As a small business owner, you may wonder if you can accept only debit cards or only credit cards. The short answer is yes, but there are rules you’ll need to follow and considerations before making that decision.

Let’s take a look at what you’ll need to do if you want to accept only one type of card.

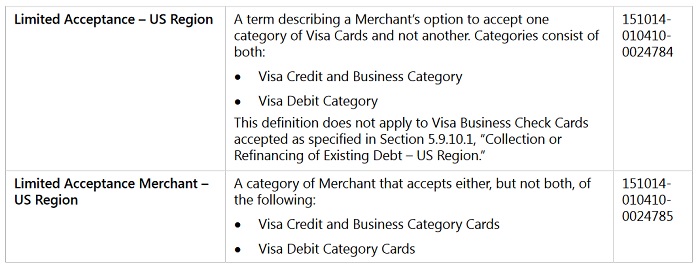

What is Visa Limited Acceptance?

The Visa Limited Acceptance program allows businesses to choose to only accept certain types of Visa cards. As you can see from this excerpt from Visa’s Core Rules, a business can choose to accept either Visa credit cards or Visa debit cards.

Note that it’s also possible to accept Visa credit cards and PIN debit cards without accepting signature debit cards. However, in some cases, doing so may be against other agreements with Visa. You’ll need to work with your credit card processor to ensure you’re set up correctly for the card types you want to accept.

Related Article: Walmart and Visa’s Legal Battle Over PIN Debit.

Mastercard Acceptance

Like Visa, Mastercard permits your business to only accept credit cards or only accept debit cards if you choose. Mastercard’s current US processing rules for businesses clearly state that you’ll have a choice of which cards you’ll accept.

As with Visa, there are rules you must follow, which are addressed later in this article.

Factors to Consider

When deciding if you’ll accept only credit or only debit cards, there are numerous factors to consider, including:

- Cost savings

- Customers’ preferred payment methods

- Competitors’ card acceptance

- Surcharging rules

The importance of each factor will depend on your specific business, your needs, and your customers. For example, if your customers prefer to pay with debit cards, that knowledge will be more important to your business than it is to someone whose customers don’t have a strong payment method preference.

Cost Savings

Keeping in mind that the actual processing cost of individual transactions can vary, a general rule is that processing debit cards will be cheaper than processing credit cards. If cost savings is your biggest priority, accepting only debit may be the way to go.

However, within debit cards are two authorization methods – PIN and signature. These two types of transactions come with different costs, meaning that sometimes the cheaper method is PIN and sometimes it’s signature. As a rough rule of thumb, signature debit will be cheaper on smaller transactions while PIN debit will be cheaper on larger transactions.

When determining your cost savings, be sure you have a solid understanding of which method is likely to result in the lowest costs for your business. (And whether your customers are comfortable with and likely to use that method.)

See also – Which is Cheaper: PIN Debit or Signature Debit?

Customers’ Preferred Payment Methods

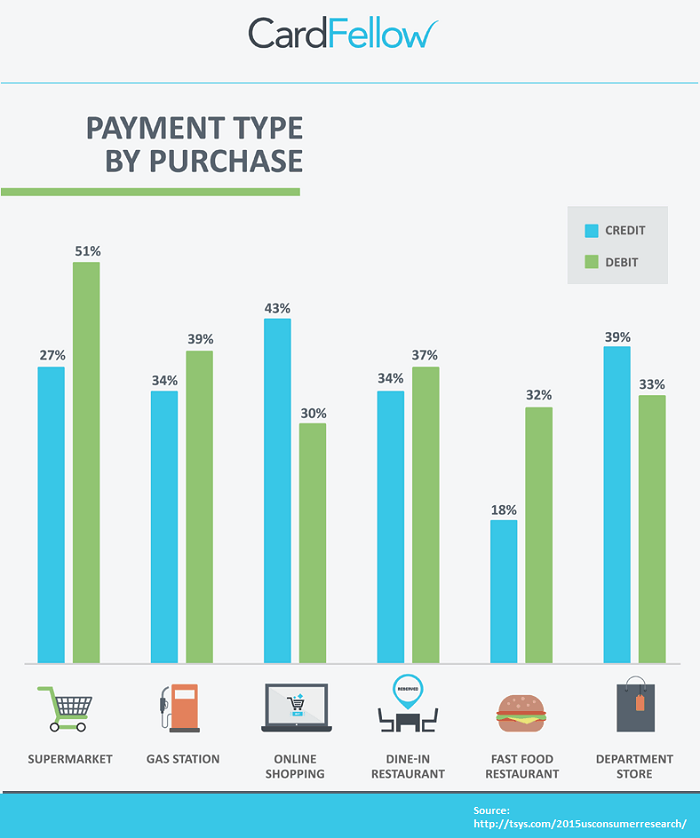

Another important factor is customer preference. Do your customers typically like to pay by debit card, or are they more inclined to go for the cashback rewards offered by credit cards? The TSYS Consumer Payment Methods study can help you by offering these stats on industry-based trends:

As you can see, for some industries, the split is fairly close. Department stores, dine in restaurants, and gas stations are fairly evenly split. Supermarkets and fast food restaurants skew more heavily toward debit as a payment preference, while online shoppers prefer using credit cards.

You can use these stats as a baseline for understanding the likelihood of debit or credit usage in your industry, but be sure to look at your specific business’ typical card mix.

Competitors’ Card Acceptance

What about your competitors? Do they accept all types of cards? Remember to think not just local, but online as well. How easy is it for customers to go elsewhere if they don’t like your card acceptance policies? Is your product or service likely to be purchased locally, meaning customers may have more tolerance for payment method requirements, or are you competing with online retailers and auction sites?

Answering these questions can help give you insight into whether it makes sense to limit acceptance of certain payment types.

Surcharging Rules

Surcharging, or adding a fee for using a credit card, became permissible in 2013. However, some states prohibit the practice, and no businesses are allowed to surcharge debit cards. Note that even when a debit card is “run as credit,” you can’t add a fee.

If you’re in a state that permits surcharging, you can consider whether that makes sense for your business. Some businesses may want to only accept credit cards so that they can apply the surcharge to all credit cards (that is, all their card sales) thus recouping all processing fees. By limiting acceptance to just credit cards and surcharging, they would not pay processing fees. If the business accepted debit cards, they would pay fees for that acceptance, as debit cards cannot be surcharged.

If you’re in a state that doesn’t permit surcharging, you could consider taking only debit cards to help curb your processing costs, since debit cards are often lower cost to process than credit cards.

See Also: Can Businesses Charge for Using a Credit Card?

Accepting Debit Cards Only

It may be less expensive to accept only debit cards. Credit cards are typically more expensive to process than debit cards, so if cost is your concern, limiting to debit cards could boost your bottom line.

Debit cards cannot be surcharged. If a customer chooses to pay with their debit card, you can’t add a fee. Some states prohibit credit card surcharges as well. In states that prohibit all surcharges, accepting only debit cards can be a way to lower processing costs.

Additionally, card-present businesses that accept only debit cards may have a reduced risk of chargebacks, as consumers may have a harder time proving the card was used fraudulently, especially if a PIN was entered at the point of sale.

However, some customers prefer to use credit cards. Rewards programs have become very popular, and some customers use their credit cards for all their common purchases.

Accepting Credit Cards Only

In most cases, accepting credit cards will not be less expensive than accepting debit cards. An exception is for small transactions (under ~$10) if your customers pay with regulated debit cards. (A debit card issued by a bank with $10 billion or more in assets: Wells Fargo, Bank of America, Citi, etc.)

You can read more about why regulated debit is expensive for small transactions in our article Small Tickets: The Durbin Downside.

Another reason a business may consider accepting only credit cards is so that they can surcharge all card transactions in order to recoup processing costs. Since debit can’t be surcharged, a business accepting debit but surcharging credit would still have to pay processing costs for the debit transactions. By eliminating debit acceptance, the business could surcharge all card transactions.

Businesses that bill customers on a recurring basis, such as for memberships or subscriptions, may want to consider only accepting credit cards due to reduced risk of declined transactions. If a customer forgets about their subscription and doesn’t have enough money in their bank account, a debit transaction may be declined.

Possible Drawbacks

While there are benefits to Limited Acceptance, there are also potential drawbacks to each type of limited acceptance.

For Debit Only

Many customers prefer using credit cards, especially for large purchases. Credit card rewards, chargeback protection, and security of not using a card connected to a bank account all mean that many consumers prefer credit when paying with plastic. This is especially true for online purchases.

For Credit Only

The primary drawback for accepting only credit cards is that they’re typically more expensive to process than debit cards. If cost savings is your goal, accepting only credit may not be the best choice. Additionally, accepting only credit cards may mean a slightly higher risk of chargebacks.

You could also consider a compromise, such as accepting credit cards and PIN debit cards, but keep in mind that customers tend to use debit cards for small transactions, which is when it’s typically more expensive than credit cards. Consider your average transaction size when determining which debit method is likely to be most cost-effective.

Visa Rules

In Visa’s Core Rules and Regulations document, certain requirements are laid out for Limited Acceptance businesses.

- Your processor must register you with Visa as a Limited Acceptance Merchant and provide reporting to Visa as requested.

- You must also accept any Visa cards issued by a non-US bank.

- You must use Limited Acceptance signage at your business and not display Visa signage indicating that you accept all Visa cards.

Visa doesn’t provide specifications for Limited Acceptance signage on its website or in its Core Rules. We’ve reached out to Visa for further information and will update this article as details become available.

Visa’s rules are subject to change at the company’s discretion. Your processor can advise you of updates if you’re a limited acceptance merchant.

Mastercard Rules

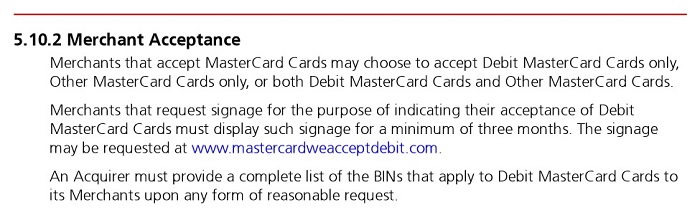

Mastercard has fewer published rules than Visa regarding limited acceptance, and even its signage comment doesn’t specify that it’s a requirement. As you can see from the screenshot from Mastercard’s Rules below, the credit card brand simply states that if a business requests signage to indicate that they only accept debit Mastercards, the signage must be displayed for at least three months. Mastercard provides a website where signage can be requested.

Mastercard further notes that acquirers must provide businesses with a list of BINs (or bank identification numbers) that apply to debit Mastercards upon request. In 2017, new Mastercard BINs were introduced and some businesses may need to update their BIN information.

Finding a Processor to Implement Limited Acceptance

Any processor should be able to set up your processing account for Limited Acceptance. The application you fill out may even include the option to note what types of cards you’ll accept, breaking it out by card brand and by card type.

Many businesses that consider Limited Acceptance are hoping to lower their costs for processing, but that’s not the only way. Before deciding on Limited Acceptance, check to see if you’re overpaying. Processing cost comparison tools – like CardFellow’s free quote tool – can show you pricing from multiple processors, all customized to your business. We’ll even help you compare it to your current pricing.

CardFellow clients save an average of 40% on their processing costs, without even choosing Limited Acceptance. Try it now!