Credit card processing fees seem complicated. But take away the sales jargon and it makes more sense.

First of all, what does “credit card processing fees” actually mean? There are several different rates and fees that make up your total processing cost. In this article I’ll explain the different aspects that contribute to the fees to give you a solid understanding of who’s charging what and which areas of cost you can control.

Not looking for explanations and just curious about the rates and fees for your business? Become a CardFellow member to receive competitive quotes instantly from leading processors. Our service is completely free and 100% private.

Each quote that you receive here at CardFellow comes complete with a credit card processing cost analysis that gives a comprehensive breakdown of fees and costs. It’s important to understand what each fee is and where it comes from, but the work of calculating costs for your business will be done by our software. Sign up now!

Components of Cost

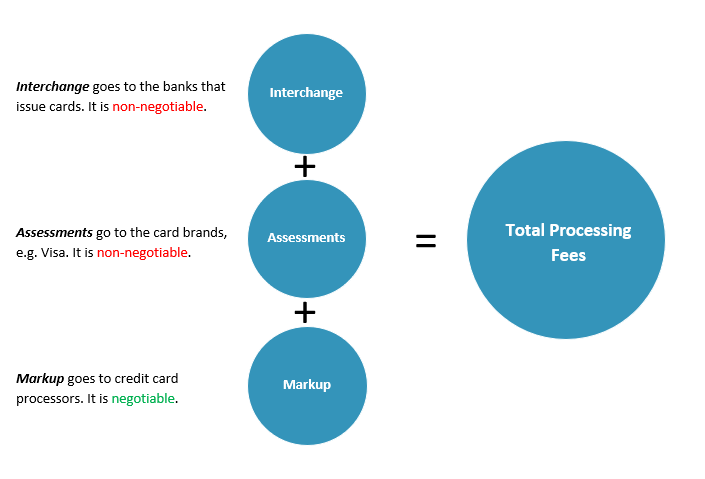

There are three parts to the total credit card processing fee you pay: interchange fees, assessment fees, and processor markup fees.

Even if you use CardFellow’s free service to find the best processor for your business, you should still understand one very important point, which is:

Specifically, interchange fees and assessment fees are non-negotiable. Those fees are set by the banks and card brands, and they’re the same for every processor. Together, interchange and assessments make up “wholesale” or “base cost.”

The rate that you pay to process a credit card transaction is a combination of base costs and markups. It’s technically called merchant discount. Think of merchant discount as the retail price of credit card processing, base costs as raw material expenses, and the markup as production costs. Thus, the merchant discount refers to your total credit card processing cost.

Base costs should account for the largest portion of expense (about 75% – 80%) followed by the markup (about 20% – 25%). With that said, we help a lot of businesses here at CardFellow that are getting hosed by their current processor, and their base costs are about equal to the markup they’re paying. In cases like this, there’s a lot of room for savings.

Jump down to the Cost Distribution section below to learn more about where your money goes.

Base Credit Card Processing Fees

Base credit card processing fees are made up of interchange and assessments, and they’re the same for all processors. No processor can give you a lower rate or a better deal on base costs. For example, First Data (the largest credit card processor) pays the same interchange fees and assessments as a small local bank.

It’s important to note that even though interchange rates don’t vary among processors, it is possible to optimize interchange charges to achieve lower costs. Check out our information on interchange fees for more details on interchange optimization.

Interchange

Interchange accounts for the largest portion of credit card processing expense and it’s paid to card-issuing banks. Believe it or not, your processor and the card brands (Visa, MasterCard, and Discover) don’t see any revenue from interchange.

The stakeholders of Visa, MasterCard and Discover (the banks) get together and decide how much they want to charge when you accept their credit cards.

The banks consider things like processing method (swiped, keyed, e-commerce), card type (rewards, business, consumer), your business type (merchant category code), and a host of other variables to create a long, exhausting list of interchange fees.

Visa and Mastercard both publish their interchange tables, while Discover does not. American Express doesn’t refer to their fees as interchange, but it functions similarly. However, they don’t post their fees publicly, either.

Interchange fees are typically two parts, consisting of a percentage and a transaction fee. For example, 1.51% plus $0.10 is the current Visa interchange fee for a swiped consumer credit card.

You can view Visa’s interchange table here.

Mastercard’s is available here.

Assessments

Visa, Mastercard, and Discover make money by charging assessments on every transaction involving one of their credit cards. Like interchange, assessments are exactly the same for all credit card processors and no processor can give you a lower rate or a better deal on assessments.

However, assessments may be charged differently if you’re on a bundled pricing model. Reason being is that your processor has more control to manipulate pricing on a bundled pricing system.

The assessments for each card brand are listed below along with the details about when they apply. Assessments are changed periodically by the card brands, and this list is updated as changes are announced.

Clarification of Terms: The only true assessment fee from each card brand is the percentage charge applied to volume. The various other fees such as network access, foreign handling, and so forth are charges incurred through processing behavior at the individual transaction level. I refer to card brand charges collectively as assessments because these charges are consistent for all businesses.

This list of fees is regularly updated to reflect changes and increases. Click the title to go to an article about that specific assessment fee and when it applies.

|

Visa

|

||

| Debit Assessment Also called Visa US Acquirer Service Fee – Debit – This assessment applies to all Visa debit transactions. |

0.13% | |

| Credit Assessment Also called Visa US Acquirer Service Fee – Credit This assessment applies to all Visa credit transactions. This assessment increased from 0.13% to 0.14% on January 1, 2019. |

0.14% | |

| Acquirer Processing Fee (APF) – Credit Also called Visa Authorization Processing Fee – Variable Credit The Acquirer Processing Fee applies to all U.S.-based credit card authorizations acquired in the U.S. regardless of where the issuer/cardholder is located. If your business is based in the U.S., the acquirer processing fee will apply to all Visa credit card authorizations. |

$0.0195 | |

| Acquirer Processing Fee (APF) – Debit Also called Visa Authorization Processing Fee – Variable Debit This fee applies to all Visa non-PIN debit authorizations acquired in the U.S. |

$0.0155 | |

| Credit Voucher Fee – Credit This fee applies to refund transactions involving a credit card. |

$0.0195 | |

| Credit Voucher Fee – Debit This fee applies to refund transactions involving a debit card. |

$0.0155 | |

| Base II Credit Voucher Fee (Credit) The Base II Credit Voucher Fee applies to all U.S.-based refund transactions involving a credit card. |

$0.0195 | |

| Base II Credit Voucher Fee (Debit) The Base II Credit Voucher Fee applies to all U.S.-based refund transactions involving a debit card. |

$0.0155 | |

| System File Transmission Fee Also called Visa Base II System File Transmission Fee System File Transmission Fee applies to all Visa transactions and is charged in addition to other transaction-based assessments, such as the Acquirer Processing Fee. |

$0.0018 | |

| Transaction Integrity Fee (TIF) Also called Visa Debit Integrity Fee This fee applies to transactions involving Visa non-PIN debit and prepaid cards that do not meet CPS requirements. |

$0.10 | |

| Fixed Acquirer Network Fee (FANF) FANF is a monthly fee that varies based on processing method, number of locations and volume. |

Varies | |

| Kilobyte (KB) Access Fee Visa’s kilobyte fee is charged on each authorization transaction submitted to Visa’s network for settlement. | $0.0047 | |

| Misuse of Authorization Fee The Misuse of Authorization Fee applies to Visa authorizations that are not followed by a matching clearing transaction (or in the case of a cancelled or timed out authorization, not properly reversed). |

$0.09 | |

| Zero Floor Limit Fee Visa’s Zero Floor Limit applies to cleared transactions that can’t be matched to a previously approved or partially-approved authorization. In short, it applies to settlement transactions submitted without a proper authorization. |

$0.20 | |

| Zero Dollar Verification Fee The Zero Dollar Verification fee applies to Zero Dollar Verification messages (approved and declined). Zero Dollar Verification messages include the verification of the card account number, address verification (through AVS), Card Verification Value 2 (CVV2) and Single Message System (SMS) acquired Account Verification authorizations. The Visa Misuse of Authorization Fee does not apply to these requests. The fee applies when you want to verify a cardholder’s information without actually authorizing an amount of their card. |

$0.025 | |

| International Service Assessment Fee (ISA) The International Service Assessment Fee applies to U.S. acquired transactions paid for with a card issued outside of the U.S. |

1.00% | |

| International Acquirer Fee The International Acquirer Fee applies under the same circumstances as the International Service Assessment Fee noted above.Note: The International Service Assessment Fee and International Acquirer Fee often both apply to the same transaction bringing the total charge to 0.85%. |

0.45% | |

|

Mastercard

|

||

| Acquirer Brand Volume This assessment applies to Mastercard transactions less than or equal to $1,000. | 0.13% | |

| Acquirer Brand Volume – Credit Transactions Greater than $1,000 This assessment applies to Mastercard credit sale transactions greater than $1,000. | 0.14% | |

| Acquirer Brand Volume – Debit Transactions Greater than $1,000 This assessment applies to Mastercard debit sale transactions greater than $1,000. | 0.13% | |

| Kilobyte Access Fee The kilobyte access fee is a data transmission charge assessed per byte of clearing and collection only data (where/if applicable). | $0.0035 | |

| Digital Enablement Fee This fee applies to all Mastercard card-not-present sale transactions. | 0.01% | |

| Cross Border Fee The fee applies to transactions where the merchant’s home country is different than the country where the card was used. This fee may be combined with the Global Acquirer Program Support Fee. | 0.60% | |

| Global Acquirer Program Support Fee This fee applies to transactions for U.S. merchants by cards issued outside the U.S. This fee may be combined with the Cross Border Fee. | 0.85% | |

| Network Access Brand Usage Fee (NABU) This fee is assessed on each authorization record for U.S. merchants for U.S. cardholders. | $0.0195 | |

| Acquirer License Fee This fee is assessed on a business’s gross MasterCard processing volume. This fee varies per acquirer based on MasterCard’s assessed charge as it’s distributed across the acquirer’s portfolio of merchants. Generally, the ALF fee is a fraction of a basis point. For example, 0.0045%, 0.0075%, etc. are examples of a likely ALF fee. This fee is also referred to by several processors as a License Volume Fee. | Varies | |

| Processing Integrity Fee: Card Present, Card-Not-Present, No Reversal The Processing Integrity Fee will apply in the following instances:

|

$0.055 | |

| Processing Integrity Fee: Pre-Authorization and Undefined Authorization MasterCard has updated its definition of an authorization from a single type to three separate types that are pre-auth, undefined-auth, and final auth. As of May 28, 2017, a pre-auth or undefined auth that is not properly cleared or reversed will incur a fee of $0.045.

A pre-authorization is an authorization that is not fully reversed or cleared within 30 calendar days of the authorization date. An undefined authorization is one that is not fully reversed or cleared within 7 calendar days of the authorization date. |

$0.045 | |

| Processing Integrity Fee: Final Authorization Transactions that do not meet final authorization standards will be assessed this penalty fee.

The final authorization integrity fee applies to authorizations that are not fully reversed or cleared within 7 calendar days of the authorization date, or to authorizations where the authorized amount does not equal the final clearing amount, or to authorizations where the authorized currency code does not match the clearing currency code. |

0.25%

Min. $0.04 |

|

| Address Verification Fee – Card-Not-Present MasterCard charges a fee each time a merchant access the address verification service when processing a transaction. MasterCard’s AVS fee is a little higher for card-not-present merchants than it is for card-present merchants. | $0.01 | |

| Address Verification Fee – Card-Present MasterCard charges a fee each time a merchant access the address verification service when processing a transaction. | $0.005 | |

| Account Status Inquiry Service Fee – Interregional The account status inquiry fee is charged for transactions where a merchant does actually authorize an amount on a cardholder’s account, but instead, validates aspects of her account. The interregional assessment is charged when the cardholder and merchant are not in the same region.

Account status inquiry transactions may include requests for address verification service (AVS), card validation code (CVC2), or both. MasterCard implemented the account status inquiry service on June, 14 2011 in place of support for AVS-only transactions. |

$0.03 | |

| Account Status Inquiry Service Fee – Intraregional The account status inquiry fee is charged for transactions where a merchant does actually authorize an amount on a cardholder’s account, but instead, validates aspects of her account. The intraregional assessment is charged when the cardholder and merchant are in the same region.

Account status inquiry transactions may include requests for address verification service (AVS), card validation code (CVC2), or both. MasterCard implemented the account status inquiry service on June, 14 2011 in place of support for AVS-only transactions. |

$0.025 | |

| Merchant Location Fee The Merchant Location Fee is billed annually at a rate of $15 per location. Payment facilitators will incur a Merchant Location Fee of $3 per merchant location. | $15 / $3 | |

| Interchange Downgrade Fee – Added in 2019, the interchange downgrade fee applies to transactions that have been “reclassified” during interchange qualification. | $0.15 | |

| Transaction Processing Excellence Program Fee – Added in 2019, this fee applies to transactions after 10 declined attempts on the same account number in a 24-hour period. | $0.10 | |

|

Discover

|

||

| Assessment The assessment applies to gross Discover card transaction volume. Note: In April 2016, Discover’s assessment increased from 0.11% to 0.13%. Note: In April 2015, Discover’s assessment increased from 0.105% to 0.11%. |

0.13% | |

| Data Usage Fee The Data Usage Fee applies to all U.S.-based authorization transactions. | $0.0195 | |

| Network Authorization Fee This fee will applies to all Discover network authorizations and will replace the previously assessed Data Transmission Fee, which applied only to settled Discover transactions. The amount of the Network Authorization Fee and the Data Transmission Fee are the same, but the Network Authorization Fee will apply to a greater number of transactions. | $0.0025 | |

| International Processing Fee The International Service Fee applies to U.S. acquired transactions paid for with a card issued outside of the U.S. | .55% | |

| International Service Fee The International Service Fee applies under the same circumstances as the International Processing Fee noted above. Note: The International Processing Fee and the International Service Fee often both apply to the same transaction bringing the total charge to 0.95%. This total will be 1.35% on and after April 15, 2016. |

0.80% | |

|

American Express

|

||

|

The advent of American Express’s Amex OptBlue introduced in early 2015 allows us to start listing Amex pricing on this page, as well. Like card brand charges for Visa, MasterCard and Discover, the charges listed below are paid to American Express.

|

||

| Assessment / Sponsorship Fee The assessment applies to gross American Express card volume. |

0.15% | |

| Card-Not-Present (CNP) Surcharge The American Express card-not-present surcharge applies to gross card-not-present volume, such as keyed and e-commerce transactions. The CNP surcharge is charged in addition to to the sponsorship fee of 0.15%, making Amex’s total assessment on card-not-present volume 0.45%. |

0.30% | |

| International Assessment The American Express international assessment applies to gross sales volume involving a card issued outside of the United States. |

0.40% | |

Markups

The markup over interchange and assessments is the only area where you have the ability to negotiate credit card processing costs. Keep in mind that many factors contribute to the markup, so not everything will be negotiable, or it will only be negotiable to a point.

Furthermore, the markup isn’t all profit. It’s split among all of the organizations that facilitate the processing of your business’s transactions such as the acquiring bank, processor, ISO(s), gateway or software provider and others. The markup must cover cost as well as profit for all of these entities.

Markups differ significantly from one processor to the next. These inconsistencies are why it’s difficult to accurately compare credit card processing on the open market. Here at CardFellow, we dictate the pricing model that processors must use to ensure fair, competitive pricing that you can easily compare.

Pricing Model

As mentioned earlier, interchange and assessments are the same for all processors. The method the processor uses to pass these costs to you is what is important. The two most basic types of pricing are interchange plus and bundled. They’re also referred to as pass through and tiered, respectively. Each pricing model is outlined below, and we also have a detailed post comparing interchange plus vs. tiered pricing.

Interchange Plus or Pass Through

With interchange plus pricing the processor’s markup isn’t dependent on interchange qualification. This separation of costs keeps the processor’s markup the same regardless of the type of card you accept, or how your process it. There are no qualified or mid-qualified rates with interchange plus. Until recently, there was no such thing as a non-qualified rate in interchange plus, either. However, Visa began using the term “non-qualified” for one of its downgrade categories, so there now could legitimately be a non-qual charge on your statement.

The processor earns a fixed percentage regardless of the underlying interchange. For example, you may see an interchange plus quote of 0.25%. No fancy tiers, no qualification at the processor level — just one rate that gets added to actual cost (interchange + assessments).

Interchange plus allows for interchange credits on refunded transactions. For example, when you issue a customer a refund, you are supposed to receive a partial credit of the interchange fee paid on the original transaction. This refund credit is not issued on bundled pricing models, but processors are capable of issuing interchange refunds on interchange plus pricing. However, just because a processor is capable of issuing interchange credits doesn’t mean it will.

Another benefit to interchange plus is that it allows for businesses to reap the benefits of decreases in interchange fees. For example, businesses with interchange plus pricing can benefit from lower debit card charges from the Durbin Amendment as of October 1, 2011.

Interchange plus is the least expensive, most transparent form of credit card processing pricing. For these reasons, it’s the only form of pricing that processors are allowed to quote here at CardFellow.

IMPORTANT

Like with bundled pricing, processors are capable of manipulating costs under an interchange plus pricing model, too. For example, interchange plus pricing does not guarantee that a processor will pass assessments at true cost, issue interchange credits, or refrain from applying a discount to refund volume. This article goes into more detail about the dangers of becoming pricing model-complacent.

This is yet another reason why it’s important to have expert guidance to ensure you secure a truly competitive processing solution for your business.

Tiered or Bundled

Tiered pricing, also referred to as bundled or bucket pricing, is named for the way a processor categorizes interchange fees into pricing tiers called qualified, mid-qualified and non-qualified. Although three tiers are most common, this pricing model can have separate sets of tiers for various types of cards. For example, six-tier pricing (where credit and debit cards each have their own three tiers) is gaining in popularity.

On a bundled pricing model the processor uses something called an interchange qualification matrix to route interchange fees to the qualified, mid-qualified, or non-qualified tiers.

A big problem with tiered pricing is that interchange fees are often not disclosed on your merchant processing statement (although they sometimes are), and the processor doesn’t tell you into which tier individual interchange fees are being routed. This leaves you with no way to calculate exactly how much you’re paying above the actual processing costs of interchange and assessments.

Tiered pricing has played a big role in building the processing industry’s shady reputation.

Inconsistent Buckets

Inconsistent buckets is the processing industry’s term for, “there’s no way to compare credit card processing quotes that are based on tiered pricing.”

Tiered pricing allows a processor to manipulate charges behind the scenes. Essentially, they can raise your cost without having to raise your rates. They do this by routing more interchange fees to the mid and non-qualified pricing tiers. Since there’s no consistency regarding interchange qualification, it’s impossible to compare tiered pricing among different processors.

Let’s look at an example to illustrate inconsistent buckets. Let’s pretend that we have the following quotes from two different processors:

Processor A |

|

| Qualified Rate: | 1.49% |

| Mid-Qualified Rate | 2.59% |

| Non-Qualified Rate | 2.99% |

Processor B |

|

| Qualified Rate: | 1.69% |

| Mid-Qualified Rate | 2.25% |

| Non-Qualified Rate | 2.49% |

Look only at the qualified rate, Processor A is offering a much better deal. What you don’t know is how many interchange categories are being routed to the qualified tier. Processor A may be routing the majority of transactions to the mid and non-qualified tiers making Processor B the better option. Of course, there’s no way to tell just by looking at the numbers.

Types of Fees

Credit card processing fees are either flat fees, transaction fees, or based on volume. Assessments are listed above, and Visa and Mastercard publish their interchange fees. The only inconsistent portion of cost is the processor’s markup. Unfortunately, the scope of different fees and pricing models utilized in the marketplace makes accurately comparing markups a daunting task.

This is the reason why we dictate the pricing model and fees that processors are allowed to quote here at CardFellow. All quotes are based on interchange plus pricing so that our software can present you with an accurate comparison of costs.

Trying to list the various fees that individual credit card processors charge is like herding cats. When comparing processing quotes, it’s easier (and more useful) to break fees down into three general categories and then compare each offer based on the estimated effective rate.

Volume

With interchange plus pricing (the best kind) the volume fee will be a single number such as 0.25%. With tiered pricing the volume fees will be in the form of a qualified, mid-qualified and non-qualified rate, and there may be more than one set of tiers.

Volume-based fees are levied against your business’s sales volume. The competitiveness, consistency and transparency of the volume-based markup are dependent on the pricing model that your merchant account utilizes.

Transaction

Credit card transaction fees often contribute more to total cost than volume fees. So, don’t ignore transaction fees to focus just on the volume markup (processor’s rate over interchange).

Transaction fees are charged each time your machine or gateway contacts the processor to get or give information, and they are a pre-determined fixed dollar amount regardless of the type or size of the transaction.

Flat

Flat fees are consistent regardless of sales or transaction volume. Monthly and annual charges are examples of flat fees.

Cost Distribution

With competitive pricing the majority of credit card processing costs are paid to your customers’ issuing banks through interchange. The remaining costs are split among a varying number of players such as the acquiring bank, processor, ISO(s), and equipment or software provider. Exactly how many players there are depends on the provider and your business’s processing needs.

Here’s an example that illustrates how credit card processing costs are distributed. Let’s pretend that you’re processing a $50 transaction by swiping a customer’s (consumer, non-reward) Visa credit card through your credit card machine. For this example we’ll assume that you used CardFellow to obtain a competitive interchange plus merchant account with rates of 20 basis points and $0.10 per transaction.

1.54% plus $0.10 = $0.87 goes to the issuing bank

0.11% plus $0.0195 to Visa when the transaction is authorized and another $0.003 when it’s settled = $0.07 goes to Visa

.20% plus $0.10 to the processor = $0.20 goes to the processor

$50 – $0.87 – $0.07 – $0.20 = $48.86 (2.28% overall effective rate)

Getting the Lowest Rates

Now that you know where processing fees come from, you know that the best credit card processor is the one that offers you the lowest markup over interchange and assessments. As we outline in this article, you shouldn’t be shopping for the lowest rates. Instead, you should be shopping for the lowest overall markup over base cost. Furthermore, you want to look at the whole picture and consider the effective rate. Don’t just focus on the interchange markup or another single fee.

Separate Costs

Interchange and assessments account for the majority of processing expense, and they’re not negotiable. Separate costs into interchange, assessments and markups when shopping for a merchant account and focus solely on getting the lowest markup.

Of course, you can make your life easier by letting CardFellow do the shopping for you. Sign up for free here at CardFellow to get instant interchange plus quotes from multiple processors.

Simplicity is Expensive

Simplicity is expensive when it comes to credit card processing. Companies like Square and PayPal Here are making nice profits by offering flat rate pricing to businesses that don’t spend the time to learn how processing fees really work.

For most businesses, credit card processing fees are second only to rental and real estate expense. All business people and entrepreneurs are busy, but the time invested in learning about credit card processing fees will pay off in spades.

Simple and competitive are two very different things, and for most businesses, credit card processing fees are either one or the other.