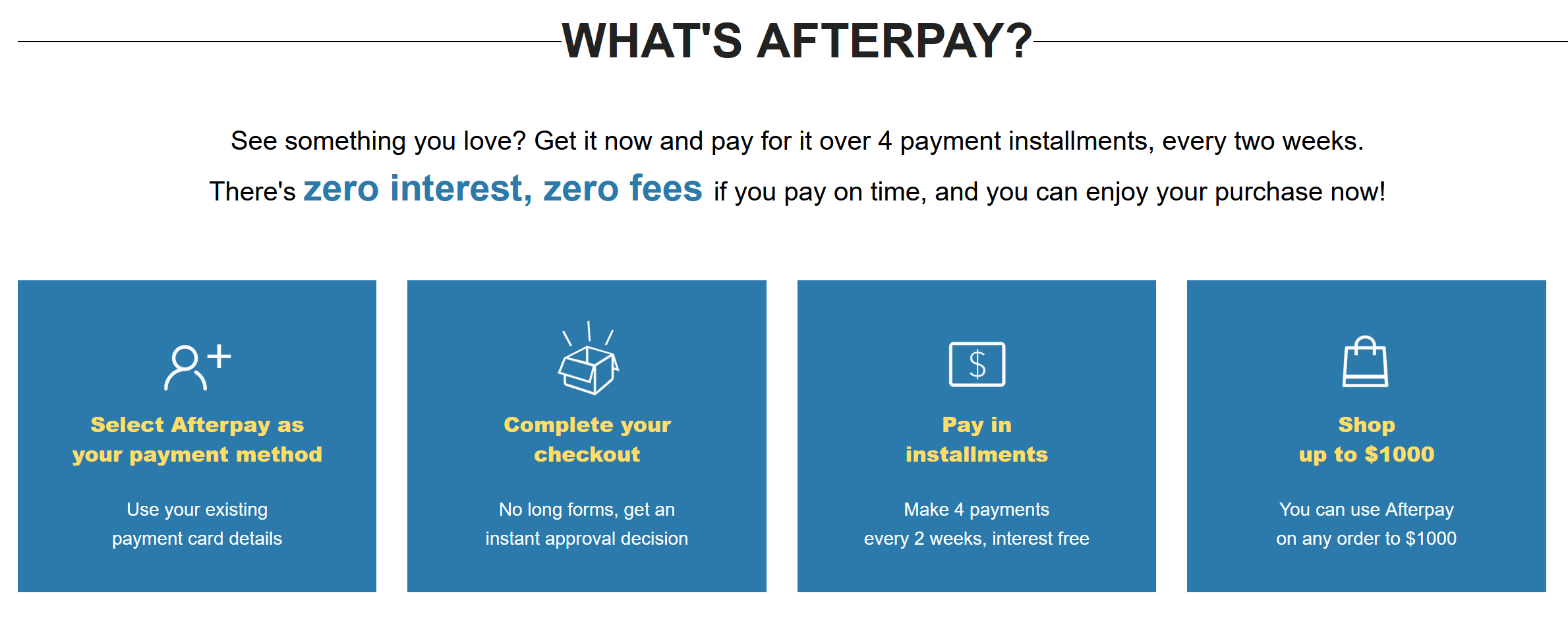

If the consumer chooses the Afterpay option, Afterpay will perform an eligibility check by doing a “soft pull” of the consumer’s credit. This does not impact the consumer’s credit score. If approved, the consumer proceeds to checkout, where they can either opt for “pay in 4” or a monthly repayment over 6-12 months. With “pay in 4,” their total bill gets split into 4 equal payments. The first is due at the time of purchase and the subsequent 3 payments are due every 2 weeks. Monthly installments vary by purchase.

Afterpay will require a payment method (typically a credit or debit card) that it will automatically charge on the due dates. However, customers can manage their payments and dates in the Afterpay app.

If the customer misses a payment, Afterpay charges a late fee (usually between $5-$10) and attempts to charge the payment method again.

If the consumer chooses the Afterpay option, Afterpay will perform an eligibility check by doing a “soft pull” of the consumer’s credit. This does not impact the consumer’s credit score. If approved, the consumer proceeds to checkout, where they can either opt for “pay in 4” or a monthly repayment over 6-12 months. With “pay in 4,” their total bill gets split into 4 equal payments. The first is due at the time of purchase and the subsequent 3 payments are due every 2 weeks. Monthly installments vary by purchase.

Afterpay will require a payment method (typically a credit or debit card) that it will automatically charge on the due dates. However, customers can manage their payments and dates in the Afterpay app.

If the customer misses a payment, Afterpay charges a late fee (usually between $5-$10) and attempts to charge the payment method again.

How Afterpay Works for Businesses

For business owners, integrating Afterpay into your checkout process is a relatively straightforward way to offer BNPL to your customers. Afterpay facilitates the transaction for you, taking on the risk and the administrative responsibilities of collecting the money for the duration of the “pay later” part. That means you get paid upfront, even though your customer will pay in installments. Afterpay charges you a transaction fee for the service. You’ll need to integrate Afterpay into your checkout process. For ecommerce businesses, Afterpay provides plugins for several popular platforms, such as Shopify and WooCommerce. While BNPL is commonly seen online, it can also be used in brick-and-mortar businesses. Afterpay offers an app that lets customers choose to use Afterpay for in-person transactions.Costs to to Use Afterpay at Your Business

While Afterpay can be beneficial, there are costs involved for business owners. You can expect to pay about 4-6% per transaction when your customer uses Afterpay. This is higher than many typical credit card processing fees. However, some businesses find that customers spend more money and purchase more often when using BNPL, so take that into account when considering if it’s right for your business. Afterpay does not have any setup fees or monthly fees.Business Owner Opinions

It can be tough to find reviews of Afterpay from the business owner point of view, as many of the reviews are from consumers. However, you can still find some out there. Afterpay’s website also has a “success stories” page from the business perspective. Some businesses report higher conversion rates and larger transaction totals when they offer Afterpay and other BNPL platforms. Consumers appreciate the ability to break purchases into smaller payments. With that option, large purchases aren’t as intimidating, and businesses benefit. On the Afterpay website, some business owners refer to the platform as a game-changer.Is Afterpay right for your business?

For many business owners, BNPL offers a unique opportunity to increase transaction sizes, reduce abandoned carts, and tap into a younger consumer base. However, it’s essential to weigh the costs against those benefits. If your business sells higher-ticket items or products with higher margins, Afterpay may be especially beneficial as the transaction fees could be absorbed by the increased volume and larger average order values. Additionally, businesses that appeal to younger, credit-averse shoppers will likely see stronger demand for BNPL. However, if your margins are thin or you’re selling lower-cost items, the higher transaction fees might cut into your bottom line, so it’s important to carefully assess whether Afterpay’s benefits outweigh the costs in your specific case. Additionally, small transactions aren’t as likely to be impacted by the option to pay later, since many consumers will simply pay for the total transaction without worrying about splitting it into smaller chunks. At the end of the day, Afterpay offers a convenient all-in-one BNPL service. If you’re looking to provide the option to pay in installments, but don’t want to take on the risk of customers defaulting, a BNPL platform is the way to go. Just be sure to monitor customer adoption and usage of Afterpay (or whatever BNPL platform you choose) to see if you’re truly getting value from it. Have you used Afterpay at your business? Did it improve conversions or increase your average transaction amount? Let us know in the comments!

Ben Dwyer began his career in the processing industry in 2003 on the sales floor for a Connecticut‐based processor. As he learned more about the inner‐workings of the industry, rampant unethical practices, and lack of assistance available to businesses, he cut ties with his employer and started a blog where he could post accurate information about credit card processing. As the blog gained in popularity, Ben began directly assisting merchants in their search for a processor. Ben believes in empowering businesses by providing access to fair, competitive pricing, accurate information, and continued support. His dedication to transparency and education has made CardFellow a staunch small business advocate in the credit card processing industry.