If you want to expand your business, create a new product line, hire more staff, or scale in some other way, you need money to make it happen. Traditionally, businesses would use a standard business loan or a credit card to fund their expansion plans.

PayPal Working Capital aims to change that. It’s a different approach to borrowing money and repaying your loan using a percentage of each PayPal payment you receive.

In this review, we’ll explore PayPal Working Capital and compare fees with other types of financing so you can see if it’s right for your business.

PayPal Working Capital in Its Own Words

“PayPal Working Capital gives businesses access to the capital they need, but it’s faster and easier than traditional loans. It’s available to select businesses that already process payments through PayPal.”

PayPal Working Capital lists the key benefits as:

- Flexible payments, taken as a percentage of PayPal sales amounts

- An up-front fixed fee, rather than periodic interest charges

- No credit check – loan eligibility is based on PayPal sales amounts

- Fast funding, typically credited to your PayPal account in minutes

Eligibility for PayPal Working Capital

Here’s what you need to get a loan from PayPal Working Capital.

- Live in the US, the UK, or Australia.

- Have a PayPal Premier or Business account that’s over three months old.

- For Premier accounts, process at least $20,000 in payments through PayPal per year.

- For Business accounts, process at least $15,000 in payments through PayPal per year.

- Not have an existing PayPal Working Capital loan.

Maximum Borrowing Amounts

If you are eligible for PayPal Working Capital, what you can borrow depends on a few factors, but can range from $1,000 – $150,000 (for new customers) or up to $250,000 or repeat customers.

PayPal has previously stated that the breakdown works out to borrowing up to 18% of the total value of payments processed through PayPal over the previous 12 months. For example:

- $15,000 processed — $2,700

- $25,000 processed — $4,500

- $50,000 processed — $9,000

- $80,000 processed — $14,400

The most that PayPal Working Capital will lend you is $97,000, which would require $540,000 of PayPal payments in 12 months.

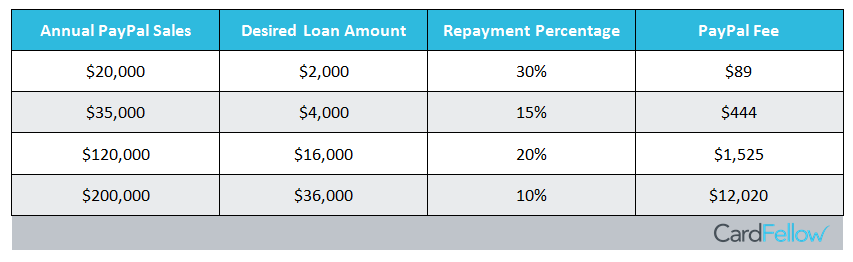

Fees for PayPal Working Capital

PayPal Working capital does not charge interest in a traditional way. Instead, they charge an upfront, fixed fee, which is repaid together with the balance of the loan. Repayments are made by deducting a portion of each PayPal sale, and applying it to the outstanding balance.

There are no periodic interest charges, monthly bills, late fees, prepayment fees, penalty fees, or any other fees. Here are some estimated fees based on annual PayPal sales, how much you want to borrow, and how much of each sale you want to use to repay the loan balance.

The fee charged is based on:

- Your business PayPal sales history

- The amount you are borrowing

- The repayment percentage you choose to make — A higher percentage results in a lower fee, and vice versa

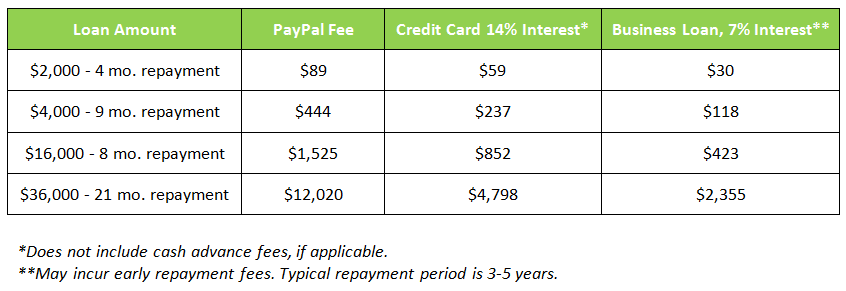

PayPal Fees Compared to Credit Card and Traditional Bank Loan Fees

Here’s how PayPal’s fees stack up against other types of loans.

Clearly, PayPal Working Capital’s fees are substantially higher than borrowing the same amount and paying it off in the same timeframe for a credit card or business loan. However, those types of loans may attract cash advance or early payment fees. Additionally, small business loans may have more stringent eligibility requirements. Be sure to consider all factors when deciding what type of funding is right for your business.

Related Article: Pros and Cons of Working Capital Cash Advances.

Repaying a PayPal Working Capital Loan

PayPal automatically deducts repayment from your PayPal account balance as a percentage of each sale, as the sale occurs. You can choose the percentage of each sale you want to dedicate to repaying the loan. Repayments continue until you repay the outstanding loan balance and PayPal Working Capital fees in full.

The repayment is applied after PayPal’s processing and transaction fees are deducted. Note that those fees are not included in the repayment percentage calculation. However, if taxes or shipping are included as part of the payment, that money will be included in the repayment percentage calculation. Basically, as your sales volume changes from day to day, the amount you repay to PayPal will vary as well.

Repayments start four days after you receive the loan.

Sales not made through PayPal do not have any influence on the loan amount you may receive, repayment terms, or any other aspect of the loan. PayPal does require you to continue processing payments through their systems.

For international payments made in foreign currencies, PayPal will apply their standard currency conversion exchange rates and deduct the amount owed in US dollars. Standard PayPal currency conversion rates and fees will apply.

You can also make manual repayments on the loan and repay it in full early, with no extra fees, if you wish.

Once you choose your repayment percentage, you can’t change it, so it’s worth thinking very carefully about how much you choose to repay from each payment.

What PayPal Working Capital Classifies as Payments

PayPal considers all payments you receive as sales except for transfers from your linked bank, PayPal and other accounts, or personal payments. Any other loans or cash advances deposited into your PayPal account are not considered sales when it comes to making repayments.

If sales are returned and a refund is made to the customer, PayPal Working Capital will not refund the repayment amount.

Minimum Repayment Amounts

PayPal Working Capital has a minimum repayment requirement of either 5% or 10% of the total loan amount every 90 days, for the first 540 days of the loan. For example, if you have borrowed $20,000 ($19,000 loan balance plus $1,000 fixed fee) you will need to repay $1000 – $2,000 every 90 days for the first 540 days of the loan.

In most cases, that is not an issue, as automatic PayPal repayments cover these amounts. If for some reason PayPal payments do not cover the minimum amounts, you can make a manual payment to keep the loan in good standing.

Impact of Defaulting

If you are not able to meet the minimum repayment amounts and your loan goes into default, two things may happen:

- The entire balance could become due

- There may be other limits placed on your PayPal account

- PayPal could collect the remaining loan balance and fees directly from your PayPal account, without your consent

- PayPal could debit the amount owed to them from any funding sources linked to your PayPal account

Applying for a PayPal Working Capital loan

You simply need to login to your PayPal account on the PayPal Working Capital website. You do not need to change anything about how you receive PayPal payments, how you charge customers, or any other aspect of your PayPal service. PayPal automatically deducts repayments from your sales.

The application typically takes five minutes, with funds received in a few minutes if you are approved. Additionally, there is no need for a personal guarantee.

Impact on Your Credit Score

There is no impact to an individual’s or business’s credit score when applying for or receiving a PayPal Working Capital loan. Your PayPal sales history determines eligibility.

PayPal Working Capital Reviews

We examined multiple reviews of PayPal Working Capital to get a feel for customer opinion of the service.

What we found is that customers have mixed opinions. Several reviewers enjoyed the ability to choose their own repayment percentage, which worked with the profit margins of their businesses. Additionally, they were happy that if they didn’t receive payments over a period of time, there was no need to repay that money, outside the minimum 90-day repayment requirements.

Related Article: Calculating Margin.

Other reviewers were happy that the application process was fast and easy, and that they got access to funds almost immediately. However, some reviewers expressed frustration that PayPal turned them down for loans, sometimes on multiple occasions. Additionally, the loan amounts vary greatly.

Alternatives and Conclusion

Remember, PayPal isn’t the only choice for funding, nor the only working capital-style funding source. Check out our OnDeck vs. Kabbage Review to get a feel for other services.

If you regularly receive payments through PayPal and want fast, easy access to money, PayPal Working Capital can sometimes be a good choice. However, their fees are not at all competitive when compared to credit cards and traditional business loans. That said, you do get the flexibility of making repayments only when you get paid. You should weigh your need for funds with your repayment terms, profit margins, and comparable fees from other providers to decide if PayPal Working Capital is right for you. You can also visit Kabbage or other services directly.

Have you used PayPal Working Capital to fund your business? What did you think? Let us know in the comments!