Fraud remains a thorn in the side of businesses, credit card processors, and customers. In fact, credit card fraud created losses in the billions every year.

There are several good techniques for fighting fraud, including biometrics and multi-factor authentication, but alone, they aren’t enough.

Instead, payment providers and the card networks need to dig into the vast amount of payment information that’s produced every day to find patterns that indicate likely fraudulent activities. They can then use this data to find and reject problematic transactions, creating a more secure payments ecosystem for everyone.

One way to extract and mine all of this information is through computing power, enhanced algorithms, and analytics. Using these systems can help experts explore the data and come up with risk assessments that can predict fraud in real time. This is known as machine learning, and processor First Data (now Fiserv) wants to use it to fight fraud.

What is Machine Learning?

In preventing credit card fraud, machine learning is a technique that uses historic data to “learn” the types of card transactions that are likely to be fraudulent. It does this by running complex data analysis, rules, and predictive modeling on credit card transactions. It combines this with human insight and labeling on transactions that turned out to be valid or fraudulent.

Using those findings, it can then create rules, models, and analysis that predicts if a specific card, used in a specific transaction, in a specific way, or from a specific person, is likely to be fraudulent. It establishes a set of “risk factors” and thresholds that apply to credit card transactions in real time, allowing businesses to accept or reject individual transactions.

These fraud detection techniques “learn” over time. Because card transactions are always being added to the historic dataset, machine learning can continually revise and update its rules based on all these new transactions, keeping the rules fresh.

The Benefits of Machine Learning

There are several benefits for to using machine learning for fraud detection. These include less need for internal teams, lower risk of fraud losses,

Less Need for Internal Teams Providing Fraud Detection

Identifying fraud can be messy, time consuming, and expensive. Machine learning helps to reduce dependency on manual fraud detection and analysts. Businesses can use their security and fraud budgets in more effective ways. It allows you to use human intelligence in the areas where machines can’t be effectively deployed, and use machines for more time-intensive, repetitive tasks.

Lower Risk of Fraud Losses

If you’re a business with small margins, every instance of fraud is a significant blow to your bottom line, since your product or service fixed costs are so high. If you’re processing 100,000 transactions annually, each of $40 ($4M), and 0.7% turn out to be fraudulent ($28K), reducing that by half could save you nearly $15,000. Machine learning can help cut fraud losses, benefiting your bottom line.

The Costs of Credit Card Fraud

If a business provides goods or services and accepts payment from a fraudulent card, either physically or online, they are typically liable for the costs of the products or services supplied. Additionally, the credit card company may impose fees for chargebacks and customer disputes.

There’s a bigger risk here too — if a business’s overall credit card fraud rate is over 1%, there’s a chance that the credit card networks like Visa, Amex, or Mastercard may refuse to allow them to accept credit cards. This could cripple a business entirely, since online businesses rely almost exclusively on card transactions, while traditional businesses can expect between 60% and 80% of all transactions to be via card.

Types of Machine Learning Used to Identify Fraud

There are a few different techniques security firms use to identify fraud. These include:

- Data about where and when cards are used, transaction amounts, the newness of a card, and whether it has been accepted or rejected before.

- Models and probability distributions for fraud; for example how often specific types of business are targeted by criminals.

- User profiles for the cardholder, including purchase and payment history.

- The age, history, and value of the credit card account.

- Pattern recognition and classification to find patterns and associations among groups of data.

- Algorithms that detect anomalies in card use, transactions, and other areas.

- Default and user-defined rules that impact whether a specific transaction would be marked fraudulent or not.

- AI and neural networks that are trained to spot erratic or suspicious card usage.

Implementing Machine Learning to Fight Fraud

There are several ways a business can take advantage of fraud detection. Some processors have their own tools built in to detect and reject erroneous cards. For example, both Stripe and PayPal have advanced fraud detection mechanisms. Alternately, a business can choose to use an external service like MinFraud.

These services typically have a “default” profile for rejecting obviously fraudulent cards. They also allow a certain amount of user customization, so you can setup your own rules for accepting and rejecting payments, based on criteria you specify. You should carefully review the rules you set — you do not want too many false negatives, resulting in you rejecting valid and good cards. Known as “false positives,” this happens when a legitimate customer with a credit card has that credit card refused or confiscated because the system erroneously believed it to be suspect. This causes not only the loss of the sale but also reputational damage with that customer.

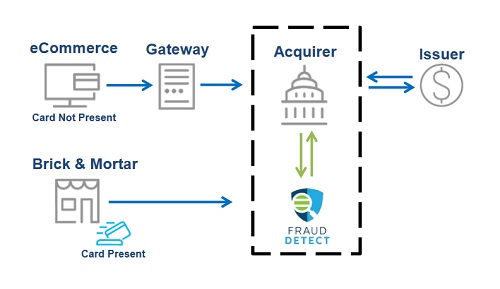

Fraud Detect by Fiserv

In the late 2010s, Fiserv acquired purchasing giant First Data, one of the largest credit card processors in the world, and its tools. This included Fraud Detect, a tool that uses machine learning to identify and prevent credit card fraud. When the tool was launched, First Data was in a powerful position to provide this information as they served around six million businesses and processed nearly 3,000 transactions a second.

That’s a very large data set to analyze and mine for potential risk and fraud. In addition to individual cards and user patterns, the service can detect which sectors and industries are currently most vulnerable to fraudulent activities.

First Data described Fraud Detect as, “…a comprehensive, state-of-the-art fraud prevention solution with real-time fraud scoring and machine learning capabilities designed to reduce a merchant’s overall exposure and cost of fraud.”

Fraud Detect comes in two main versions — a small to medium business offering, and a mid-market or enterprise offering. The small and medium business offering provides out-of-the-box fraud detection, but is lighter on customizable profiles and options. It gives businesses some basic control, reporting, and a case management system.

The mid-market and enterprise offering provides deep integration with a business’s existing platforms and allows for much deeper rules and profiles, together with extensive case management options. This includes device fingerprinting, behavior analysis, third-party integrations, scenario analysis, and bespoke implementation and configuration.

In short, Fraud Detect provides all the features businesses will need to dynamically reduce risk and control fraud.

How Fraud Detect Works

In addition to using machine learning and artificial intelligence, the Fraud Detect solution also brings in cybersecurity metrics and information from the “Dark Web,” where criminals buy and sell stolen credit card and identity information. The system works across multiple platforms including in store, online, on smartphones, and in applications.

The service provides a dynamic score on every transaction, indicating how trustworthy that particular card is likely to be. The higher the score, the more likely it’s fraudulent. In addition, the service focuses on avoiding false positives.

When it was released, First Data said one of the drivers for developing Fraud Detect is the rise of Internet of Things (IoT) devices. These are the various “smart” items we connect to our lives — fitness trackers, cars, alarm systems, traditional smartphones, and tablets. As the usage of these items grows, there is an increased risk of fraud across these “card-not-present” channels.

The aim is to provide “accept,” “decline,” or “review” recommendations for any card in less than a second.

Whatever machine learning solution you choose, implementing good fraud detection will help your bottom line, reduce chargebacks, lower your overhead costs, and promote trust from customers and the credit card networks.