Discover and American Express both issue their own credit cards. When a cardholder initiates a chargeback on a Discover or Amex, the process works a little bit differently.

Ideally, you want to prevent chargebacks in the first place by properly utilizing anti-fraud tools and offering easy cancellations. But sometimes chargebacks happen anyway, and it’s important to know what to expect. In this article, we’ll explain the stages of the dispute process for American Express and Discover. You can also contact your credit card processor for assistance with specific chargebacks.

Looking for info on Visa and Mastercard? Check out our post What Happens When You Get a Chargeback, which focuses on Visa and Mastercard disputes.

American Express

In the past, American Express issued its own cards. No other U.S. banks provided cardholders with Amex. That has changed over the years, and banks like Wells Fargo, Citi, USAA, and Synchrony Financial offer Amex cards. However, Amex is still a large issuer of its own cards, and as such, you may deal directly with Amex when it comes to chargebacks.

However, if you’re on the OptBlue program, you’ll still go through your processor, similar to how you respond to Visa and Mastercard chargebacks.

OptBlue

In addition to acting as the card issuer, Amex previously provided businesses with merchant accounts. If you wanted to accept Amex, you had to go through Amex, even if you already had a processor for Visa, Mastercard, and Discover. That changed in early 2015, when American Express introduced the OptBlue program.

OptBlue is open to businesses that accept less than $1 million/year in American Express cards, and allows you to process Amex through your regular processor. That processor sets your rates over Amex’s wholesale costs, like they do for Visa and Mastercard, and they’ll assist you in providing documentation if you receive an Amex chargeback.

Amex has a reputation for siding with its cardholders, but that doesn’t mean that you can’t ever win a chargeback. It’s a good idea to keep careful records and consider using American Express SafeKey to cut down on fraudulent transactions before they progress.

American Express Chargeback Policy Changes

American Express claims that in response to business complaints about chargebacks, it implemented new policies that led to a large decline in disputes.

Perhaps one of the most notable changes was the implementation of a timeframe reduction. Amex has traditionally not put a strict limit for cardholders how long they can dispute a transaction. In late 2016, the company imposed a 120-day limit from the date of the transaction. (With exceptions for goods and services not received or for cancelled orders, as well as re-disputed transactions. The company also limited re-disputes to 2.)

Also in 2016, Amex in eliminated fraud chargebacks for missing signatures. In 2017 it began attempting to resolve disputes by customers not recognizing a transaction more thoroughly.

Dispute Process

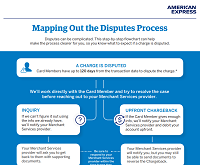

There are several possible phases to an American Express dispute. The company details them in the dispute process flowcart, below.

Click here to view full size.

As you can see, American Express has an inquiry phase, chargeback phase, and reversal possibilities.

Inquiries and Chargebacks

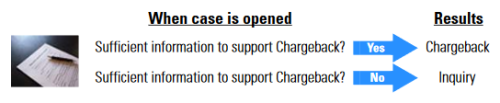

Where Visa and Mastercard refer to “retrievals” as the first stage of a dispute, American Express uses the term “inquiries.” Amex may send inquiries to businesses to request additional information about a disputed transaction. If you don’t respond in the allotted timeframe or if you don’t provide enough information, the inquiry will become a chargeback.

However, it’s important to note that Amex doesn’t always send inquiries before chargebacks. You may get a chargeback without going through the inquiry process. American Express’ Merchant Regulations explain that if Amex has enough information to support a chargeback, they will proceed right to a chargeback. If Amex does not have enough information to support a chargeback, they will send an inquiry.

If you’re part of Amex’s chargeback programs due to higher chargeback levels, you won’t receive inquiries first.

Notification and Deadlines

American Express notifies you of inquiries and chargebacks by mail and through your merchant account online dashboard. Amex explicitly states that it prefers you use the online system to send information and manage chargebacks, but it does accept documents by mail or fax.

Like Visa and Mastercard, Amex assigns reason codes to chargebacks. They start with a letter indicating the ‘type’ of chargeback. The most common reason codes you’ll see are A, C, F, or P, which refer to chargebacks due to authorization issues, cardholder disputes, fraud, or processing errors.

You’ll have 20 days to respond to an inquiry and 20 days to respond to a chargeback.

Chargeback Reasons

There are multiple reasons you could receive an Amex chargeback, ranging from submitting a charge that was more than the authorization amount to cardholder claiming they returned an item but didn’t receive a refund.

Amex’s Merchant Regulations document contains a good amount of information regarding specific chargebacks. The guide lists chargeback types, a description of that chargeback type, the information that Amex has if it proceeds with that chargeback, whether Amex requires sending an inquiry before proceeding to a chargeback, and – most importantly for you – the documentation you’ll need to provide if you intend to fight a chargeback.

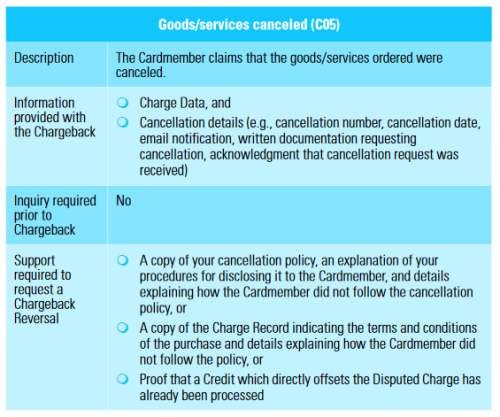

In the screenshot below, Amex details the information for a chargeback called Goods/Services Canceled.

The card brand explains that this chargeback occurs when an Amex cardholder claims that the product or service they ordered was cancelled. In such an instance, Amex states that it will be in possession of data on the original charge as well as details about the cancelled order, such as a cancellation number, acknowledgement of a cancellation request, etc.

If you chose to fight a “Goods/Services Canceled” chargeback, you would need to provide a copy of your cancellation policy and details on how the cardholder didn’t follow that policy or proof of refunding the customer for the order.

This is just one example of the chargeback types Amex lists in the Merchant Regulations. There are dozens of similar tables detailing the chargebacks you may receive.

Chargeback Reversal – Fighting a Chargeback

American Express refers to fighting a chargeback as “requesting chargeback reversal.” If you’re not in an Amex chargeback program, you can request a chargeback reversal and provide documentation to support your claim. As with Visa and Mastercard, Amex will look for “compelling evidence” when evaluating your chargeback dispute.

Compelling Evidence

American Express considers documents to be “compelling evidence” if they show proof of a card member’s participation in the transaction.

Such proof of participation varies depending on the type of transaction (card-not-present, recurring billing, etc.) but can include signed contracts between you and the cardholder, signatures upon delivery or pickup of an item, proof that the IP address making a digital purchase matches the IP address that downloaded the digital product, proof of a previous (undisputed) transaction shipped to the same address, and email correspondence about a purchase.

Fraud Recourse and Immediate Chargeback Programs

High risk businesses and businesses with a “disproportionate” amount of chargebacks may be placed into one of Amex’s Chargeback Programs. Under those programs, Amex will not send inquiries and you will not be able to fight the chargeback unless you can provide proof that you were not enrolled in the chargeback program at the time of the chargeback. Your only other option for “fighting” the chargeback is to provide proof you’ve refunded the customer and therefore don’t need a forced chargeback.

Defining “disproportionate:” Amex considers your chargebacks to be disproportionately high if your monthly ratio of disputed charges to gross charges is 3% or more in a 3-month period OR if your monthly ration of chargebacks is 1% or more in a 3-month period.

For Amex’s purposes, chargeback reversals do not count toward the 1% ratio.

Discover

Like American Express, at one point Discover was the only issuer of its cards. That changed in the mid-2000s and banks including HSBC and GE Financial have since issued Discover cards. However, Discover is still a large issuer of its cards, and disputes and chargebacks will often involve the card brand.

Discover has a dashboard for dispute resolution, which processors can use on behalf of businesses. Called the Discover Network Dispute System, it allows authorized users to view documentation about the dispute, upload images / documents to respond to a dispute, and view the status of the claim.

Discover’s system will show transaction details, cardholder details, and business details for each disputed transaction. Like American Express, Discover has traditionally not imposed strict time limits on cardholders for disputing a transaction.

Protections from Chargebacks

When used properly, some anti-fraud tools can help limit your liability for certain types of chargebacks or increase your chances of a successful chargeback dispute. In particular, proper use of AVS for address verification (including shipping only to matched addresses) and requiring the 3-digit code on the back of the card can help you build a case against chargebacks for fraud.

This is particularly important for situations of “friendly fraud.” Customers that place transactions intending to dispute them hope to receive the item they purchased and get their money back. Friendly fraud can be difficult to avoid (since the cardholder is making a legitimate transaction) so it’s important to have strong security tools in place that can help show that you did everything right.

Stages of a Dispute

As with Visa and Mastercard, Discover’s disputes consist of a two-step process involving a retrieval and a chargeback. A full chargeback then also has stages.

The initial step, which Discover called the Ticket Retrieval Request (TRR) essentially gives the choice between accepting the dispute or disagreeing with it. When disagreeing, you’ll need to provide supporting evidence for why you believe the chargeback to be invalid. (This can include proof of a refund already processed for the customer that initiated the dispute.)

When a TRR proceeds to a full chargeback, Discover will make a decision on that chargeback and notify you. At that point, either you or the issuer can appeal the chargeback decision, at which point it would proceed to arbitration.

Notification and Timelines for Response

Discover will send a letter for each phase of a dispute. Letters you may receive include:

- Ticket retrieval request

- Chargeback notifications

- Chargeback decision (called “representment decision”)

- Pre-arbitration request (if the representment decision is appealed)

- Pre-arbitration decision

- Dispute arbitration request for additional information

- Dispute arbitration decision

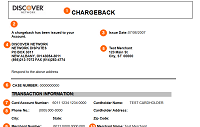

Each letter will list the details of the transaction and provide information on the phase of the dispute, as well as any actions that you’ll need to take. The sample letter below (a chargeback notification letter) explains “A chargeback has been issued to your account” in the top left.

Sample letters are provided for reference purposes only and may look different. If you have questions about the specifics of a dispute letter you receive, contact Discover.

The timelines for responding to each phase vary, so it’s important to work with your processor and/or Discover to ensure you’re providing requested documents before deadlines. For initial responses, you have 20 days, but if you’re working with your processor on the dispute, they may require documents sooner.

Appealing the representment decision must be done within 30 calendar days. If the issuer appeals, you’ll have 20 days from notification of the appeal to submit additional documents. In the event of a dispute arbitration request for additional information, you’ll have 45 calendar days to provide any new compelling evidence. Once Discover receives documentation from both parties, it will rule on the arbitration within 15 business days.

Timeframes for responses are provided as a guideline only and are subject to change. Additionally, your processor may have shorter deadlines.

Reason Codes

Discover provides “reason codes” to define the chargeback’s “category.” Reason codes will be included in the dispute letters you receive. There are a few dozen Discover reason codes, all two letters. The ones most businesses are likely to see include:

- AA (cardholder doesn’t recognize the transaction)

- AP (cancelled recurring payment)

- RG (goods or services not received)

- RM (goods or services not as described)

- UA## (fraud)

You may also see chargebacks with reason codes for authorization issues or processing errors.

Discover and Compelling Evidence

Of the four card brands, Discover publishes the least amount of information about evidence requirements for disputing chargebacks. However, the card brand does include a “merchant action” section in the dispute notification letters mentioned above, which will include documents that it requires related to the disputed transaction.

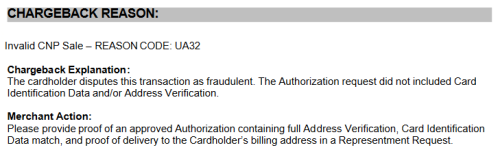

For example, in the chargeback notification letter linked above, we can locate the “merchant action” section, as seen in this snippet.

This sample chargeback includes a fraud reason code (UA32) and states that the authorization didn’t include the three-digit code on the card (Card Identification Data or CID) or address verification information. In order to fight the chargeback, Discover requests that the business provides proof of an authorization that utilized address verification and shows a CID match as well as proof of delivery to the cardholder’s billing address. (The address that AVS matched.)

AVS codes are stored along with other transaction details after a purchase, so you can locate the requested information in your gateway or transaction details logs. If you don’t know whether to find that information, you’ll need to work with your processor.

Additional Chargeback Defense

If you receive a lot of chargebacks or need additional assistance beyond what your processor provides, it may be worth considering a chargeback management company. However, such services aren’t free, so be sure to weigh the cost and benefits carefully.

Have you won a Discover or American Express chargeback? Let us know about your experience. Leave a comment below!