Commercial Standard previously referred to a Visa interchange “downgrade” category, but now refers to something else entirely.

In the past, Visa Commercial Standard meant that when a commercial card was used but it didn’t meet criteria for its “target” interchange category, it “downgraded” to a more expensive category. For commercial credit cards, “Standard” was that downgrade.

However, at this point, the only Commercial Standard category applies to international cards. So what happened to Commercial Standard? It became “Non-Qualified.” For more information, check out our article on Corporate Non-Qualified.

The rest of this article refers to Commercial Standard for international transactions – that it, for transactions that take place in the United States with a card that was issued outside of the United States.

Commercial Standard Interchange Rates

Visa publishes the rates for all its interchange fee categories. The following interchange fees come directly from the Visa interchange table and are subject to change at Visa’s discretion.

| Volume Rate | Per-Transaction Fee | |

| Commercial Standard | 2.00% | $0.00 |

In the “criteria” section below, we’ll take a look at when these categories will apply to commercial transactions.

Commercial Standard Interchange Requirements

It’s a bit misleading to call the criteria “requirements” as Standard interchange applies when you haven’t met requirements for other categories. However, for simplicity’s sake, we’ll call it requirements to qualify.

For commercial standard interchange, the transaction:

- Used an international credit card (issued outside of the United States)

- Does not meet CPS requirements

- Does not pass enhanced data

There are no business type restrictions for commercial standard interchange. Any business that accepts a commercial card (including corporate cards, purchasing cards, and business cards) can “downgrade” to commercial standard.

Lastly, any type of commercial card can be subject to the Standard downgrade. That includes corporate, purchasing, and business credit, debit, and prepaid cards.

Understanding Commercial Interchange

Commercial card interchange is a little different than consumer card interchange. For one thing, commercial cards are eligible for lower costs if you provide extra information that normally isn’t included, like a purchase order number and tax rate.

If you don’t supply the extra information (called “enhanced data” or level 2 / level 3 data) you won’t receive the lower rates. However, that’s different than receiving penalty “downgrade” rates.

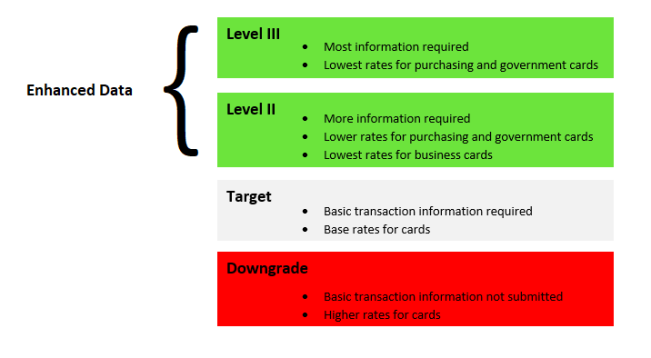

Think of it this way: If you only provide the basics for a commercial transaction, you’ll hit the “target” or base interchange qualification. Those rates will be the middle of the road cost for that transaction.

If you provide level 2 or level 3 data, you can hit “enhanced” interchange. Those rates are the best (least expensive) you can pay for that transaction.

If you don’t provide level 2 or level 3 data AND you fail to meet the basic requirements for “target” interchange, you’ll “downgrade” to the Standard interchange category. Those rates are the worst (most expensive) you could pay for that transactions.

This concept is summed up in this diagram:

As you can see, “target” interchange is neither an enhancement nor a punishment. But choosing to provide more info can result in enhanced interchange qualification, meaning lower costs. By contrast, not meeting requirements for “target” interchange can result in a downgrade, meaning higher costs.

Do I need to provide enhanced data?

If you accept a lot of commercial cards, it’s in your best interest to qualify for enhanced data rates. But even if you can’t / don’t want to take steps to provide enhanced data, you’ll want to ensure you’re not receiving lots of downgrades. That indicates you’re essentially paying a penalty rate.

CardFellow members can get assistance with interchange qualification and downgrade correction by contacting us for your free audit. You can also become a CardFellow member for free if you aren’t already.

Commercial Standard on Statements

You can usually identify Standard interchange on statements. Many processors provide statements that include a section for “interchange detail.” That will list the categories that applied to your transactions for the month.

However, flat rate processing companies (such as PayPal, Square, Stripe, and others) don’t list interchange for you. You will not be able to see which individual interchange categories applied.

Different processors use different terms or abbreviations for interchange categories. Some of the ones you might see for Commercial Standard include:

- STND PURCH

- STND BUS

- STND CORP

- STND BUSDB

- STNDCOMMPP

The first three refer to commercial credit cards while the last two are debit and prepaid. However, this is not a complete list of all possible aliases.