In the latest accusation against Wells Fargo, the company’s merchant services division is facing a lawsuit that alleges misleading sales tactics, expensive cancellation fees, and overbilling, including mislabeling some of its own fees as interchange.

Let’s take a look at what the lawsuit claims and what you can do if you process credit cards through Wells Fargo Merchant Services.

Wells Fargo Lawsuit

The lawsuit – Patti’s Pitas et al v. Wells Fargo Merchant Services – filed in August 2017 in New York, alleged that Wells Fargo charged unauthorized fees and failed to deliver on promises that included transparent pricing, no monthly fees, and no cancellation fees. It further claims that the “deceptive language” of monthly statements disguises the fees and that an excessive 63-page merchant agreement includes fine print that could not be fully read or understood by busy business owners.

According to Reuters, the lawsuit was filed on behalf of businesses in North Carolina, Pennsylvania, and other states and claims that hundreds of thousands of businesses may have been affected over the past six years.

Wells Fargo’s Response

In a statement, Wells Fargo’s spokesperson denied the claims made by the lawsuit and said that the company plans to defend the “misrepresentations” that the lawsuit makes.

First Data’s Role

Wells Fargo offers credit card processing in conjunction with First Data (now Fiserv), one of the largest credit card processors in the United States. First Data declined to comment on the lawsuit.

It’s important to note that not all First Data / Fiserv accounts are with Wells Fargo. If you use First Data / Fiserv for credit card processing and did not go through Wells Fargo to secure it, you may not be affected by these allegations.

It doesn’t hurt to check your statements and compare your pricing, though. If you want to see if you’re paying more than you need to for credit card processing, use our quote comparison tool to get baseline pricing, and then give us a call to help you analyze your current statement. Try it now!

2021 Settlement

The $40 million class action lawsuit was settled with final court approval in July 2021. Wells Fargo did not admit wrongdoing and the courts did not “rule” in favor of either party – the settlement means that both parties agreed to a settlement as a way to end the suit.

Does this affect you?

The big question for most business owners is: does this affect me?

It’s too late to receive payment from the settlement if you have not already done so, but if you’re with Wells Fargo for credit card processing, it’s possible that you could be experiencing over-billing.

At CardFellow, we’ve examined a number of Wells Fargo merchant services statements over the years and have seen many instances of expensive or misleading rates and fees. Below are some examples to help you determine if you’re in the same boat.

What to Look For

It can be tricky to understand complex processing statements. Here are specific things you can look for to help determine if you may be overpaying for processing with Wells Fargo.

Tiered Pricing

As we note in our Wells Fargo Merchant Services review, the company favors all forms of bundled and tiered pricing, such as the billback model noted below. Tiered pricing is the least transparent and often the most expensive. This statement snippet shows how Wells Fargo’s tiered (qual, mid, non) pricing appears.

Look for: Words like “mid-qual,” and “non-qual” on your monthly processing statement.

Read more about tiered pricing.

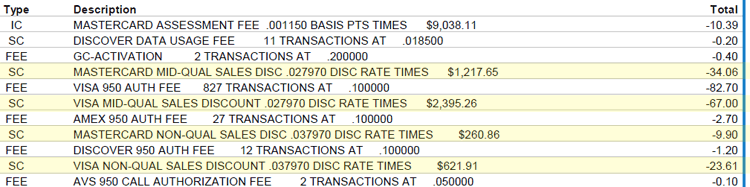

Excessive Bundled Rates

Like all processors, Wells Fargo Merchant Services sets pricing on a per-case/per-business basis. However, Wells Fargo has a tendency to price businesses very aggressively, often using bundled pricing with “qualified” rates at or above 4%. The statement snippet below highlights a qualified rate at 4.2%.

Look for: The “sales discount” and the associated rate.

In the snippet above, the rate is expressed as the decimal .042000, which equals 4.2% when expressed as a percentage.

Billback Pricing

Wells Fargo is well known for using what’s called billback pricing, which results in expensive processing and opaque reporting. Billback can be recognized on a statement by charges from a previous month being shown on the current month’s statement. For example, this image shows charges from January (JAN) on a February statement.

Look for: Previous months’ charges (going back two or even three months) on your current month’s statement.

Interchange Clearing Fee

Another Wells Fargo tactic is charging an “interchange clearing fee.” Regular CardFellow readers will remember that “interchange” is the component of processing costs charged by banks that issue credit cards and it’s non-negotiable. Since the fee Wells Fargo charges has the word “interchange,” many businesses mistakenly believe that it’s one of those non-negotiable interchange fees. In reality, it’s a Wells Fargo markup masquerading as an interchange fee.

Look for: The words “Interchange Clearing Fee” in your processing statement.

You can also read more about the fee and see examples in our article on Wells Fargo’s interchange clearing fee.

Excessive Interchange Markup

Wells Fargo frequently charges excessive interchange markups. The statement below shows a markup of 180 basis points, plus a 20 basis point “interchange clearing fee.” The result is a net 200 basis point (2%) markup to WF before any base costs are paid.

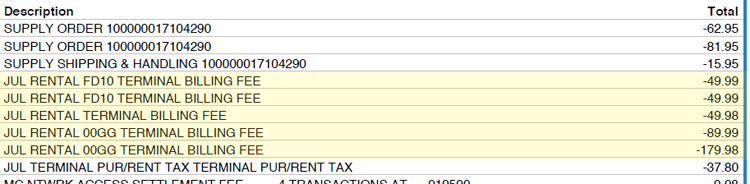

Equipment Rental and Leasing

In addition to expensive processing, Wells Fargo leases or rents equipment at highly inflated pricing when compared to purchasing the same equipment outright. This statement snippet shows inflated rental pricing. Note that if a business leases equipment the processor doesn’t show those charges on your usual processing statement, as the lease is a separate agreement.

Look for: A separate statement with an equipment charge, which may include the word “terminal” and the model. In the snippet above, the business leases an FD10 credit card machine.

What to Do if You’re Overpaying

If you compared your statement to the examples above and found indications that you’re being overcharged, the first thing to do is confirm your suspicions. Follow the steps below if you’d like assistance from CardFellow:

- Get baseline pricing

Take 2 minutes to set up a business profile where you’ll get baseline pricing. This will give you a better idea of what you could be paying with a different processor. (Don’t worry, it’s free, no obligation, and we don’t give out your contact information.)

- Request a statement review

Once you have your baseline pricing, contact us (by email, phone, or livechat) to request a statement review. We’ll ask for your most recent processing statements and will go over them with you to determine if you’re overpaying, and by how much.

- Decide if you’ll switch

With the CardFellow statement review, you’re never under obligation to switch processors. We’ll show you how your current pricing stacks up, and if you’d like to switch, we can help you do that.

Find out if you’re overpaying by setting up your free business profile. Try it now!