Level III (or level 3) data refers to providing specific line item details at the time of a purchasing card or government card transaction beyond what is required for consumer card transactions.

Visa and Mastercard have separate interchange categories for level III transactions, so providing all of the required information can result in savings if your business accepts a lot of cards that are level III eligible. However, not all cards are level III eligible, and not all gateways are capable of passing level III data.

Let’s take a look at when you should seek out a level III solution, current options for level III-capable gateways, and how to ensure you’re keeping your processing fees as low as possible.

Note that Visa refers to “level III” or “level 3” while Mastercard uses the term, “data rate III” or “data rate 3.” For the purposes of this article, we’ll use “level III” but the information also pertains to “data rate III” unless otherwise specified.

This article specifically addresses level III credit card processing, including purchasing cards, business-to-government (B2G) transactions, and large tickets. If you’re new to enhanced data or looking for more general information on B2B transactions or level II data, check out our guide to B2B Transactions.

Level III Requirements

Three primary factors affect whether a transaction qualifies for level III interchange rates:

- Whether the card itself is eligible for level III

- Whether you’ve provided all the required data for level III

- Whether your gateway passed all the level III information you provided

Additional factors, such as batching within a specific timeframe, may also affect your final interchange qualification.

Cards Eligible for Level III

Many corporate and purchasing cards are level III eligible, but some business credit cards are not. Business cards differ from corporate cards in that the cardholder is usually liable for purchases rather than the company. It’s more common for small businesses to have business credit cards and larger companies to have corporate credit cards.

There’s no way to look at a card to determine if it’s eligible for level III data, but it’s essentially irrelevant, as you’re not able to refuse specific cards anyway.

If you take a lot of corporate or government cards, it’s best practice to submit all of the required data for level III transactions. If certain cards are only level II eligible, providing data from level III won’t negatively affect your costs. If the cards are eligible for level III, you’ll benefit from the lower costs by providing all data.

Level III Line Item Detail

Level III transactions require sending the most data at the time of the transaction. Including specific line item detail is the only way to “qualify” for level III transaction rates. Level III transactions must include all of the fields required for level I and level II, as well as additional details that only apply to level III.

Level I fields include merchant name, transaction amount, and the date. Level II adds requirements including merchant zip code and tax ID.

Level III required fields are subject to change. The following lists are provided as a reference only. Be sure to confirm with your processor that you’re set up to pass level III data correctly and review your statements to confirm correct qualification.

Visa Level III Requirements

| Discount Amount | Unit of Measure |

| Freight / Shipping Amount | Unit of Cost |

| Duty Amount | Discount Per Line Item and Line Item Total |

| Item Commodity Code | Ship-To Zip Code |

| Item Descriptor | Destination Country |

| Product Code | Ship-From Zip Code |

| Quantity | VAT information (tax amount, rate, invoice #) |

Mastercard Level III Requirements

| Tax Amount | Item Quantity |

| Tax Indicator | Description |

| Customer Code (for Purchasing Cards) | Unit of Measure |

| Tax ID | Extended Item Amount |

| Product Code | Debit or Credit Indicator |

American Express Level III Requirements

Note that American Express level III data is only supported for businesses based in the U.S. who are doing business in U.S. dollars and have a direct account with American Express. That means if your business is on OptBlue, you’re not eligible for level III data with American Express.

| Date | Item Description |

| Suppler Name / ID Number | Unit Price |

| Dollar Amount | Quantity |

| Address with Zip Code | Freight / Handling |

| Sales Tax | Asset Number |

| Client Defined Variable Data Field (“Cardmember Reference Field”) |

SKU |

| Order Number, Cost Center / Accounting Code – or – Employee Name – or – Sample Number | Split Shipments / Shipment #

|

| Tax ID (TIN) | Total Meter Count |

| Minority, Women-Owned, Small Business Status | Service Credits |

| Corporate (1099) Status | Tax Type Code |

| Ship-To Zip Code | Supplier Reference Code |

| Supplier Reference Number (Order or Invoice Number, used for reconciliation) |

Source: Amex corporate purchasing card program administrator’s guide, available after sign-in.

While this looks like a lot of required line items, the good news is that some solutions automate the process of sending level III data, meaning you won’t need to manually enter the details when you process a transaction.

Level III-Capable Gateways

Cards aren’t the only component when it comes to level III data. Gateways play a large role as well. If your gateway isn’t capable of passing level III data, it’s irrelevant whether you provide all of the required level III details – the transactions will still not qualify for level III because the data never “arrived” with the transaction.

If the purchasing cards you accept are only level II-eligible, gateway choice won’t matter as much. Almost all gateways are capable of passing level II data. However, since you can’t tell from looking at the card if it’s level II or level III-eligible, it’s a good idea to specifically seek out a level III-capable gateway if you take a lot of purchasing, corporate, or government cards.

Countertop credit card machines and common POS systems don’t support level III. If you swipe a commercial or government card, you’ll be charged commercial card-present interchange rates, which are not the lowest cost. For achieving level III, you’ll need a gateway and virtual terminal solution.

Note that proprietary gateways offered by companies like Stripe and PayPal do not support level II or level III. If you accept a lot of commercial or government cards, those will not be a good fit.

Lastly, even gateways that support level III may not pass level III data on all processor platforms. It’s important to confirm with your processor that you’ll be set up for correctly passing level III data, and then verify correct setup once you start processing.

So, which gateways support level III data? Let’s take a look at the best options.

Best Gateways for Level III Processing

The “best” gateway for level III processing will include options like auto-filling required fields for you. Auto-fill helps reduce human error and ensures that you’re actually providing the line item detail necessary to qualify for level III rates. Fortunately, there are several gateways that can auto-fill data for you.

However, that doesn’t mean a gateway without autofill is a bad choice. It just means you’ll need to be up to date on the required fields and parameters for providing enhanced data. Businesses that have multiple staff members entering payments should avoid gateways and virtual terminals without auto-fill. Gateways without autofill take additional training and open you up to more errors when multiple people are entering enhanced data manually.

It’s also worth noting that if you have a direct account with Amex and want to provide level II and level III data, you’ll have a limited choice of gateways that can provide that data to Amex. Your options are primarily limited to processors that can utilize the FD North platform or Chase Paymentech Salem. The list below refers to gateways that are suited to providing enhanced data to Visa and Mastercard.

CardPointe

Offered by CardConnect, the CardPointe virtual terminal solution automates enhanced data for you. CardPointe can be configured to auto-fill the required fields when you process the card, saving time and minimizing the risk of human error.

Note that some processors can offer CardPointe on the FD North platform, meaning you’d be able to provide level II and level III data to American Express.

Where to get it: Processing companies that have a relationship with CardConnect can support CardPointe for enhanced data. CardPointe is an option with some processors that place certified quotes in the CardFellow marketplace.

Read more about it in our article CardPointe by CardConnect.

MX Merchant

The MX Merchant B2B app works in conjunction with the MX Merchant virtual terminal, allowing you to streamline level II and level III data. Once you enable the app, it runs in the background to populate required fields. You simply enter a transaction as usual into your MX Merchant virtual terminal, and the app does the rest. There’s no additional input required, and no extra employee training.

Where to get it: MX Merchant was developed by Priority Payment Systems, but the company doesn’t require you to use Priority for processing. As a result, many different processors offer MX Merchant, including companies that place quotes through CardFellow.

NMI

Network Merchants, Inc. (NMI) doesn’t actually offer services directly to businesses. It provides gateway solutions for other payment processing companies. Some of them “white label” the NMI gateway, meaning they pay NMI to use the gateway but call it something else.

NMI’s website is not geared to consumer businesses, but to processing companies. So while NMI says it can handle level II and level III data, it doesn’t provide additional details. Level III compatibility using the NMI gateway partly depends on what platform your processor uses. We reached out to NMI to ask about platform compatibility, but the company declined to provide that information. If you plan to use NMI for level III, it’s important to confirm with your processor that they have platform compatibility for level III.

Where to get it: Because NMI offers white labeling, many processors support the NMI gateway without calling it that. However, others still refer to it as the NMI gateway. In either case, processors in the CardFellow marketplace can support NMI.

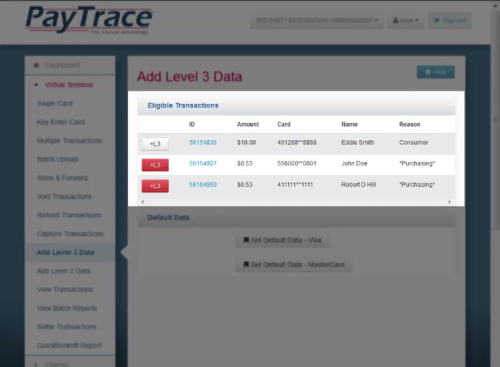

PayTrace

The PayTrace gateway notifies you in real time if a card you’re processing qualifies for level III data, giving you an opportunity to enter required details only for transactions that qualify. If you don’t include level III data at the time of the transaction, it will show up in your pre-settlement transaction report with a red button indicating it doesn’t have level III data attached. In the screenshot below, two transactions show an opportunity to qualify for level III, but haven’t had level III data added. They’re identifiable by the red “+L3” button and the “Reason” column listing “Purchasing.”

You’ll then have the opportunity to add level III data before settlement. Once added, the +L3 button will turn white instead of red.

You’ll also be able to create “templates” with default values filled in to speed up the process of providing level III line item detail. However, you can change the values for any individual transaction if necessary, or update the defaults in the template.

Where to get it: PayTrace is a universal gateway, meaning many processing companies support it, including those in the CardFellow marketplace. Get a quote for the PayTrace gateway.

Authorize.Net*

*Limited availability.

There’s an important caveat to including Authorize.Net in this list of best level III gateways – the company only recently began supporting Level III. As such, there is not much information available on how it works. We’re including it on this list because it’s one of the most popular and well-known gateways and the company intends to expand level III support.

In the spring of 2018, Authorize began seeking businesses for a pilot program testing level III transactions. At the time, level III was only available with Authorizet.Net for businesses using TSYS as their credit card processor.

As of 2023, there’s no new information about Level III support on Authorize.Net’s website. We’ve reached out to Authorize.Net to find out if level III is available with additional processors yet, and will update this section as more information becomes available.

Where to get it: Authorize.Net is a universal gateway, meaning almost any processor can support it, including those in the CardFellow marketplace.

While these aren’t the only options, they’re the best gateways for level III data in terms of ease of use and processor compatibility.

Ready to get started with a level III solution? Start here to get the most competitive pricing.

If you’re already accepting purchasing cards, you can check your gateway for compatibility.

Checking an Existing Gateway Account

Even if you think you’re passing level III data correctly, it doesn’t hurt to double check. Not qualifying for level III when possible means you’re needlessly leaving money on the table.

A quick way to check your qualifications is to look at your processing statement. Are you seeing a lot of “Standard” or “STD”? If so, your transactions are downgrading and it indicates a problem. However, in some cases you may be missing out on savings without an obvious listed downgrade. If you’re only receiving level II rates for transactions that are eligible for level III, you’re overpaying.

The best way to look for optimal B2B interchange qualification is to have a processing expert familiar with level II and level III review your statements. CardFellow offers a free independent analysis service to help you determine possible savings for your B2B or B2G transactions.

To get started, you’ll simply need to create a free business profile and upload recent statements.

Large Ticket Credit Card Processing

Many B2B and B2G transactions are large purchases. With large transactions, you’ll save more money with a lower percentage fee and a higher per-transaction fee because the per-transaction fee doesn’t change like a percentage does. Both Visa and Mastercard offer large ticket programs for high dollar value transactions.

Mastercard has multiple Commercial Large Ticket categories with dollar value thresholds:

- Commercial Large Ticket 1 applies to transactions from $10,000 – $25,000.

- Commercial Large Ticket 2 applies to transactions from $25,000.01 – $100,000.

- Commercial Large Ticket 3 applies to transactions from $100,000.01 – $500,000.

- Commercial Large Ticket 4 applies to transactions from $500,000.01 – $1,000,000.

- Commercial Large Ticket 5 applies to transactions greater than $1,000,000.

Visa has one “Commercial Product Large Ticket” category with a dollar value threshold:

- Commercial Product Large Ticket applies to transactions that are at least $5,000.

Visa also has a separate “Large Purchase Advantage Fee Program” with 5 categories with dollar value thresholds. However, those categories only apply to select Visa Purchasing cards. Other qualifying commercial cards for large purchases receive the Commercial Product Large Ticket rate.

The “Large Purchase Advantage Fee Program” thresholds are as follows:

- $10,000.01 – $25,000.

- $25,000.01 – $100,000.

- $100,000.01 – $500,000.

- $500,000+

In addition to the dollar-value thresholds, qualifying for large ticket rates requires correctly passing level III data. If you don’t provide level III data, you won’t qualify for large ticket interchange even if your transaction is above the dollar value thresholds noted above.

When to Choose a Level III Solution

The difference in amount of data required for level II vs. level III is not insignificant. Additionally, providing level III data requires a gateway that can explicitly handle level III. For these two reasons, it’s important to note that not all businesses need a level III solution.

If you accept a purchasing card occasionally but primarily take consumer cards, you don’t need to focus on level III data. For infrequent acceptance, it may not be worth your time or money to invest in a level III-capable solution.

However, if you accept a lot of purchasing or government cards or have frequent large ticket sales with purchasing cards, level III solutions may provide a measurable cost savings on your processing fees. The difference between level II and level III interchange rates can add up quickly, especially on larger transactions.

If you’re a government contractor, sell to wholesalers, or just generally have a lot of B2B transactions, you should set up level III credit card processing.

Level III Interchange Rates

As of 2023, Visa sets its level III rate for qualifying commercial cards at 1.90% + 10 cents per transaction. Mastercard splits data rate III-eligible cards into more categories than Visa. Data rate III cards range from 1.75% + 10 cents per transaction to 2.06% + 10 cents.

Rates subject to change.

Large Ticket Interchange Rates

Visa’s large ticket rate for commercial cards is 1.45% + $35.00 per transaction. A separate GSA large ticket rate applies to General Services Administration (GSA) government cards. That rate is 1.20% + $39.00 per transaction. For select purchasing cards, large ticket rates range from 0.40% + $58.50 to 0.70% + $49.50.

Mastercard has several categories for large ticket. Mastercard’s large ticket rates range from 1.20% + $40.00 to 1.51% + $40.00.

While the per-transaction component of the fee in large ticket rates seems high, remember that this rate only applies to higher value transactions. For large transactions, paying a lower percentage fee in exchange for a higher per-transaction fee results in lower overall costs.

Is Level III Really Worth It?

Yes. For businesses that accept a lot of purchasing or government cards, qualifying for level III rates can produce significant savings. This is especially true for businesses that have high average tickets.

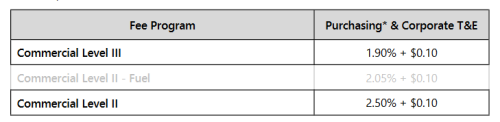

For example, in Visa’s interchange table, we see the rate for commercial level III is 1.90% + 10 cents. However, if you only provided enough data to qualify for level II on a card that is level III eligible, you would pay 2.5% + 10 cents: a 0.6% difference. On a $1,000 purchase, it’s only $6, but on a $10,000 purchase, it’s $60. Level III savings can add up quickly.

Not providing any enhanced data? You’ll pay 2.70% + 10 cents, leaving even more money on the table.

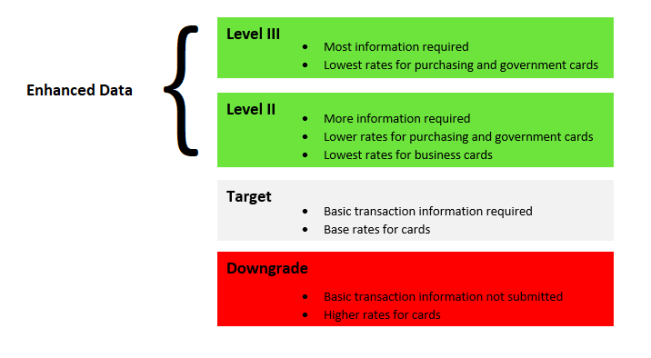

Target, Enhanced, Downgrades

Proving level III data is better than only providing level II, but providing level II is still better than not providing any enhanced data. If you don’t provide any enhanced data, you won’t qualify for the lower rates associated with that enhanced data, instead receiving the “base” rates.

Essentially, “target” interchange is what you can expect if you meet basic requirements but don’t go above and beyond. Going above and beyond by providing enhanced data allows you to secure more favorable rates.

However, if you fail to provide the required information for the target level, your rates will be higher. When this happens, your transactions “downgrade” to a below-target interchange category.

Downgrades for Purchasing Cards

If you accept a purchasing or government card and don’t provide any enhanced data, your transaction will typically qualify for “target” interchange. As noted above, target interchange is what you’ll qualify for when complying with minimum transaction requirements for a particular card. Target doesn’t get you the “perk” of lower enhanced data interchange rates nor the “punishment” of higher rates for failing to meet requirements.

However, if you don’t meet requirements for the “target” interchange category, your transaction will “downgrade” to a more expensive interchange category. For purchasing and corporate cards, that’s the category called “Standard” and it’ll cost you 2.95% + 10 cents before any processor fees are added. That’s a full 1.05% higher than level III purchasing card rates, which can add up quickly.

While it’s not possible to completely eliminate downgrades, if you see a lot of “standard” or abbreviations such as “STD” on your processing statements, you’re losing money to avoidable downgrades.

Still have questions? Sign up for a free CardFellow account to get quotes and give us a call to go through the numbers.