What is Surcharging?

Simply put, credit card surcharging means adding a fee to the total transaction price when a customer pays with a credit card instead of another method. (Such as cash, check, or debit card.) The fee is a percentage of the total and subject to a cap set by the card brands. This cap can be superseded by state law. The surcharge is added at the point of sale and increases the total amount due by the customer. For example, if your business imposes a 4% surcharge (the maximum allowed in most states), a customer purchasing a $10 item with a credit card would pay $10.40. (4% of $10 = $0.40.) Update: In spring 2023, Visa announced that it was lowering the surcharge cap from 4% to 3% (or the actual cost of processing, whichever is lower.) Representatives for the company have referred to surcharging as "not great" for the customer experience. At the time of this update, Mastercard's cap is still set at 4% or the actual cost of processing, whichever is lower. Questions remain regarding Visa's legal authority to alter the cap, but so far no challenges have been brought in court.Surcharging History

Surcharging has not always been permitted. Prior to 2013, it was prohibited by the card brands - specifically Visa and Mastercard - because the companies didn’t want to dissuade customers from using their credit cards. Visa and Mastercard have always prohibited these fees as part of their merchant agreements; Discover and American Express allowed them, but forbade businesses to surcharge their cards differently than any other brands. So, unless a business only accepted Discover and American Express - which was unlikely - surcharges were off the table.Legal Cases

A 2013 class action lawsuit against Visa and Mastercard resulted in a settlement allowing businesses to charge customers a fee for using credit cards. This fee is now commonly referred to as a “merchant surcharge, “surcharge,” or “checkout fee.” The latter name has fallen out of favor but may still be seen in some locations. While that court case went through appeals, it was ultimately upheld in 2023. Additionally, in 2017, the United States Supreme Court heard a case involving the legality of surcharging in the state of New York. Lower courts had upheld the state’s ban on surcharging credit cards. However, the Supreme Court ruled that the New York law regulated speech, not business conduct, potentially making the law unconstitutional, and remanded it to the lower courts to specifically review in terms of free speech. In 2019, the State of New York and plaintiffs reached an agreement to dismiss the case, a move that allowed New York businesses to begin surcharging, provided that businesses disclosed the fees to customers in dollars and cents. The case was seen as a watershed moment for surcharging, with legal experts and industry insiders predicting widespread ability to surcharge in the following years. Indeed, as of 2025, only four states still prohibit surcharges by law - California, Connecticut, and Massachusetts. The class action settlement and the New York case allowed businesses to reduce the impact of credit card processing fees by instead passing those costs on to consumers. However, there are many rules businesses must follow in order to charge those fees, as well as pros and cons that should be considered before deciding if surcharging is the right move.Fast Facts on Credit Card Surcharges

- Surcharges are legal in most states

- Adding fees not against merchant agreements; the card brands allow surcharging

- California, Connecticut, Maine, and Massachusetts prohibit surcharges

- Colorado, New York, and Texas have surcharge laws being challenged in court or special rules for surcharging

- Where legal, surcharges are only allowed on credit cards, NOT debit cards

- The card brands cap surcharges at a fixed percentage or the "actual cost of processing," whichever is lower. Visa caps surcharges at 3% and Mastercard caps them at 4%. This applies except in Colorado, where the cap is 2%

- Businesses must inform customers of the surcharge before checkout

- Surcharges and cash discounts are not the same thing

Surcharge Basics

As you consider whether or not surcharging is right for your business, start by familiarizing yourself with some essential information — the difference between checkout fees (surcharges) and convenience fees, the states where surcharging is currently banned, and the procedures you must follow in order to start surcharging.Surcharges vs. Convenience Fees

Even before the Visa & Mastercard settlement, businesses could to charge their customers convenience fees for using credit cards in a very limited set of situations. These fees are meant to be used when paying with a credit card is a “bona fide” convenience over other forms of payment — for example, if the only other option for the customer would be a money order. Unlike surcharges, convenience fees are a flat amount, not a percentage. Most transactions — including any transaction that is face-to-face, and any transaction done over the phone or online if that is the only method of payment available — fall outside the definition of a convenience fee. CardFellow has an excellent guide to convenience fees, and the rules for these have not changed. However, a surcharge does not have to meet the requirements that a convenience fee does. Instead, it applies to any credit card transaction as a cost of using that card. This applies to all four of the major card brands - Visa, Mastercard, Discover, and American Express. There are limits on what businesses can charge and conditions that they must meet in order to surcharge credit card transactions — the next part of this article will explore these in depth.States Where Surcharging is Banned

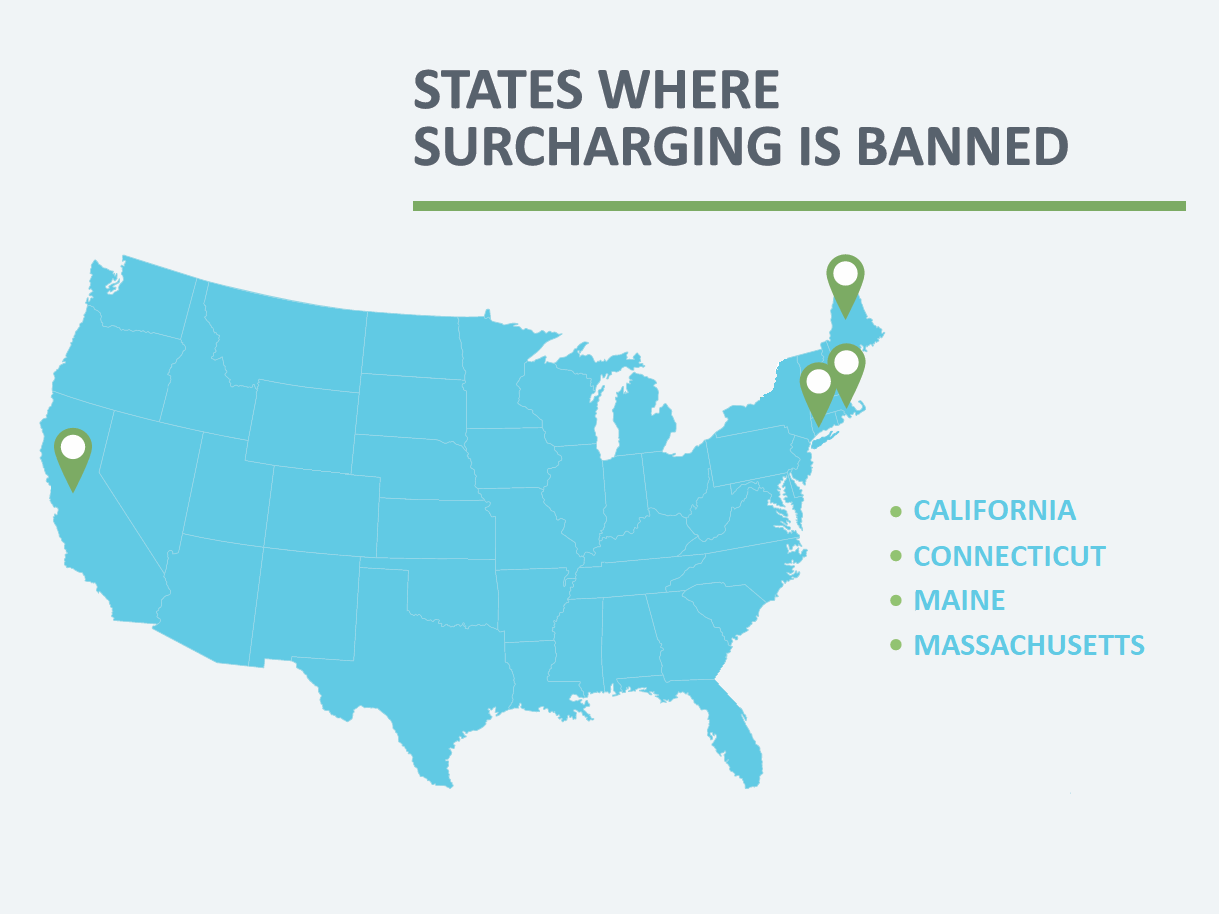

As of 2025, there are four states that prohibit surcharging: California, Connecticut, Maine, and Massachusetts. If your business operates in any of those states, you may not charge credit card fees to your customers. Several states still have anti-surcharge laws on the books, but they are being challenged in court or are currently unenforceable.

On the other side of the coin, several states are considering or have pending legislation that would make surcharging illegal if passed. Those states include Hawaii, Illinois, New Jersey, and Rhode Island. Many experts believe it is unlikely that new bans on surcharges would actually go into effect due to successful court challenges to surcharging in other locations.

If you do business in multiple states, you may only surcharge credit card transactions in the states that allow it.

Several states still have anti-surcharge laws on the books, but they are being challenged in court or are currently unenforceable.

On the other side of the coin, several states are considering or have pending legislation that would make surcharging illegal if passed. Those states include Hawaii, Illinois, New Jersey, and Rhode Island. Many experts believe it is unlikely that new bans on surcharges would actually go into effect due to successful court challenges to surcharging in other locations.

If you do business in multiple states, you may only surcharge credit card transactions in the states that allow it.

State-Specific Rules

Several states have their own rules (or court challenges) surrounding credit card surcharging. We’ve included information on those states and their specifics below, but be aware that the legal landscape in these states may shift quickly. It’s a good idea to consult a business attorney or your state's Attorney General prior to implementing a surcharge program if you’re in a state dealing with surcharging grey areas such as those listed below.California

California has a messy history with surcharges. The state originally prohibited them, but court challenges called the ban into question. In 2018, courts in the state of California ruled that the ban on surcharges was unconstitutional as it placed restrictions on business’ speech. But in the summer of 2024, California put forth Senate Bill 478, the Consumer Legal Remedies Act, designed to eliminate so-called "junk fees." Governor Gavin Newsom signed the bill into law, which requires that all fees must be included in the list price of an item. There are some exceptions - government required fees such as sales taxes or fees such as "reasonable shipping costs" don't have to be factored into the displayed price. Surcharges do fall into the fees that must be part of the price. The law does not regulate what businesses can charge, but the posted price must include all the required fees. The Office of the Attorney General's website keeps a list of FAQs about the law. That FAQ specifically addresses the question, "Can a business comply with this law by listing or advertising one price and separately stating that an additional percentage fee will apply?" This question is clearly asking about surcharges, which are a percentage of the total and required to be disclosed in posted signage in states that allow surcharging. The answer from the site is clear: "No. The price listed or advertised to the consumer must be the full price that the consumer is required to pay." However, the next question in the FAQ reads: "Does a business need to include credit card processing fees in the advertised price?" The answer on the site is "Generally, no, because a credit card processing fee is not a mandatory fee if the customer can avoid the fee by paying a different way (e.g. cash.) However, if a business only accepts credit cards as a form of payment, then the credit card fee is mandatory and would have to be included in the advertised price."Colorado

While Colorado does allow surcharging, it has a more restrictive cap on the fees a business can charge. Colorado businesses can only add a fee up to 2% or the actual cost of processing, whichever is lower.New Jersey

Like other states, New Jersey allows surcharging, but it caps the surcharge to limit profiting from it. The law states that businesses must post notices about the surcharge and caps the surcharge at the cost of processing the transaction. Technically, according to Visa and Mastercard rules, businesses should already be limiting the surcharge to their actual cost of processing (or not more than 3% for Visa or 4% for Mastercard.) This law simply enforces that and gives the state of New Jersey the ability to pursue action against businesses that profit from surcharges.New York

New York has a complex history with surcharges and the state's legal case was one of the more well-publicized, in part due to its escalation. In 2017, the Supreme Court heard a case regarding the legality of surcharging in the state of New York. Lower courts had upheld New York’s ban on surcharging credit cards. The case, Expressions Hair Design v. Schneiderman, was heard in January of that year, with the SCOTUS weighing in during early April. The Supreme Court stated that the New York law regulates speech, not business conduct, which could potentially make the law unconstitutional. The Supreme Court remanded the case to lower courts, who reviewed it specifically in terms of free speech. In early January 2019, the State of New York and the plaintiffs reached an agreement to dismiss the case. Dismissal allowed New York businesses to pass credit card fees to customers provided that business makes a disclosure to the consumer showing the credit price in dollars and cents. Razi, who authored CardX’s amicus brief in the Expressions Hair Design Supreme Court case, explains that he, “Expect[s] the New York law will survive, but in a far narrower form—and ‘no surcharge’ will simply mean ‘no surprise.’" Indeed, a law enacted in early 2024 stated that businesses must clearly display the total price for paying with a credit card - including any applicable surcharges. Additionally, the law prohibits surcharges greater than the actual cost of processing. This should have already been the case, as its part of the card brands' rules, but is now also codify in the NY law.Maine

According to the Maine legislature website, the state does not permit surcharging. "Surcharge prohibited. A seller in a sales transaction may not impose a surcharge on a cardholder who elects to use a credit card or debit card in lieu of payment by cash, check or similar means. For purposes of this section, "surcharge" means any means of increasing the regular price to a cardholder that is not imposed on a customer paying by cash, check or similar means." This text clearly states that a business may not impose a surcharge for payments made by credit or debit card instead of ones made by cash or check. Discounts for using cash or check are still permissible.Texas

As of 2018, Texas businesses can surcharge in most cases. In Rowell v. Paxton, the court determined that surcharging is considered protected speech under the First Amendment. Thus, the Court ruled Texas’ “no surcharge” law unconstitutional. However, there may be instances where surcharging is still not permissible. The Texas State Law Library, a government website that serves the research needs of the Texas Supreme Court, Attorney General, and other legal agencies, has a page dedicated to the question of surcharging, but as of this update, it states that the question is complex. It goes on to explain that surcharging may still be against the law in some instances. It references the 2018 Rowell v. Paxton case, where the ban on surcharging was deemed unconstitutional. However, the page then cites an opinion provided by the Attorney General in 2019 stating that the law is still enforceable in certain situations. The AG states: “When a court determines that a statute is unconstitutional as applied, it normally invalidates the statute only as applied to the litigant in question and does not render the statute unenforceable with regard to other litigants or different factual circumstances. […] Thus, circumstances may still exist where, as applied, section 604A.0021 operates to prohibit a credit card surcharge fee.” In this statement, the Attorney General is explaining that the court decision only applies to the party involved in the court case and that it does not mean the state ban on surcharges can never be enforced in other situations. If you’re running a business in Texas and are considering surcharging, be sure to check with a licensed attorney in your state or consider a compliant cash discount program rather than a surcharge.Pros and Cons of Credit Card Surcharges

Deciding to surcharge isn’t easy - there are pros and cons to doing so and you should carefully weigh the costs and benefits for your business. The benefits are fairly straightforward:- Surcharging can help your bottom line It’s unlikely you’ll be able to completely eliminate your credit card processing costs by surcharging, but you can defray a large portion of them.

- If processing costs are built in to your prices, it’s possible that surcharging will allow you to lower prices across the board. This, in turn, could make your business more competitive, especially if most of your customers pay with cash, check, or debit cards.

- Most of your customers use credit cards Remember the principles of supply and demand - if you add a few percentage poitns to each transaction, customers who shop with credit cards may buy less. In addition, studies have repeatedly shown that consumers spend more with credit cards than with cash. Even if your customers switch, it’s very possible that they will spend less if they feel limited to the cash they carry in their wallet.

- It’s easy to find alternatives to your business nearby If a consumer can get a similar product or service for the same price across the street, and that business doesn’t surcharge, why would they go to the one who does?

- Your typical transactions are high dollar amounts Consumers likely won’t flinch over 3% added to a pack of gum; 3% added to the price of a TV is a different story. The more your goods or services cost, the more likely a surcharge will cause them to buy less - or not purchase from you at all.

- You serve consumers who are particularly averse to surcharges Older generations are somewhat more likely than younger generations to have an aversion to credit card surcharges.

How to Get Started

If you’re allowed by state law to charge a fee for using a credit card and you’ve decided it’s the right move for your business, here’s the process to get started: Notification- Notify the card brands you accept of your intent to surcharge. Visa and Mastercard each require notice of intent to surcharge. Mastercard provides information about disclosing intent to surcharge in their surcharging FAQ. Each brand requires 30 days notice before you may begin surcharging customers.

- Inform your acquiring bank of your intent to surcharge. Different banks have different procedures; most require 30 days’ notice as well. Your merchant service provider will likely be able to tell you what n meet this requirement.

- Decide what to surcharge. You can choose whether you want to charge for only specific types of cards (such as rewards cards, which tend to carry higher costs for businesses) or for all cards issued under a brand. You must choose one or the other — you cannot charge a fee for all cards and an additional fee for card products which have higher processing costs.

- Both Visa and Mastercard require businesses to post a sign both at the main entrances to their business and at all points of sale notifying customers that their credit card purchases will be subject to credit card surcharges. The signs on entrances need to inform customers that you charge fees, while the point of sale signs must disclose the percentage that will be added to the transaction. Visa provides signage that you can print out and use.

- Online businesses have to let customers know about fees on the first page of their website that references card brands

- Credit card surcharges need to appear as a separate item on receipts. In many cases, your merchant service provider will need to program your point of sale terminals to meet this requirement. Contact them with questions.

The “Don'ts” of Surcharging Cards

Both the court settlement and the card brands have outlined specific limits on surcharging in order to protect consumers. If you decide to surcharge, protect yourself from costly chargebacks or sanctions from your acquiring bank and the card brands by remembering the following:- Don’t charge a fee greater than your actual credit card processing cost. Visa and Mastercard base this on whatever your merchant discount rate was in the last quarter.

- Don’t charge a fee higher than 4% of the transaction for Mastercard or 3% for Visa. The surcharging settlement outlines this limit.

- Don’t surcharge debit cards or prepaid cards. These forms of payment are specifically excluded from the settlement. You cannot surcharge a debit card, even if it’s “run as credit.”

- Don’t forget to let your customers know that you charge credit card fees. The card brands' requirements are outlined in this article. Your customers should always know what forms of payment you surcharge, as well as how much your surcharge, before they use their card.

- Don’t keep surcharge fees when refunding customers. When issuing refunds, you must also refund any surcharges - even for partial refunds. For example, if you refund 50% of a customer’s purchase, you need to refund 50% of the surcharge you collected.

Alternatives to Surcharging

Not sure that surcharging is the right answer? Consider these alternatives:- Offer a cash discount While it sounds - and is - similar, a cash discount is an option to “reward” customers who pay with cash rather than “penalizing” credit card customers with an added fee. You can offer a cash discount to customers that don’t pay with plastic. Many gas stations, for example, already engage in this practice.

- Impose a minimum purchase amount Businesses can set a minimum purchase up to $10 for credit card transactions. Setting a $10 minimum ensures a higher transaction amount, making it more worthwhile to eat the cost of credit card processing. Note: You cannot impose minimums on debit card transactions.

Ben Dwyer began his career in the processing industry in 2003 on the sales floor for a Connecticut‐based processor. As he learned more about the inner‐workings of the industry, rampant unethical practices, and lack of assistance available to businesses, he cut ties with his employer and started a blog where he could post accurate information about credit card processing. As the blog gained in popularity, Ben began directly assisting merchants in their search for a processor. Ben believes in empowering businesses by providing access to fair, competitive pricing, accurate information, and continued support. His dedication to transparency and education has made CardFellow a staunch small business advocate in the credit card processing industry.