Now that credit and debit cards have become a popular way to pay for meals, customers often add tips for servers when they sign their credit card receipt. However, this common practice could have implications for your bottom line.

Tips over a certain percentage of the bill can trigger flags for fraud, resulting in card issuer-initiated chargebacks, or can cause your transaction to be downgraded to a more expensive interchange category.

Tip Tolerance

When credit and debit cards are swiped in a restaurant, the amount authorized includes a 20% “tip tolerance.” This means that when you swipe a customer’s card, it will be approved if the customer has funds available for the total cost of their bill plus 20%. For example, if a customer’s bill is $100, the actual authorization amount will be $120. This is done to ensure that there are enough funds available for the possibility of a customer leaving a 20% tip.

In some cases, customers tip more than 20%. If they do, the transaction may set off a warning (“flag”) to the issuer to check for fraud. The issuer could decide to initiate a chargeback, requiring information from your business about the transaction to determine the validity.

Issuers initiating chargebacks for small checks or for tips close to 20% isn’t very common, but it can happen. Tips that are much larger than 20% are more likely to be subject to a card issuer chargeback. Dealing with chargebacks can be time-consuming and cost you money, so it’s best to avoid them in the first place if at all possible. Visa provides a best practices guide for restaurant staff to help ensure smooth card acceptance.

Related Article: Understanding and Handling Chargebacks.

In 2016, Mastercard eliminated tip tolerance for several transaction types, including chip and PIN, card-not-present, and contactless payments like Apple Pay. A 20% tip tolerance is still available for card-present transactions that are NOT chip and pin or contactless. This means a large number of chip cards WILL still have a tip tolerance, as not all chip cards are chip and PIN. Many chip cards issued in the United States are chip and signature and thus still eligible for the 20% tip tolerance.

If preauthorizations are done for an estimated amount, MasterCard also requires a second authorization for the actual total. Skipping the second authorization could lead to an issuer-initiated chargeback.

What happens if I get a chargeback for a big tip?

If the issuer initiates a chargeback for a tip over 20%, the only thing you can do is respond to requests for information promptly and thoroughly. Providing documentation that the transaction is valid (such as a signed credit card receipt with the tip amount) may help the issuer determine that the transaction isn’t fraudulent. Work with your credit card processor to provide all required information on or before deadlines for the best chance of a favorable outcome.

Tips and Interchange Downgrades

A more common and expensive issue with big credit card tips is the possibility of an interchange downgrade. Interchange fees are the biggest component of credit card processing costs. Every transaction you process is charged according to an interchange category. Many different factors affect which interchange category a transaction will fall into. A downgrade means that a transaction is routed through a more expensive interchange category, resulting in a higher cost for you.

For tips under 20%, the transaction will usually fall into an interchange category based on the card type and input method. It may be a swiped credit card, swiped debit card, etc. and you’ll pay the interchange associated with that category. However, if a tip is over 20%, the transaction can fall into a more expensive “catch-all” interchange category.

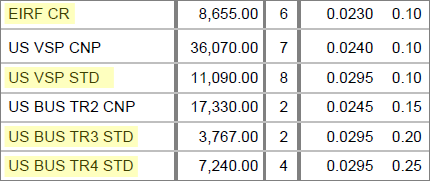

Spotting Downgrades on Your Statement

Credit card processing statements aren’t in a consistent format across the board, which can make it challenging to spot every downgrade. For a general idea, look for the words EIRF or Standard (or variations like STD), which indicate a downgrade. The image below shows what a downgrade might look like on some statements.

If you chose a processor through CardFellow, our service to you includes looking for and correcting downgrades when we conduct account reviews on your behalf. If you haven’t had an account review and think you’re paying too much, please contact us for a review.

Read more about Interchange Downgrades.

How can I avoid interchange downgrades?

Many things affect what interchange category a transaction is routed through, but usually it has to do with how you process a card, and what type of card it is. Generally speaking, debit is less expensive than credit, swiped is less expensive than keyed, and so on. This is one of the few situations that it’s not really your fault if your large-tip transaction is routed through a more expensive category.

Unfortunately, there isn’t much that can be done to minimize an interchange downgrade for this type of transaction. Instead, you can focus on ensuring that the transactions you can control are routed through the lowest possible interchange categories for their type. That means processing transactions according to the requirements to qualify for the lowest cost interchange categories.

When you choose a processor through CardFellow, we monitor your account to ensure interchange optimization to help you get the best possible processing solution. Try it.

EMV Chip Cards and Tipping

The EMV liability shift means that more businesses are accepting EMV chip cards and more customers are using them. But one thing to keep in mind is that the new EMV chip cards could affect how restaurants accept tips. Chip cards may require a shift in tipping procedure due to how chip cards are processed. Some machines and processors don’t allow you to adjust the transaction total for a tip after the card has been removed from the machine.

Be sure to check that the machine you use (or are considering) will allow for tip adjustments and that your processing company supports that machine.

Related Article: Can an employer legally deduct processing fees from servers’ tips?