Based on the countless Intuit merchant account statement analyses we have done here at CardFellow, we have found Intuit’s credit card processing charges to be 40% – 50% greater than the rates businesses receive in our free marketplace.

Intuit is best known as the maker of the popular QuickBooks accounting software, and as the provider of the GoPayment mobile processing application. If the company’s credit card processing keeps going as it is, Intuit will also become known for exorbitant credit card processing charges and excessive downgrades.

In this article, we’ll briefly review what you get with Intuit credit card processing, the costs, and alternatives if you want to use QuickBooks but don’t want to pay the high processing fees associated.

Intuit Credit Card Processing

Most people know Intuit as the makers of QuickBooks, but the company has a merchant services division so that you can sign up for credit card processing as well. You may see references to “QuickBooks Payments” or “Intuit Payments,” both of which refer to accepting cards with Intuit.

You can use Intuit payments for accepting all major credit and debit cards. The company offers options for brick-and-mortar in-person payments, mobile in-person payments, online transactions through compatible web stores, and phone payments. Depending on your needs, you can also purchase equipment through Intuit. The company offers GoPayment readers for mobile solutions and partners with companies like Revel for POS systems.

QuickBooks and Credit Card Integration

Intuit’s popular QuickBooks accounting software makes it possible for users to process and record a credit card transaction in one easy step. But this convenience comes with a hefty price tag.

Intuit knows that competition from other credit card processors will drive processing costs down, so the company designs QuickBooks so it will only work natively with Intuit’s own credit card processing service. By reducing competition Intuit is able to charge excessive fees.

However, just because direct integration with QuickBooks requires an Intuit merchant account doesn’t mean you can’t get your data into QuickBooks in other ways. In fact, many popular plugins are seamless, allowing an easy integration that functions virtually the same as the direct Intuit integration.

If you’re not a fan of plugins, you can instead use an export/import function to send your transaction details from your processor to your QuickBooks account. There are multiple options for integrating credit card processing with QuickBooks that don’t require you to fork over extra money to Intuit.

If I use QuickBooks, do I have to use Intuit credit card processing?

No. Using QuickBooks does not lock you into credit card processing with Intuit. You can choose another credit card processor and still utilize QuickBooks for accounting. Additionally, many processors offer plugins that allow you to sync your transaction data with QuickBooks. Some plugins even allow you to initiate transactions within QuickBooks for processing with your merchant service provide of choice.

There’s a lot to consider when choosing a processing solution, and having QuickBooks adds another variable to consider. Fortunately, we’ve done a lot of the work for you. Our thorough guide to processing with QuickBooks covers everything from options for syncing data to choosing a plugin. Read more about QuickBooks credit card processing.

If I don’t use QuickBooks, can I still use Intuit credit card processing?

You can, but there wouldn’t be much reason to do so. The primary benefit of using Intuit for credit card processing is the automatic integration between QuickBooks and the payment processing. Without QuickBooks, you’re simply signing up for credit card processing, and Intuit’s options are pricey.

While Intuit now offers flat rate pricing that can be a savings over its tiered options, it’s still more expensive than other processing solutions available to both small and large businesses. If you don’t use QuickBooks, there’s no real reason to consider Intuit for credit card processing. Other solutions will be lower cost and may also provide more choices in terms of equipment and features.

Intuit Credit Card Processing Costs

It can be a little difficult to get accurate numbers for the costs to use Intuit for processing. In the past, the company heavily favored tiered pricing, though it has since begun including other pricing models. In fact, Intuit’s website prominently publishes flat rate pricing.

However, in CardFellow’s discussions with Intuit, we’ve found some inconsistencies between published pricing and what businesses have actually paid. If you plan to use Intuit, be sure to keep an eye on your statements and ask questions about anything that doesn’t line up.

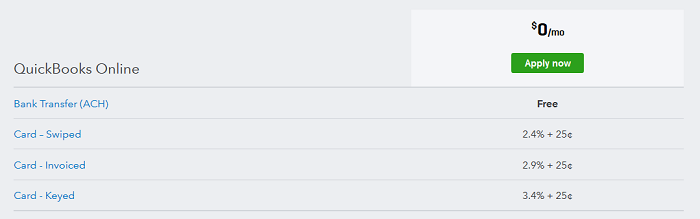

Intuit publishes different pricing for QuickBooks Online users and QuickBooks desktop users, as follows:

QuickBooks Online

Users signing up for processing with QuickBooks online only have the option of a “pay-as-you-go” style plan with no monthly fee.

Pricing subject to change.

As you can see from the screenshot above, the flat rates vary depending on how you take the card. A swiped card will cost you 2.4% + 25 cents per transaction while an invoice payment will cost 2.9% + 25 cents per transaction. Keyed cards come in the highest at 3.4% + 25 cents per transaction.

Some businesses prefer this type of flat rate pricing due to its apparent simplicity, but keep in mind that simple is not the same as low cost. For most businesses, this pricing is on the high side.

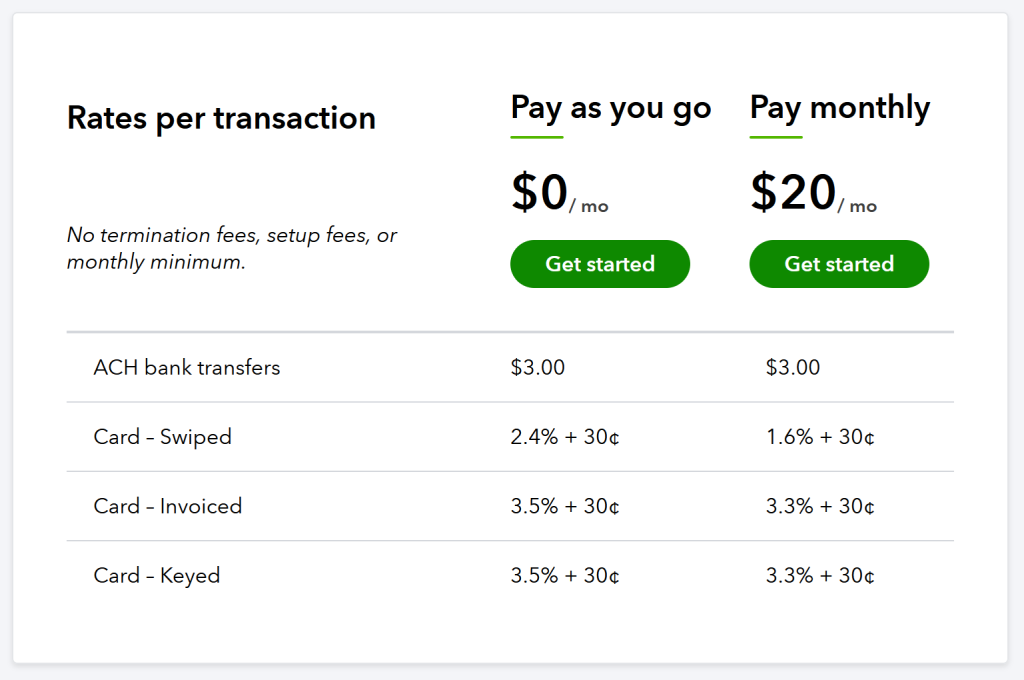

QuickBooks Desktop

You have two options when it comes to card acceptance with the various QuickBooks Desktop software: pay-as-you-go or monthly. The pay-as-you-go option has no monthly fee, while the monthly option will cost you $20/month in addition to the per-transaction costs. With that plan, you pay monthly in order to receive lower per-transaction costs. However, the ‘savings’ aren’t very significant for invoice payments or keyed cards, so if that’s your primary acceptance method, it may not make sense to take on a monthly fee.

Pricing subject to change.

In the screenshot above, Intuit lists pay-as-you-go rates starting at 2.4% + 30 cents per transaction for swiped cards, 3.5% + 30 cents for invoice payments, and 3.5% + 30 cents for keyed cards.

For monthly plans, Intuit publishes rates of 1.6% + 30 cents per transaction for swiped cards and 3.3% + 30 cents per transaction for both invoice payments and keyed cards.

While the percentage is already a bit high, the cents portion of the fee in particular is quite high. If you have a lot of transactions, this fee will add up quickly and bite into your bottom line.

While flat rate pricing is often lower cost than tiered pricing, it’s still not as low as competitive interchange plus. Unless your business only processes a few thousand/month in credit cards or has small average transactions (under $10), flat rate like the Intuit fees listed above will not be the lowest cost option.

In some cases, businesses may be on tiered pricing with Intuit, which is an even more expensive.

Other Pricing

Historically, Intuit has used tiered pricing and some businesses are on that model today. To understand how Intuit uses tiered pricing to conceal high rates we first need to look at the wholesale cost of credit card processing.

The banks that issue credit cards charge interchange. Interchange fees are the same for all businesses and processors. They represent the lowest possible rate for a given transaction.

If you’ve strolled through the blog here at CardFellow, or better yet, used our service to compare credit card processors in minutes, you know there are two basic forms of credit card processing pricing called interchange plus and tiered.

Interchange plus eliminates hidden credit card processing fees and is relatively inexpensive because it separates a processor’s markup from the interchange fees charged by banks. Intuit only offers interchange plus pricing to large businesses with substantial processing volume.

Instead, Intuit uses opaque and expensive tiered pricing.

Tiered Pricing

Tiered pricing allows Intuit to charge its customers based on its own rates called QUAL, MQUAL and NQUAL while paying interchange fees to banks behind the scenes. Intuit will decide which of your transactions it considers “qualified, “mid-qualified,” and “non-qualified.”

Each one of Intuit’s pricing tiers has a corresponding rate. For example, QUAL, MQUAL and NQUAL may carry rates of 1.60%, 2.60% and 3.60%, respectively.

With full control of rates, Intuit is able to dictate the pricing tier to which a business’s credit card transactions are routed. For example, Intuit may route a regular consumer credit card to the QUAL tier and a reward credit card to the NQUAL tier. You’d pay less to accept the consumer card than the reward card.

When Intuit processes a transaction at the higher MQUAL or NQUAL pricing tier the transaction is said to have downgraded. While it’s true that downgrades happen at interchange (how Visa and MasterCard classify a transaction), in the case of tiered pricing, many downgrades also occur at the processor level (Intuit gets to downgrade any transaction it wants).

Unfortunately, Intuit doesn’t disclose its ability to influence downgrades on the company’s website.

Note: In recent years, Visa has begun using “non-qualified” for some of its downgrade transactions, making it more difficult to identify tiered pricing just based on that. However, “non-qualified” is still a red flag that you’re overpaying – it’s just a matter of whether you’re overpaying due to interchange issues or due to your processor. It’s worth investigating if you see a lot of “non-qualified” transactions on your processing statement.

Intuit & Excessive Downgrades

Intuit makes more money when it routes a transaction to MQUAL or NQUAL because these tiers have higher rates than the lowest QUAL tier.

When talking with a prospective customer it’s not uncommon for a salesperson to claim that the QUAL rate will apply to most transactions, and only a small number of transactions will downgrade to the higher MQUAL and NQUAL rates.

The countless analyses of Intuit merchant accounts statements that we have done here at CardFellow prove the exact opposite is true. In most cases, Intuit downgrades an excessive number of transactions to the higher MQUAL and NQUAL rate tiers.

In the following examples we will look at actual Intuit processing statements sent to CardFellow by companies that used our free marketplace to get instant credit card processing quotes. Each company reduced credit card processing fees more than 50% by leaving Intuit.

Intuit Excessive Downgrades: Example #1

This snippet shows an Intuit merchant account statement for a medical office. Before switching from Intuit and lowering its fees by more than 50%, this business was using Quickbooks to swipe virtually all credit and debit card transactions.

Intuit priced this business with rates of 1.60% QUAL, 2.60% MQUAL and 3.60% NQUAL. Total Visa processing volume for this month was $31,550.03, but Intuit only considered $2,735.02 as QUAL. Intuit downgraded a whopping 90% of gross Visa sales volume to the NQUAL pricing tier!

We checked every conceivable reason for such excessive downgrades such as card type, software issues, delayed batching and more. We later found that Intuit was simply downgrading virtually every type of transaction except those involving a swiped debit or core (non-reward) consumer card. Effectively, Intuit overcharged this business on a full 90% of its Visa card transactions.

Intuit Excessive Downgrades: Example #2

This next example of excessive Inuit downgrading is taken from the statement of an online business that also used CardFellow’s free service to lower fees by over 50%. Like the business from example #1, this company was processing transactions correctly and should not have experienced this many downgrades as a result of interchange qualification. The excessive downgrades were caused by Inuit routing the vast majority of transactions to the NQUAL pricing tier.

As you can see, Intuit downgraded a staggering $62,460.29 to the NQUAL rate. That’s 69% of gross sales volume!

Save Money by Switching from Intuit

Despite Intuit’s best efforts, other processors are able to offer credit card processing for Quickbooks through software add-ons called plugins. Some plugins are proprietary and only work with one processor while others are universal and can work with multiple processors. However, each plugin functions a little differently. Some may require double-entry, while others boast functionality that is virtually identical to the native QuickBooks processes. If you prefer to initiate transactions directly in QuickBooks, there are plugins that allow for that as well.

It may take a little extra homework on your part to weigh the QuickBook plug-in options available, but we’ve made it much easier by covering important features and costs of several popular plugins.

Check our our overview of QuickBooks plugins.