When looking for the best credit card processor for your business, the pricing model the processor uses can have a big impact. Pricing models dictate how processing fees are charged and passed to you and can set the stage for either very competitive or very expensive pricing.

In this guide to pricing models, we’ll explain the pros and cons of different options.

Fundamentals of Processing Fees

Before we can get into pricing models, it’s important to start with a basic understanding of processing fees. Every credit card transaction is comprised of three parts: interchange, assessments, and markup.

![]()

Interchange is the largest component of costs. There are hundreds of interchange categories, each with a rate and fee associated. The interchange cost for any given transaction depends on the category for which it “qualifies.” Interchange costs are non-negotiable, and they go to the banks that issue credit cards to consumers.

Assessments are fees paid to the card brands. They are also non-negotiable. CardFellow keeps a running list of credit card assessments.

Together, interchange and assessments can be thought of as the “wholesale” cost of credit card processing. As with anything, you want to pay as close to wholesale as possible.

Markup refers to the processors’ fees on top of interchange and assessments. It’s the only component that’s negotiable. All processors charge a markup (even the ones that claim they don’t) because that’s how they make money.

Any fee that is not interchange or assessments is part of the processor’s markup. That includes monthly or annual fees, statement fees, PCI compliance fees, per-transaction fees, etc.

Your goal is to pay a small markup. To do that, you’ll need to be able to separate the wholesale cost and the markup. Pricing model plays a big role here.

Pricing Models: Interchange Plus

The most transparent pricing model, interchange plus also has the potential to be the lowest cost. On an interchange plus pricing model, the processor will charge you the cost of interchange and assessments plus a small markup. The three components of cost will be separated on your monthly statement, allowing you to easily see your wholesale cost and the processor’s markup.

While at one time, interchange plus was not commonly available to small businesses, that’s no longer the case. All of the certified quotes in the CardFellow marketplace are required to use an interchange plus pricing model.

However, remember that interchange plus simply dictates that a processor will list the components of cost for you – it doesn’t guarantee that you’ll pay only the true cost of interchange and assessments unless you have a specific agreement with the processor.

Read more about why interchange plus isn’t a silver bullet.

At CardFellow, certified quotes will include interchange and assessments passed to you at true cost, so you won’t need to worry about padded fees. Additionally, we monitor your statements for you to ensure that your processor charges you correctly.

Wholesale Processing

Wholesale credit card processing is a trendy name for interchange plus. Processors will promise “wholesale rates” or state that you’ll have exclusive access to “wholesale pricing.” Remember, the sum of interchange and assessments is “wholesale.” There will still be a markup on the wholesale amount, as the processor needs to make money, too.

Some processors claim that their wholesale pricing “eliminates middlemen” or lets you go “direct to the card companies.” These claims are a bit misleading – Visa, Mastercard, and Discover don’t offer merchant accounts directly to businesses, so it’s not possible to go “direct” to the card companies. Additionally, every processor is technically a “middleman” as that’s the function of a processing company. They act as the go-between for you, your customer’s bank, and your bank.

“Wholesale” processors may still offer good pricing, but don’t fall for the marketing spin. It’s not a different pricing model, and yes, you do still pay a markup.

0% Markup Processing

Another spin on interchange plus is “0% markup” processing. Processors using straight interchange plus pricing will typically quote their markup as a percentage and a per-transaction fee. For example, a processor placing a certified quote in the CardFellow.com marketplace might quote a markup of 0.20% and 10 cents per transaction.

A 0% markup processor will quote 0 percent markup, but still charge per-transaction fees. Additionally, while most interchange plus processors quote a monthly or annual fee, 0% markup processors typically charge a much higher monthly or yearly fee to make up for the 0%.

In some cases, 0% markup processors try to make it sound like there’s no markup at all. This isn’t accurate. Rather, there’s just no percentage-based markup. Remember, any charges other than interchange and assessments are a markup. That includes per-transaction fees, monthly or yearly fees, statement fees, etc.

Membership Processing

Membership processing is a type of processing (usually by a processor quoting interchange plus or 0% markup) where you’ll pay a large “membership” fee. It’s not actually a different type of processing; it just has a different name.

Pricing Models: Tiered or Bundled Pricing

The least transparent type of pricing is called “tiered” or “bundled” pricing. Unlike interchange plus pricing, many processors using bundled pricing will not break out the separate components of cost on your statement.

With tiered pricing, the processor will create “tiers” for your transactions. Typically, there will be three tiers – qualified, mid-qualified, and non-qualified – but a processor could use more or fewer tiers if they wish. The processor assigns a different rate to each tier, with the “qualified” tier receiving the lowest rate and the “non-qualified” tier the highest. Most often, the processor will show you the “qualified” rate prominently, hiding the mid-qualified and non-qualified rates in small print or assuring you that those only apply to certain cards.

Then the processor decides which of your transactions it will charge according to the different tiers. In many cases, the processor will charge the bulk of your transactions at the mid-qualified or non-qualified tiers, resulting in high costs.

It’s very difficult to see the wholesale costs and the markup with this type of bundled pricing, which makes it impossible to tell if you’re getting a good deal by paying close to wholesale. Even worse, the processor can change which of your transactions go to which tier at any time, making it difficult to accurately plan for your processing costs.

At CardFellow, we advise avoiding tiered pricing with “qualified” and “non-qualified” rates.

Read more about tiered credit card processing.

Flat Rate Pricing

Technically a type of bundled pricing, flat rate pricing can be good for some businesses, in limited circumstances. It has caught on in part because it looks easy. But it’s important to note that it’s not often a low cost solution.

Flat rate pricing is what it sounds like. The processor charges you one flat rate for all your transactions, regardless of card type. This is the type of pricing offered by companies you’ve probably heard of, like Square, Stripe, and PayPal.

Like all types of tiered pricing, flat rate is not very transparent – you won’t be able to determine the wholesale cost and the processor’s markup from your statement.

Simplicity

What you do get with flat rate pricing is a billing statement that looks simple and easy-to-predict costs. For example, if a flat rate processor quotes you 2.75% on all swiped transactions, you know that you can do the math. 2.75% of your credit card sales will go to processing fees.

However, it’s important not to confuse simplicity with competitive pricing. Behind that flat rate, interchange, assessments, and markup still apply – you’re just not able to see them because they’ve been bundled together into one percentage. Moreover, that percentage has to cover the processor’s costs and its profit, so the rate tends to be on the higher side.

Flat rate processing is typically a good solution for businesses with average transactions under $10 or that accept less than $3,000/month in credit cards. If that’s not your business, you’ll likely find lower cost processing working with a competitive interchange plus processor.

If the thought of complicated interchange costs and lengthy billing statements has you wary, remember that choosing a processor through CardFellow.com means you’ll get complimentary statement monitoring from our processing experts. We’ll keep an eye on your processing costs for you so you can run your business.

Zero Fee Processing

Zero fee credit card processing (also called free credit card processing or surcharge processing) is a model in which the processor will charge processing fees to your customer by way of a surcharge on their purchase.

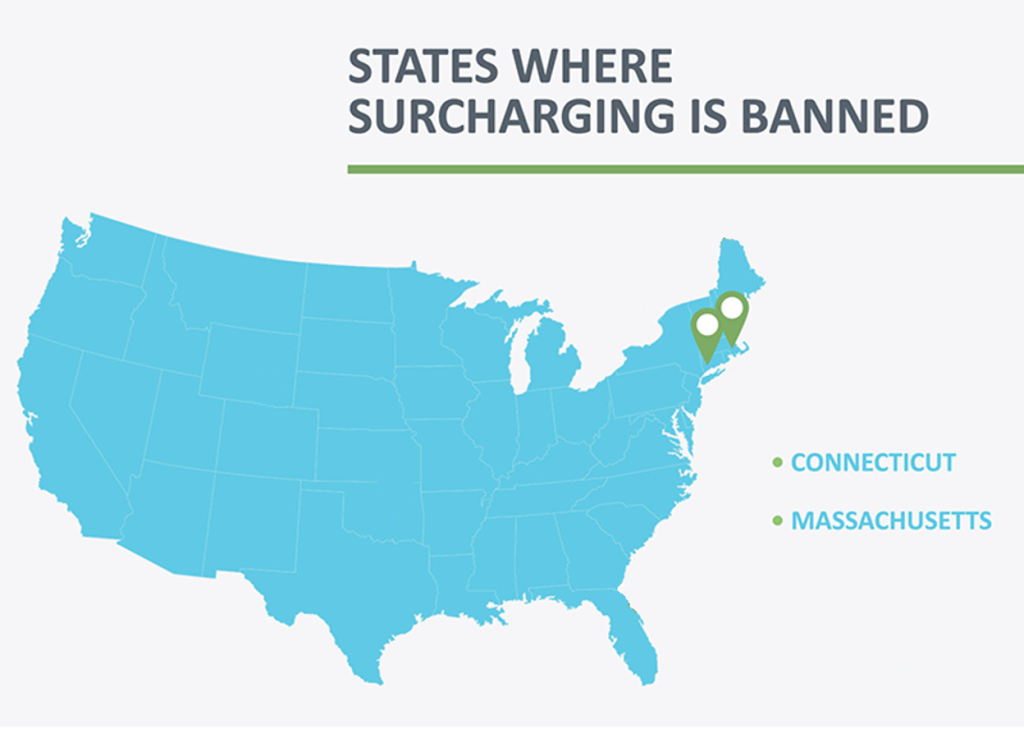

When you get set up with a surcharge / zero fee processor, the company will configure your terminal to add a surcharge up to 4% to your customer’s total. Note that surcharging (and thus zero fee processing) is not permitted in certain states. Additionally, you cannot surcharge debit transactions, even when “run as credit.” If you’re in a state that prohibits surcharges, you will not be able to use zero fee-style processing. At the time of this update, only two states prohibit surcharging: Massachusetts and Connecticut.

If you do use zero-fee processing, you’ll still be responsible for charges for debit cards, equipment charges (if applicable), and any monthly fees. Some processors that offer zero-fee processing require monthly fees for utilizing their equipment.

It’s also worth noting that in most states, surcharging is permissible. You can choose to pass on the cost of processing to your customers through a surcharge regardless of what pricing model you use. “Free” processing simply handles setup for you rather than requiring you work with your processor for setup.

Which costs customers more?

In many cases, if you’re on a competitive interchange plus pricing model and choose to surcharge, your customers will pay less than if you surcharge through a zero-fee processor. The reason is that surcharges can’t exceed the actual cost of processing or 4%, whichever is lower. Businesses on a competitive interchange plus model will typically pay much lower rates than 4%, so the surcharge to customers would be lower as well. However, no-fee processors typically jack up the cost of processing to just under 4% so that they can surcharge your customers for the maximum allowable amount.

Read more about zero fee processing.

The Best Credit Card Processor

The best credit card processor for your business is going to depend on your needs, industry, and more. Credit card processing is one area of business where it’s not always a great idea to go by reviews or get recommendations from fellow business owners. Processors can (and do!) set pricing and terms differently for each business. That means Jane could get a great deal from Processor A and Bob could get an expensive deal from the same exact company.

To find the best credit card processor for your business once and for all, check out CardFellow’s free quote comparison tool, which provides best-pricing-first quotes from leading processors and includes protections like a lifetime rate lock on markup, no cancellation fees, and more. Best of all, it’s completely free and private. Try it now.