If your business has bundled credit card processing fees, your processor is pocketing your fee credits every time you issue a debit or credit card refund. Are you in an industry that regularly accepts returns and issues refunds like clothing and shoe stores, general merchandise retailers, or electronics stores? This affects you.

Luckily, plugging the cash flow leak is possible by getting interchange pass through pricing instead of bundled pricing, and knowing what to look for.

You don’t have to worry about losing money on credit card refunds if you found your processor here at CardFellow. We don’t allow processors to structure pricing in such a way that allows for this hidden charge, and we require your processor pass refunds to you. If you aren’t a current CardFellow client and want to know if your processor is pocketing your credits, sign up for a free account and contact us for assistance.

Do processors return fees when I give a customer a refund?

Some do, some don’t. In the open market, there’s no requirement that processors return the processing fees on refund transactions.

PayPal Doesn’t Return Fees on Refunds

In 2019, PayPal announced a change to its fee policy. In short, when you refund a customer through PayPal, you will not receive any of the processing fees you originally paid on the transaction.

This is not limited to PayPal. In fact, many processors keep your fees. Don’t make the mistake of thinking that just because you switch from PayPal that processors will automatically return fees. In reality, you need to be on a pricing model that passes those fees back to you, and with a processor that doesn’t simply pocket your refund fees.

Interchange Charges & Credits

So, how do fees on refunds work, anyway?

Visa and Mastercard use interchange fees to determine how much you pay an issuing bank each time you accept a credit or debit card. Interchange is also used to determine how much money you get back on your processing fees when a customer returns the product they purchased. Meaning, the amount you get back isn’t the same as the amount you paid. In other words, refund fees are not a 1:1 with the original transaction fees.

You should be able see the evidence of returned fees in the form of interchange credits on your monthly credit card processing statement. Interchange credits will look similar to this sample from a business we recently helped here at CardFellow.

In this snippet, the client received credit for the fees they paid on transactions that they refund. The transactions are labeled starting with “Refund.”

By receiving interchange credits, this one section shows a savings of $27.39 for the business. For clothing and shoe stores, processing refunds regularly, the numbers could be much higher. If you don’t you see any credits on your statement, and you know you issued refunds during the month, your processor is pocketing your fee credits and you’re losing money.

Note that not all statements label interchange credits the same way. Be sure to look for abbreviations and variations of the words.

Related Article: How to Read a Credit Card Processing Statement.

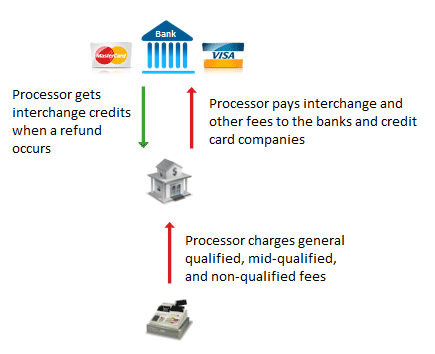

Bundled Pricing Allows Processors to Easily Intercept Refunds

If you’re not receiving credits, your processor may be using a bundled pricing scheme. If so, your statement probably looks something like the one below.

This is a sample statement from another business that we helped. Before finding CardFellow, this business’s processor was using bundled pricing, and as you can see, there’s very little detail on the statement.

On a bundled pricing model the processor essentially pays interchange fees on behalf of the business. However, they then charge the ambiguous qualified, mid-qualified, and non-qualified rates. In effect, bundled pricing positions the processor between interchange and the businesses they serve, giving them power over your money.

Interestingly, this position also makes it possible for a processor to intercept interchange credits rather than passing them along to you. The illustration below shows you the flow of interchange charges and credits.

In this illustration, we see that the processor (in the middle) pays interchange to the banks/card brands on behalf of the business, and charges the business arbitrary rates and fees. (The red lines.) When a refund occurs, the processor receives interchange credits. However, the processor isn’t obligated to pass those credits to the business, and pockets your money.

Related Article: Top 3 Hidden Fees of Credit Card Processing.

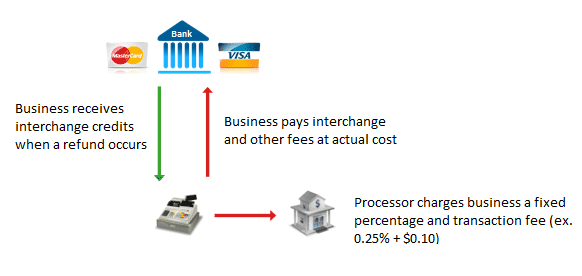

Pass Through Pricing: Patching the Refund Leak

It’s much easier to see if you’re receiving interchange credits on refunds if you work with a processor that offers interchange pass through pricing. Unlike bundled pricing, pass-through pricing allows interchange charges and refunds to flow directly to your business.

The processor sits on the sidelines and makes money by charging a low, fixed percentage and transaction fee instead of general qualified, mid-qualified and non-qualified rates which bundle everything together.

The following illustration shows you how interchange pass-through functions. As you can see, the processor isn’t sitting in the middle of everything manipulating fees and intercepting credits.

In this example, the interchange credits can return to the business when processing refunds. If you process a lot of returns at your store, recouping the costs you paid on the transaction is crucial for your bottom line.

But Interchange Plus Alone Won’t Fix the Problem

However, and this is important, interchange plus by itself doesn’t guarantee processors will return fees. Your processor can still elect not to pass the credit to you. In fact, it’s fairly common for a processor to pocket the fees. You’ll need a processor to commit to true pass-through pricing, including interchange credits on refunds.

CardFellow members can rest easy. We require processors to pass interchange credits to you when you refund a transaction.

Checking for Refunded Fees

Take a close look at your processing statement. Are you receiving the interchange credits you’re owed? If you’re not, consider switching processors to one that will pass along your rightful refund money.

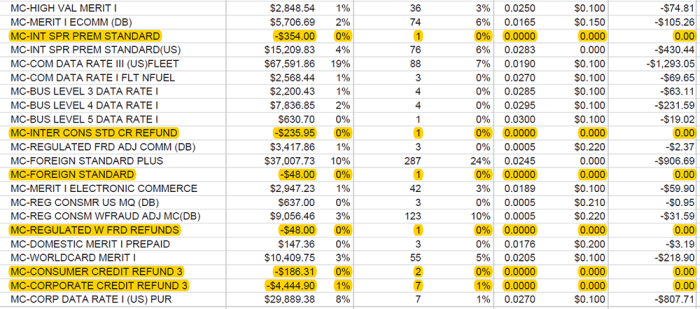

Keep in mind that even if you see refunds listed on your monthly processing statement, the processor may not be returning your fees from those refunds. For example, in the statement below, the processor listed all the times that transactions were refunded (highlighted in yellow) but did not actually return the fees paid to the business.

In the second column, the minus sign indicates a refund rather than a charge. In the final column, the 0.00 indicates that no money was returned to the business.

If you’re in the market for a new credit card processor, sign up for free here at CardFellow and receive multiple interchange pass through quotes instantly. We’ll also help you choose the best processor from the offers that you receive. Best of all, we require (through a legal agreement) that processors in our marketplace pass along your interchange credits. We even monitor your statements to make sure they do. You’ll never have to worry that your processor is pocketing money that rightfully belongs to you.