You’re probably already aware that you pay an interchange fee anytime a customer pays with a credit card. Interchange fees are generally the most expensive component of credit card processing costs, and they’re non-negotiable.

However, some credit card processors are now offering “zero fee” processing as a way to seemingly get around interchange fees and attract businesses to use their services. These processing options may have different names: zero fee processing, cash discounting, and free credit card processing.

Obviously there’s a lot of fine print involved, and it’s important to understand these “zero-fee” programs before signing up for one of these services. While they may seem tempting at first, those fees aren’t just disappearing. Instead, your customers will pay them. As charging customers more may have an impact on sales and customer satisfaction, it’s important to consider whether “free” credit card processing will cost you in the long run.

Let’s take a look at surcharging and zero-fee processing solutions for card-present (in person) transactions.

- What Is Zero-Fee Processing?

- Is there really no cost to me?

- Zero-Fee Processing Considerations

- Differences Between Surcharging and Zero-Fee Processing

- What does zero fee processing cost customers?

- Ongoing Legal Issues

- Lowering Credit Card Processing Fees

What Is Zero-Fee Processing?

Zero-fee processing or “no cost” processing is a processing solution where credit card processing fees are passed to your customers automatically. Instead of your business paying the processing costs, your customers will pay those fees.

Passing your processing costs to customers is known as surcharging credit cards, and is already an option you can choose regardless of your credit card processor. In the United States, surcharging is permissible in all but a few states as long as certain requirements are met.

While no-fee credit card processing is available with traditional processors, some companies are trying to create a business around offering “free” or “no-cost” processing, meaning that the processor will handle the setup of surcharging for you. This type of processor arrangement is primarily what I’ll focus on in this article.

Is there really no cost to me?

Not exactly.

With zero-cost processing, the majority of the costs will be covered by your customers, but there may still be costs to you, including monthly fees, PCI compliance fees, and more. For example, one company – Blue Yonder – charges a $65 monthly fee for processing. With some processors, you can choose to bundle the additional fees into the customer surcharge.

Additionally, surcharges can only be applied to credit cards. If your customer chooses to pay with a debit card, you’ll still incur the costs of processing that transaction, even if the card is “run as credit.” A debit card is always considered a debit card for processing purposes, and so it will incur debit card costs. (Contrary to popular belief, processing debit cards isn’t free.)

Lastly, you may have equipment charges. Some zero fee processors offer the option to lease credit card machines, which I strongly suggest not doing. Leasing will add monthly charges that far exceed the costs of purchasing a terminal outright.

Zero Fee Processing Considerations

Credit card processing isn’t cheap, and the idea of free processing is appealing. But there are some potential drawbacks to zero fee processing or surcharging. Since the costs are borne by your customers, you should ask yourself:

- Are competitors surcharging?

If not, how will you attract and keep customers when they’ll be expected to pay 2-3% more at your business? Will your competitors be able to use your surcharge against you?

- Can your goods or services be easily obtained elsewhere?

The internet makes it easy for customers to find somewhere else to make their purchases. Can customers purchase the same things you offer with little or no inconvenience? For brick and mortar, remember that major retailers like Walmart and Target don’t surcharge.

- Is your target market strongly against surcharging?

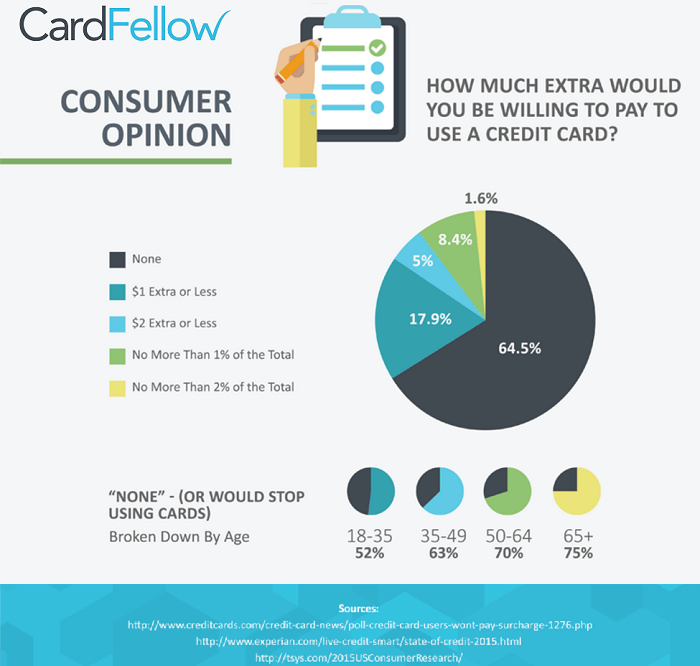

As shown in this infographic, 64.5% of people surveyed say they would stop using cards if surcharges are applied.

Surcharges can only be applied to credit card transactions, which might make customers consider using their debit card or paying with cash instead, resulting in lower costs than credit card transactions, but not eliminating your fees. It could have a bigger effect: customers may choose to go elsewhere. Some customers use their credit cards to get rewards, while others don’t carry cash. In those instances, customers may choose not to shop at your business rather than pay what they see as a penalty for using a credit card.

Differences Between Surcharging and Zero Fee Processors

You can choose to surcharge customers with almost any traditional processor. However, you’ll need to work with your processor and you’ll each handle parts of the set up. Your processor will need to reprogram your terminal to list surcharges as a separate line item on receipts, as well as ensure that only credit transactions are surcharged, and for the appropriate amount. You’ll be responsible for informing Visa and MasterCard of your intent to surcharge, as well as obtaining and displaying appropriate signage stating that your business surcharges.

With a zero fee processor, the company will generally handle all aspects of set up except for physically displaying signage, which will still fall to you. The main difference is that the zero fee processor handles notifying the card brands on your behalf, saving you the effort of filling out their forms yourself. Additionally, equipment is likely pre-programmed for surcharging. Some no-fee processors will even provide pre-printed signage for you to post at points of sale or other locations required by the card brands / state laws.

What does zero fee processing cost customers?

The charges will vary by processor, but cannot be more than 4%.

I reached out to Dynamic Payment Systems, one of the processors advertising free credit card processing. In actuality, the company charges a 3.45% flat fee for each credit card transaction. You’re allowed to either charge a 3.45% surcharge to customers or a 3.65% surcharge to cover additional monthly fees. (These monthly fees include a $5.00 admin fee, $6.99 PCI fees, and equipment leasing charges.)

3.45% is a fairly sizable markup for basic card-present transactions. Remember, your customers will see the charge on their receipt, and will be aware of it before a purchase. Adding 3.45% on top of their total may be a deterrent.

Related Article: Credit Card Processing Rates and Fees.

Ongoing Legal Issues

The ability to pass interchange fees on to customers as surcharges stemmed from a lawsuit.

Back in 2005, a class-action lawsuit was filed by merchants and trade associations against Visa, Mastercard, and other financial institutions that issue payment cards over interchange fees. The case is formally known as the Payment Card Interchange Fee and Merchant Discount Antitrust Litigation, docket 05-md-01720 in the United States District Court in the Eastern District of New York in Brooklyn.

Although the lawsuit was settled in 2013, lawyers representing big-box retailers like Target, Home Depot, Walmart, and Neiman Marcus have opposed the settlement, and as of September 2015, the case is being litigated in the 2nd U.S. Circuit Court of Appeals, as docket no. 12-4671.

It’s perfectly legal to pass these fees for now, but, with the case still sitting in appeal, this could change.

Additionally, as mentioned before, there are some states that prohibit surcharging, which also applies to surcharges passed on through zero-cost processing solutions.

Lowering Credit Card Processing Fees

You can lower your credit card processing fees without resorting to passing them on to customers. The first step is to ensure you price-shop credit card processors before signing up for one. That’s why CardFellow was founded.

Sign up for a free account here to receive instant quotes from leading processors and find the best processor for your business’s needs. Quotes you receive from CardFellow’s member processors are among the lowest you’ll ever see.

It’s also important to ensure all credit card processing equipment is operational to avoid manually inputting card information, which incurs higher fees. This also reduces the risk of fraud and chargebacks from the issuing bank.

Also, instead of passing fees to customers, you can impose minimum purchase limits for credit card usage. Only allowing credit card payments for purchases above $10 has the benefit of possibly upselling customers who may have spent less. It also saves you from paying fees on low-margin, low-value transactions that could bankrupt your business.

Cash Discounting is not surcharging and is legal in all 50 states and follows the rules set by the card networks.

The correct disclosures, etc must be followed.

That’s correct. However, zero-fee processing isn’t usually cash discounting. In a cash discounting program, the higher credit card price would be posted and then a discount for cash customers would be applied at the register. In most current zero-fee iterations, a fee is added at the register.

If I walk into a store and they have a sign that says a 3.2% discount has been applied to all prices for cash customers, any other form of payment will apply a 3.2 % to the total purchase.

That would be a cash discount or surcharge, depending on how they structure it. They’ll deduct 3.2% from the total if a customer uses cash (if the price posted is the credit price) or add 3.2% if a customer uses a card (if they price posted is the cash price.)

Is this an ad for CardFellow?

I’m not sure what you mean? You’re on the CardFellow website. This is an article in the CardFellow blog on credit card processing.

Hi Ellen –

I always enjoy reading your blog. Your information is always high quality and almost always correct.

In this case, there is an opportunity for more precision.

There is a big difference in the jurisdictional issues. What I have seen most writers (including you) say is that it matters where your business is located regarding whether you can surcharge.

What matters is where the item is being shipped and, if no shipping address (as in the case of soft goods) then the billing address of the cardholder. This is similar to the way sales tax is calculated if a merchant does not have a presence in a jurisdiction to where it is shipping and can waive the sales tax.

For small brick and mortar companies doing business in only one state, that’s pretty easy to manage. The moment you start wanting to surcharge customers from multiple states (and countries), for instance, any e-commerce company, things get much more complicated.

In addition, your state rather casually that a merchant is not allowed to markup a surcharge. That is not trivial. As you undoubtedly know, not even the interchanges can tell a merchant how much it will charge for any given transaction until after the folio closes. Thus, an estimate or an average generally means that the merchant is out of compliance and has over-collected on half of the transactions. There is, of course, no restriction on under-collecting, but the interchange rates for VISA cards alone can run into the hundreds of thousands of permutations and they can vary wildly based on the card brand and type which means the merchant could be leaving significant money on the table.

One last thing : A debit card transaction may be surcharged, but it is highly technical and difficult to do while remaining in compliance. Most experts conclude that it can’t be done logistically and state incorrectly that it is prohibited.

I’ve been looking at this problem for well over a year. We’ve built a solution. But, rather than promote my company on your site, I will just leave it at that you have my email address.

Thank you again for the great content. I have learned much from you. I’m sure that will continue.

Hi Robert,

Thanks for your comment. This article was written with the card-present merchant in mind; I apologize that it’s not clearer in the article, and we’ve updated that accordingly.

“In addition, your state rather casually that a merchant is not allowed to markup a surcharge. That is not trivial. As you undoubtedly know, not even the interchanges can tell a merchant how much it will charge for any given transaction until after the folio closes. Thus, an estimate or an average generally means that the merchant is out of compliance and has over-collected on half of the transactions.”

The surcharge cap is 4% or the actual cost of processing, but doesn’t preclude the processor’s markup from the cost. Visa specifies that the fee can’t be more than the merchant discount rate. That’s how many of these automatic surcharge companies handle this – they simply make the total cost for the merchant a fixed amount, often just under 4%. Then that’s the amount that they apply as a surcharge. You’re correct that it’s a little more complex when an interchange plus processor institutes a surcharge for a merchant.

“One last thing : A debit card transaction may be surcharged, but it is highly technical and difficult to do while remaining in compliance. Most experts conclude that it can’t be done logistically and state incorrectly that it is prohibited.”

Do you have a source for that? I’d be happy to update our information, but I’ve only ever seen explicit documentation stating that debit card surcharges are not permissible, even when ‘run as credit.’ Visa’s merchant surcharge FAQ is very specific about it: https://usa.visa.com/dam/VCOM/download/merchants/surcharging-faq-by-merchants.pdf

“I’ve been looking at this problem for well over a year. We’ve built a solution. But, rather than promote my company on your site, I will just leave it at that you have my email address.”

We’re always happy to look at including new solutions in our directories of services/equipment, so feel free to send me an email at ecunningham at cardfellow.com if you’d like to share more info about your company.

I know that it has to be posted if we are going to charge a fee but what about over the phone transactions? Is a verbal disclosure valid, or is there a rule for charging a surcharge for phone transactions?

Non face-to-face transactions may need to follow convenience fee rules. It would be best to consult a business attorney or your credit card processor for the specifics in your area.

I own a small medical office in CT where surcharging remains illegal. This law unfairly targets medical offices where co-payments and fees are contractually fixed. Meaning, if a patient has a $15 co-pay, I cannot adjust the price up to offset my costs, inflation, etc. If, for example I pay a .25 + 1.75$ on every transaction it really cuts into profitability. Credit/Debit cards now represent 70% of all revenues between check, cash & card. It is also noteworthy that one payer (Anthem BC/BS) has not increased their payments in 20+ years. Twenty years ago a relatively small % of over the counter monies came in the form of credit/debit cards. Now it’s the majority. In short, the medical community is being unfairly squeezed. If we were selling beanie babies we could simply increase our prices by 3% to offset the stranglehold placed upon us. We can’t. So our contractual payment fees are frozen in time, our costs of doing business and inflation continues to rise which makes it much harder for small business medical persons to give the best care and stay in business.