Digital Wallet Definition

For a quick reminder, a digital wallet refers to an electronic system that allows customers to pay for purchases without presenting a physical credit or debit card. Customers load their card details into the digital wallet app of their choice. They pay by tapping their smartphone or smart watch to a compatible terminal or by selecting their card from stored payment methods when making an online purchase. Apple Pay and PayPal are examples of digital wallets. For a more detailed explanation, check out the link below. See also: Introduction to Digital Wallets.

For a more detailed explanation, check out the link below. See also: Introduction to Digital Wallets.

Visa Staged Digital Wallet Fees

Given Visa’s past comments, it may not be a surprise that the company has chosen to update their fees. In 2013, when Mastercard announced its own staged wallet fee, Visa CEO Charlie Scharf stated that it would not be imposing the same fee at that time, but added that it would be, “Totally appropriate to do that.” Here is the text of the announcement Visa sent regarding staged digital wallet fees: Effective April 22, 2017, Visa will assess a transaction fee of $0.10 for staged digital wallet transactions. The fee will apply to purchase transactions and account funding transactions, identified by the “WT” Business Application Identifier (BAI). These transactions are subject to Standard interchange rates and are not eligible for Custom Payment Service (CPS) qualified rates. “Standard” interchange rates for Visa are typically 2.95% and 10 cents per transaction. From the wording of the announcement, an additional 10-cent fee will apply on top of the 10-cent portion of the standard interchange category.Mastercard Staged Digital Wallet Fees

Mastercard’s fee bears the mouthful name “Staged Digital-Wallet Operator Annual Network Access Fee.” Imposed in 2013, the Mastercard fee is tiered and calculated on the prior year’s transaction volume. Mastercard doesn’t provide any further details on the fee. Where the two fees differ is in who directly pays. Mastercard’s fee is aimed at the digital wallet operator (for example, PayPal itself) while Visa’s fee affects interchange, which businesses pay through their credit card processor. By charging the higher “standard” interchange rate for staged wallet transactions, Visa ultimately raises the base cost of processing those transactions, which will raise a business’ costs. That’s not to say Mastercard’s fee is necessarily cheaper since a digital wallet operator could simply choose to raise their pricing to cover the wallet fee, effectively passing it on to the business. Note: In 2016, Mastercard and PayPal reached an agreement that eliminated the Staged Digital-Wallet Operator Annual Network Access Fee for PayPal. It may still apply to other staged wallets.Staged vs. Pass Through Wallets

It’s important to note that the staged digital wallet fees only apply to "staged" digital wallets and not to “pass through” mobile wallets. A staged digital wallet is a wallet that uses multiple “stages” to complete the transaction- a “funding” stage and a “payment” stage - and doesn’t necessarily pass along card information to the card brand or issuer. With a staged digital wallet, the first “stage” is the funding stage, where the wallet acquires money from the purchaser. The second stage is the payment stage, where the wallet operator provides money to the business. The wallet essentially acts as a middleman. With a staged wallet, the card issuer or card network doesn't necessarily know what type of card was used or other useful information. PayPal, Google Wallet, and Square Cash are examples of staged wallets. A pass-through digital wallet is a wallet where card payment information is used directly in the transaction, and passed along to the issuer and card network. In many cases, a smartphone or other physical device may take the place of the physical debit or credit card, but the information from the card is still provided. For example, you may select a credit card in your Apple Pay menu and “tap” your phone to a compatible credit card machine to pay. Even though you didn’t swipe your credit card, your card details were used (by your smartphone and the machine) to make the purchase. Apple Pay, Android Pay, and Samsung Pay are examples of pass-through wallets.Costs for Digital Wallet Acceptance

Accepting pass-through digital wallets in your store will cost the same as if the purchase was made with a physical credit card. Whatever you pay for physical card transactions is what you’ll pay for digital wallet transactions with pass-through wallets like Apple Pay. Staged wallet transactions will now be more expensive if they’re a Visa transaction. (Non-PayPal Mastercard staged wallet transactions may also cost more, depending on how the wallet operator chooses to pass on Mastercard’s fee to your business.) Visa announced that, effective April 22, 2017, staged digital wallets will be incur a 10-cent fee per transaction and will be charged standard interchange rates. Staged digital wallet transactions are explicitly not eligible for Visa’s lower cost rates. Related Article: Qualifying for Visa CPS Rates.Why are staged wallet transactions more expensive?

The main reason seems to be to deter staged wallet transactions, which don’t pass along information to the card networks and issuers. If data about a transaction isn’t passed along to the card networks and issuers, it complicates things like consumer rewards and limits the card networks’ ability to follow trends in customer payment behavior. Additionally, the card networks feel that it allows some companies (like PayPal) to use their network in ways it didn’t intend or without paying their fair share. In 2013, Mastercard was not shy about explaining its rationale: “We view these new fees as an effective vehicle for diffusing much of the frustration that exists among incumbents who today view PayPal as a free rider. We would not be surprised to see other incumbent payment networks follow [our] lead.” Source: NFC World. In 2016, Mastercard CEO Ajay Banga reinforced the idea that Mastercard’s issue is with staged wallets due to lack of information: “If you do things that make it complicated for the ecosystem to work cleanly I’m not going to be supportive.[…] my view is the merchant must know which card was used to purchase the product. […]The data should flow cleanly back and forth. It enables the issuer, it enables the merchant, it enables the network to control fraud and do things with it. The moment you create a staged wallet, where you create a mix of different cards[…]I don’t particularly like it. You’re using my rails to play games with my client and me, that’s the problem.” Source: Diginomica. Essentially, the card networks want to discourage digital wallet companies from using their network without passing along information about the transaction.Does the staged wallet fee affect my business?

Maybe. The businesses that will be affected are those that accept digital wallet payments from staged wallets – PayPal, Square Cash, etc. – for Visa transactions. If that’s your business, you should expect to pay the higher “standard” interchange rate for those transactions. You will not be affected if you accept Apple Pay, Samsung Pay, Android Pay, or any other pass-through NFC wallet. In 2016, Mastercard and PayPal reached an agreement where PayPal will not pay a staged wallet fee for Mastercard transactions, so there’s no reason that a business should pay a higher fee for PayPal transactions that use a Mastercard. However, other staged wallet Mastercard transactions may still incur a fee for the digital wallet operator (such as Square Cash or Google Wallet) which may be passed to your business. Be sure to look at your statements or contact your processor if you have questions about your costs for specific digital wallet transactions.Spotting the Fee

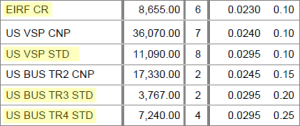

For Visa transactions, the staged digital wallet fee’s biggest impact is that it effectively “downgrades” some digital wallet transactions to more expensive “standard” interchange categories. Unfortunately, there are many things that can cause a transaction to downgrade, so the presence of a “standard” interchange category on your billing statement doesn’t necessarily reflect the staged wallet fee. However, it does provide an indication that you were charged more for that particular transaction than for other transactions. Look through your billing statement for the words “standard” or any variation, like STD or STND. That indicates the “standard” interchange category and is worth exploring further with your processor.

Lowering Your Processing Costs

If your processing costs are already too high and you’re looking to lower them, CardFellow can help. With a comparison shopping marketplace that offers quotes from leading processors and boasts no cancellation fees and statement auditing to ensure optimal interchange, you can quickly and easily find a solution with great pricing and great terms. Best of all, it’s free and there’s no obligation. Try it for yourself by filling out our short information form. (Don’t worry, we won’t share your contact info!)

Ben Dwyer began his career in the processing industry in 2003 on the sales floor for a Connecticut‐based processor. As he learned more about the inner‐workings of the industry, rampant unethical practices, and lack of assistance available to businesses, he cut ties with his employer and started a blog where he could post accurate information about credit card processing. As the blog gained in popularity, Ben began directly assisting merchants in their search for a processor. Ben believes in empowering businesses by providing access to fair, competitive pricing, accurate information, and continued support. His dedication to transparency and education has made CardFellow a staunch small business advocate in the credit card processing industry.