Credit card processing companies are popping up left and right offering “cash discount” programs to eliminate your credit card processing fees. Are they legal and are they permitted in merchant agreements?

The short answer: yes, when done correctly.

The longer answer is that there’s a lot of confusion about the difference between “cash discounts” and “surcharges,” or “checkout fees” and that confusion has led to labeling surcharge programs as cash discount programs. Let’s look at the differences between the two and how you can stay on the right side of laws and card brand regulations.

Cash Discount vs. Surcharge

A cash discount is when you post credit card prices and offer a discount on that price for customers who pay with cash.

A surcharge is when you post cash prices and charge an additional fee on top of that price for customers who pay with a card.

In the first situation, a customer may pay less than the listed price. In the second case, they may pay more than the listed price.

If you charge more at the register than the listed price, it is a surcharge, regardless of what processors call it. Even if a processor tells you that you’re simply adding a “service fee” or a “non-cash adjustment,” it is still a surcharge.

While it may sound like a minor difference, it’s actually very important in terms of legality and compliance with card brand rules. Getting it wrong means risking fines or having your merchant account shut down. So keep in mind the quick rule of thumb – if the customer pays less than the shelf price, it’s a discount. If they pay more than the shelf price, it’s a surcharge.

The end result is the same – customers paying with cash pay less than customers paying with a card – but the card brand rules and state laws make it important that everything is listed and disclosed to consumers properly.

Sources – Visa, the Durbin Amendment, CardX

CardFellow reached out to Visa and Mastercard to confirm the distinction between cash discounting and surcharging. Mastercard did not reply to CardFellow’s request for clarification on cash discounts. However, Visa provided a clear statement.

Visa

When asked about cash discounts, Visa told CardFellow: “A discount for cash is different from a surcharge. The rule states the posted price must be for cards, however, merchants can provide a lower price for cash acceptance. Discounts for cash are allowed by Visa. However, merchants are not permitted to post a price for cash, and then charge a higher price for cards.” [Emphasis added.]

In this statement, Visa clearly explains that a business offering a cash discount is allowed, but that the posted price must be for cards. Businesses can offer a lower price from that posted (card) price as a cash discount.

The Durbin Amendment

Visa’s statement squares with definitions found in the Durbin Amendment, which states that payment card networks will not restrict business’ ability to offer a discount for cash and check payments. The Cornell Law website defines “discount,” stating: “The term “discount”— (A)means a reduction made from the price that customers are informed is the regular price; and (B)does not include any means of increasing the price that customers are informed is the regular price.”

This section clarifies that a discount must be a reduction in price – not an increase in price. Some processors may argue that the “regular price” is the cash price. However, if the regular price is the cash price, then no discount on the regular price is being offered.

The “regular price” posted must be what you would charge a consumer for paying with a card. You would then give a discount from that “regular price” to cash customers.

CardX

We also reached out to CardX, a company that specializes in surcharge programs and has led the charge in making such programs available in more places across the country. CardX founder and CEO Jonathan Razi, a Harvard Law School graduate, explains that the definition of “regular price” comes from the Truth in Lending Act, specifically U.S.C. §1602(y):

“[…]The term “regular price” means the tag or posted price charged for the property or service if a single price is tagged or posted…” [Emphasis added.]

The “posted price” refers to prices posted on shelves, menus, invoices, or in advertisements. So, if a business posts a $10.00 price on a shelf, they would need to charge cash-paying customers less than $10 at the register in order to be offering a cash discount. Otherwise, it’s a surcharge. (Remember our rule of thumb from the beginning: Paying less than the posted price is a discount. Paying more is a surcharge.)

Razi confirms, “If the price on the shelf is $10.00, any fee added at the register constitutes a “surcharge” under U.S.C. §1602(r):

“The term “surcharge” […] means any means of increasing the regular price to a cardholder which is not imposed upon customers paying by cash, check, or similar means.”

Like Visa, Razi is unequivocal in his explanation. “The bottom line is that most purported “cash discount” programs are non-compliant because they list the cash price on the shelf and then add a fee at the point of sale. This brings them under the card brand rules for surcharging[…] Instead, a true “cash discount” program must increase the price listed on the shelf and then reduce it at the register when customers choose cash.”

Some processors are becoming aware of the distinction. Razi mentions that the Clover system (now offered by Fiserv, formerly known as First Data) removed all “cash discount” programs from its app marketplace, stating in an email to users, “A ‘true cash discount’ does not add any fees or surcharges at the register.”

At the time, First Data confirmed to CardFellow that the cash discount apps had been removed but that it’s possible to surcharge through the Clover system if legally allowed in the state where the business operates.

Dual Prices

In some jurisdictions, it may be possible (or required) to post both the cash price and the credit price in dollars and cents with equal prominence to handle the “regular price” situation. Many people have seen this at gas stations, early adopters of dual pricing.

Dual pricing can offer transparency to your customers so there are no “surprises” at the register. The shelf (or invoice, menu, or gas pump) clearly indicates that there are different prices for cash and for credit and explicitly states what those prices are.

Two states – Maine and New York – require that businesses post cash / credit prices in dollars and cents to be compliant with surcharging rules.

If you’re not sure about the requirements for your state, be sure to consult your lawyer or your state’s Attorney General.

Why does it matter?

There are two reasons that the execution of a cash discount program matters: state law where surcharges are prohibited and surcharge prohibition on debit cards.

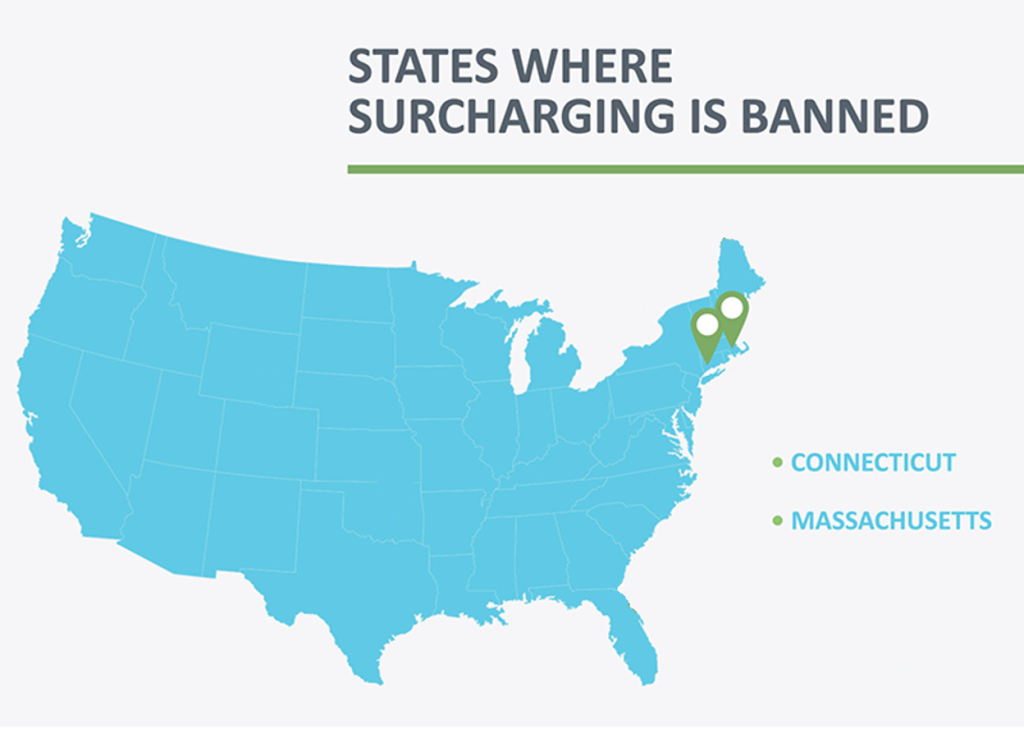

States Where Surcharging is Banned

Firstly, while cash discounts in their true form are allowed in all 50 states, two states still prohibit surcharging credit card transactions. If you surcharge in a state with a law against it, you’re breaking the laws of that state. As of 2025, surcharging is prohibited by law in Connecticut and Massachusetts.

This is down from 9 states, as surcharge laws have come under scrutiny in the past decade. Several states have gone to court over the practice. Some states have no-surcharge laws on the books but have faced legal battles and may not be able to enforce those laws.

State laws where surcharges are prohibited may change in the future. We’ll update this map as those laws change, but it’s a good idea to check with your lawyer or state Attorney General for the latest information before surcharging. Attorney Generals for each state have websites that may contain up to date information on practices such as surcharging.

Surcharge Prohibitions on Debit Cards

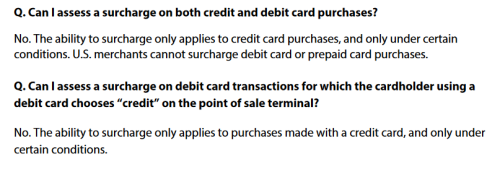

The second reason the cash discount / surcharge distinction matters is because surcharges are never permitted on debit cards. This is true even if cards are “run as credit” and even in states where credit surcharges are legal. Visa’s FAQ on surcharging clearly spells out that surcharges cannot be applied to debit.

If you’re adding a surcharge to a debit transaction, even if you’re calling it a “non-cash adjustment” you’re risking your merchant account. You could face fines or have your processing account closed.

Razi explains: “You cannot apply a fee above the listed price to a debit card, no matter what the fee is called. When you list a price and then add a fee at the point of sale, it is definitionally a surcharge under the law, and must comply with the card brand rules (and state laws, where applicable). For this reason, the fee (whether labeled a “surcharge”, “non-cash adjustment”, “service fee”, or anything else) can never be applied to a debit card, and “cash discount” programs that add a fee to debit are exposing their merchants to fines and shutdowns by the card brands.”

You’re never able to add a fee to transactions a consumer makes with their debit card, and it’s a good idea to steer clear of any processing companies that enable it.

Repercussions

The consequences for surcharging debit or for implementing a cash discount program that’s really a surcharge program without complying with surcharge rules can be serious. Processors can shut down accounts when they’re informed by the card brands of non-compliance. Furthermore, both Visa and Mastercard have forms on their websites that allow cardholders to easily report being charged a fee for card use.

For violations of the card brand rules, Razi states that businesses can be fined $1,000 per occurrence, increasing to $5,000, $10,000, and $25,000 per occurrence for repeated violations. Ultimately, the merchant may be added to the Terminated Merchant File (“TMF,” or MATCH list) which makes it difficult to secure a merchant account from any processor in the future.

For the sake of your merchant account and your wallet, be sure you’re on the right side of laws and card brand regulations before surcharging or signing up for a cash discount program.

Spotting a Surcharge Program

The tricky thing is that many processors offering “cash discount” programs are actually offering surcharge programs but labeling them as “cash discount” programs. How can you tell if a processor is offering a true cash discount program, or if it’s a surcharge program in disguise? Look for the following:

- Reference to a “non-cash adjustment” or “service fee”

If a processor states that customers paying with cards will receive a non-cash adjustment or service fee when they check out, it’s a surcharge program. Remember, paying more at checkout is a surcharge, regardless of what it’s called. - Explaining you’ll post “cash prices”

Processors offering surcharge programs may explain that your business will list “cash prices” on shelves and will add a fee for customers that don’t pay with cash. If you’re not posting credit card prices and offering a discount for cash, it’s a surcharge program. Again, the customer is paying more at checkout. That means it’s a surcharge.

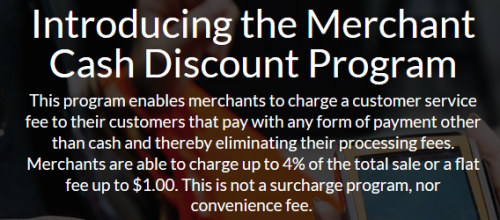

In the screenshot below, a company introduced a “cash discount” program that incorrectly stated that charging a service fee is not a surcharge program.

Looking at the first sentence with the phrase “customer service” removed shows more clearly that it’s a surcharge program. The sentence would read, “This program enables merchants to charge a fee to their customers that pay with any form of payment other than cash…” Charging a fee for paying with a card is, by definition, a surcharge. Claiming that it’s a “customer service” fee doesn’t change that. Tellingly, the company also references a 4% cap, which is the maximum Visa and Mastercard allow for surcharges.

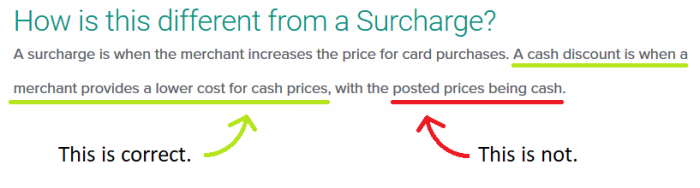

Unfortunately, some processing companies wrongly address the difference between a cash discount and a surcharge. For example, you may see a FAQ section with a question like, “How is a cash discount different from a surcharge?” In the screenshot below, a company answers that question by saying that a cash discount means offering a lower price for cash, with the posted prices being cash.

This processor appears to think that “increasing the price for card purchases” means increasing the posted / shelf price and is irrelevant to the actual price charged. However, if the posted price is for cash and the business charges a card user more, they have “increased the price for card users.” As covered thoroughly in this article, the posted prices must be for cards, with the discount offered on that posted price. Posting cash prices and then implementing a fee at the register is a surcharge.

Of course, not all surcharge programs are misleadingly called cash discount programs. Many processors offer surcharging capabilities and can help you implement surcharges as long as they’re legal in your state. Read more about adding a fee for credit card transactions to determine if implementing a surcharge program may be the right move for your business.

Should You Implement a Cash Discount?

Implementing a true cash discount program sounds like a no-brainer, but keep in mind that to do so, you’ll need to list credit prices on the shelves. If you’ve already priced your goods and services to account for the cost of credit cards, implementing a cash discount program is easy. You won’t need to change your shelf or menu pricing and can simply offer a discount on those prices to cash customers.

For most businesses, there’s no harm in offering a cash discount if you’ve set prices to account for cards. It simply means that you’re passing the credit card processing fee savings to your customer. However, be aware that some customers think that cash-preferring businesses may not properly pay taxes, which can negatively affect perception of your business.

By contrast, surcharge programs add a fee at the time of checkout. Some surveys indicate that customers react negatively to added fees, so you may find more resistance to a surcharge program than to a cash discount program. Where customers see a discount as a benefit or perk, they see a surcharge as a penalty.

Additionally, surcharges cannot be added to debit cards, so be aware that you’ll still pay the costs associated with processing debit cards. This is true even if you don’t accept PIN debit and run the debit cards “as credit.” How much will that impact your business? It depends on how much of your processing volume is credit and how much is debit, and then further depends on the current rates and fees you’re paying for accepting debit. Read more: How much are debit card processing fees?

Cash discounts and surcharge programs aren’t automatically bad ideas.

However, surcharge programs disguised as cash discount programs can open you up to negative repercussions, including fines or even loss of your merchant account. Any business that has abruptly had an account closed can tell you the headaches (not to mention lost revenue and negative customer perception) that come with not being able to accept cards.

Credit Card Minimums

If you’re uncertain about implementing a surcharge program or a cash discount, you can choose to start instead by simply imposing a credit card minimum – this is an amount that you’ll require customers to spend in order to use their credit card. You can set a minimum of any amount up to $10 for credit card transactions. Customers that want to make purchases under $10 will either need to use debit cards (which typically incur lower processing fees) or pay with cash.

Note: You cannot apply the minimum purchase requirement to debit card transactions. Customers that wish to use a debit card must be allowed to do so for any amount.

Conclusion

If you want to take advantage of a cash discount program to lower your processing fees, be sure to choose a processor that will help you correctly implement it. Avoid processors peddling surcharge programs under the “cash discount” name.

These days, surcharge programs are legal in more states than ever, so there’s even less reason for processors to act deceptively or market their cash discount programs as surcharge programs. If you’d prefer to charge a fee for credit card use rather than mess with shelf pricing and ensuring you’re posting credit prices, work with a processor that can offer compliant surcharge programs.

Need help finding the right processor? Try a free CardFellow.com account for expert assistance and easy comparisons.