|

Volume Rate |

Per-Transaction Fee |

| Merit 1 Debit |

1.65% |

$0.15 |

| Merit 1 Prepaid |

1.76% |

$0.20 |

Note that the debit rate applies only to “unregulated” debit cards. That is, to debit cards issued by banks with less than $10 billion in assets. Banks that have more than $10 billion in assets issue “regulated” debit cards, which are subject to a cap on interchange fees.

The current regulated debit cap is set at 0.05% + 22 cents. That’s the most you’ll pay at the interchange level when you accept a regulated debit card. However, your processor can add their own fees on top of the capped interchange rate, so your final cost to accept a regulated debit card will be higher than 0.05% + 22 cents.

Other Rates for Specific Business Types

There are also Merit 1 rates specifically for real estate, insurance companies, and daycares.

The rates for real estate and insurance Merit 1 credit are the same:

1.43% + $0.05 per transaction for Core, Enhanced Value, and World and 2.25% + $0.10 per transaction for World High Value and World Elite.

The rate for daycare MCCs is 1.60% + $0.10 per transaction regardless of the credit card type (core or rewards.)

Now that we’ve tackled the rates, what are the requirements to actually qualify for Merit 1 interchange? Once again, it varies somewhat by card type.

Merit 1 Interchange Requirements

Every interchange category has specific requirements. Transactions that meet those requirements will “qualify” for that interchange category. For Merit 1, most criteria apply across all categories.

In order to receive Merit 1 interchange rates, a transaction must:

- Be card not present – that is, entered online or keyed in as opposed to swiped

- Pass 1 valid electronic authorization

- Have a matching authorization and settlement merchant category code

- Be settled within 3 days of the transaction date

If a transaction meets those criteria, you can expect it to qualify for Merit 1 interchange. Which specific category will be determined by the card used. Meaning, debit cards will receive debit merit 1, rewards cards will receive the appropriate rewards merit 1, etc.

However, if a transaction does not meet all criteria, it can downgrade to a more expensive interchange category.

Interchange Downgrades

In credit card processing a “

downgrade” occurs when a transaction falls to a more expensive interchange category. Every transaction has a “target” interchange category for which you can expect it to qualify when everything is done correctly.

However, if everything is not done correctly, and a requirement isn’t met, it will downgrade from the target category. A few downgrades here and there is normal. On the other hand, a lot of downgrades indicates a problem with your processing methods. Additionally, excessive downgrades cost you more.

If you’re seeing a lot of downgrades (usually identifiable by the words “

Standard” or various abbreviations like STND) it’s a good idea to look into it. CardFellow members can call us for assistance with downgrades.

Statement Abbreviations

Merit 1 rates will show up on processing statements either spelled out completely or under various abbreviations. Ultimately, your processor controls how they label your interchange categories. In some cases (such as with flat rate pricing) the processor won’t disclose interchange categories to you at all.

However, in situations where you can see interchange detail on your monthly processing statement, you may see Merit 1 listed as:

- MERIT 1 (for core credit)

- ENHMERITI (for enhanced merit 1)

- MCW MERITI (for Mastercard World Merit 1)

- HV Merit1 (for High Value Merit 1)

- MWE MERITI (for Mastercard World Elite Merit 1)

Remember, processors can list interchange by other names as well.

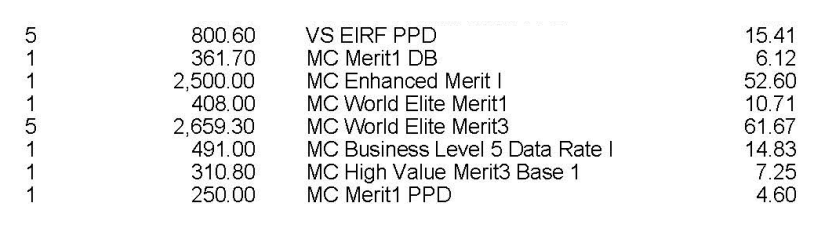

Some processors may not abbreviate Merit 1 at all. In the statement example below, you can see that the processor spells out not just Merit 1, but also World Elite and Enhanced. The only part it abbreviated is Mastercard (MC) and the situations where it was a debit card (DB) or a prepaid card (PPD) instead of credit.

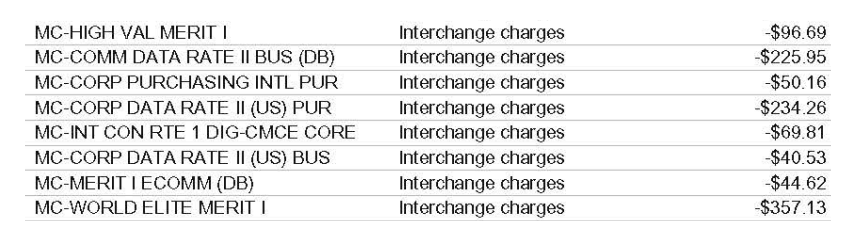

That's the case with another processor's statement as well. You can see from this one that the processor does abbreviate CR for credit and DB for debit, but otherwise spells out Merit 1, Enhanced, and World Elite.

This processor abbreviates a little bit more (High Val for High Value) but Merit 1 is still clearly listed by full name in the interchange fees.

Debit and Prepaid Merit 1 on Statements

As seen in some of the examples above, for debit and prepaid cards, you may see Merit 1 listed as:

- Merit 1 DB (for Merit 1 debit)

- Merit I PPD or PP (for Merit 1 prepaid)

Once again, your processor has discretion to label the categories using other names or abbreviations.