Processor Directory > Stripe

Stripe Review

Media attention itself doesn’t necessarily mean it’s right for you. Services, pricing, security, reviews, and customer service all play a role when finding your ideal processor. In this Stripe review, we’ll take a look at what it can do and what you need to know about processing with Stripe Payments.

- Stripe’s History

- News

- What can Stripe Payments do?

- Prohibited Businesses

- Stripe vs. Braintree: How are they different?

- Is it secure?

- Reporting

- Stripe Fees

- What else should I know?

- Customer Service

- Stripe Reviews from Customers

Stripe’s History

Stripe is a payment processing company founded in California in 2010. Officially, the company name is just Stripe but is sometimes referred to online as Stripe Payments or Stripe Credit Card Processing. Stripe is what’s called an aggregator, meaning it doesn’t provide individual merchant accounts to businesses, but rather aggregates them under one umbrella account.

The company has big name investors, such as PayPal co-founder and Tesla Motors founder Elon Musk, and big name clients such as Twitter, Kickstarter, Lyft, Reddit, and Salesforce. Stripe works with thousands of businesses and processes billions of dollars in payments each year. It’s also known as a "developer-friendly" platform due to its comprehensive documentation.

News

In January 2018, Stripe announced that it would be ending support for Bitcoin, citing decreased usage. The company has not ruled out the possibility of supporting cryptocurrencies in the future.

In March 2018, Stripe purchased POS company Index, indicating a move to accepting payments in-store in addition to the ecommerce options the company is known for.

What can Stripe Payments Do?

Stripe lets you take credit and debit cards through mobile apps or online stores. It’s primarily used by businesses that only take credit cards online, though in-person Stripe payments may be possible through integration with other systems like Shopify, Collect, and POS company Index, which Stripe acquired in spring 2018.

You can accept Visa, MasterCard, Discover, American Express, and JCB using Stripe. It also works with Apple Pay so you can keep your customers who use Apple products happy. Stripe supports other digital wallets (such as Google Pay) as well.

In early 2016, Stripe announced a new feature called Atlas, designed to help foreign entrepreneurs and small business owners get a bank account in the US and incorporate in Delaware in order to conduct business in America more easily. However, in this Stripe review, we’ll focus on services available for US-based companies. If you’d like more information on Atlas, visit Stripe’s website or check out this video from Stripe:

For US clients, you can use Stripe in the following ways:

Online Payments - Stripe Checkout

Stripe Checkout is a payment form that can be embedded within your existing website so your customers can pay instantly without being directed to another page. Checkout works with computers, tablets, and smartphones. With a mobile device, Checkout lets customers save their information and pay with a one-tap option to minimize frustration. Checkout uses JavaScript, and Stripe provides code for you. Checkout payment forms are customizable.

Stripe also offers Elements, a library of pre-built components that allow you to easily create your own checkout solution on mobile, desktop, or both.

Take Payments on the Road - Stripe Payments for Mobile

If you need to take payments on the go, Stripe offers seamless integration for mobile payments. Stripe’s mobile services are available for both Apple and Android systems. Mobile payments even lets you collect a card upfront and bill later.

In-App Payments – Stripe Relay

New to the Stripe offerings, Stripe Relay lets you create “buy” buttons that can be used directly within several different apps, increasing the sales from mobile devices. It’s a little different than a shopping cart system and is designed for quick purchases.

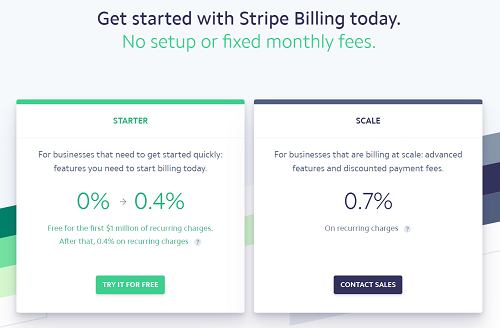

Stripe Billing for Recurring Payments

If you bill your clients on a recurring basis, such as for monthly subscriptions, Stripe has subscription options with no limit on the type of plans you can offer and charge. If a customer changes their subscription plan, Stripe will calculate the new payment for your customer automatically. Billing information is securely stored with Stripe, and changes in customer information can be made quickly and easily as needed. Stripe also works directly with the banks to make sure that credit card information is up to date so your automatic billing payments aren’t declined.

Recurring billing, called Stripe Billing, incurs separate fees.

As of 2018, the "starter" package costs 0.4% on top of the other charges for accepting payment. For example, if you accept a credit card, Stripe charges 2.9% + 30 cents. So if you accept a credit card through the recurring billing solution, your total fee will be 3.3% + 30 cents.

The "scale" package costs 0.7% on top of other payment charges, but Stripe states that you'll benefit from discounts on its usual pricing.

Note that Stripe currently runs a promotion to waive the 0.4% fee for your first $1 million in Stripe Billing transactions.

Take Payments In Person - Supported Services

While Stripe doesn’t offer in-person payments itself, it does explicitly endorse other services that do, such as Collect for Stripe. Collect allows you to take in-person payments on a smartphone or tablet with a compatible card reader or manually entering card details. Be aware that as a separate service, Collect charges an additional fee on top of Stripe’s fee, which may make it cost prohibitive. Get more details on Collect for Stripe.

Stripe also offers libraries for code in a number of programming languages, allowing access to developer solutions and platform building tools.

Stripe Capital

In September 2019, Stripe introduced a merchant cash advance program called Stripe Capital.

Like other merchant cash advances, Stripe Capital is not a typical loan. There are no interest rates. Instead, you repay the amount you borrow plus a fixed fee. However, you don't control the repayment - it's tied to your sales. In order to pay off the cash advance, you'll pay Stripe through a percentage of your daily sales, deducted from your credit card sales. The percentage remains the same, but means that you pay more toward the "loan" on days that you have higher sales, and less on days with lower sales. For example, the chart below, from Stripe's website, shows example daily payments for a business on a 12% repayment model. That means that they pay Stripe 12% of their card sales each day.

Some businesses prefer this type of arrangement, while others find it frustrating to not know when the loan will be paid off. However, you do have the option to pay off the advance in full with no early repayment penalty.

Stripe Capital eligibilty is based on your processing history with Stripe. You don't need minimum credit scores (Stripe doesn't even check your credit) or other requirements often found with traditional loan applications.

To check your eligibility, sign in to your Stripe dashboard.

Prohibited Businesses

Processing companies can choose to prohibit particular business types from using their services. In the case of Stripe, many industries that are considered "high risk" won’t be able to use Stripe. This includes businesses in firearm sales, adult entertainment, software as a service (SaaS) and more.

Some businesses in "high-risk" industries report that while they were initially able to sign up for Stripe, the company eventually determined that the business was not one that Stripe could support. In those cases, Stripe notified the business by email that the business would have 5 days to locate another processing company. Stripe also suggests to businesses that they consider high-risk specialty processor PaymentCloud.

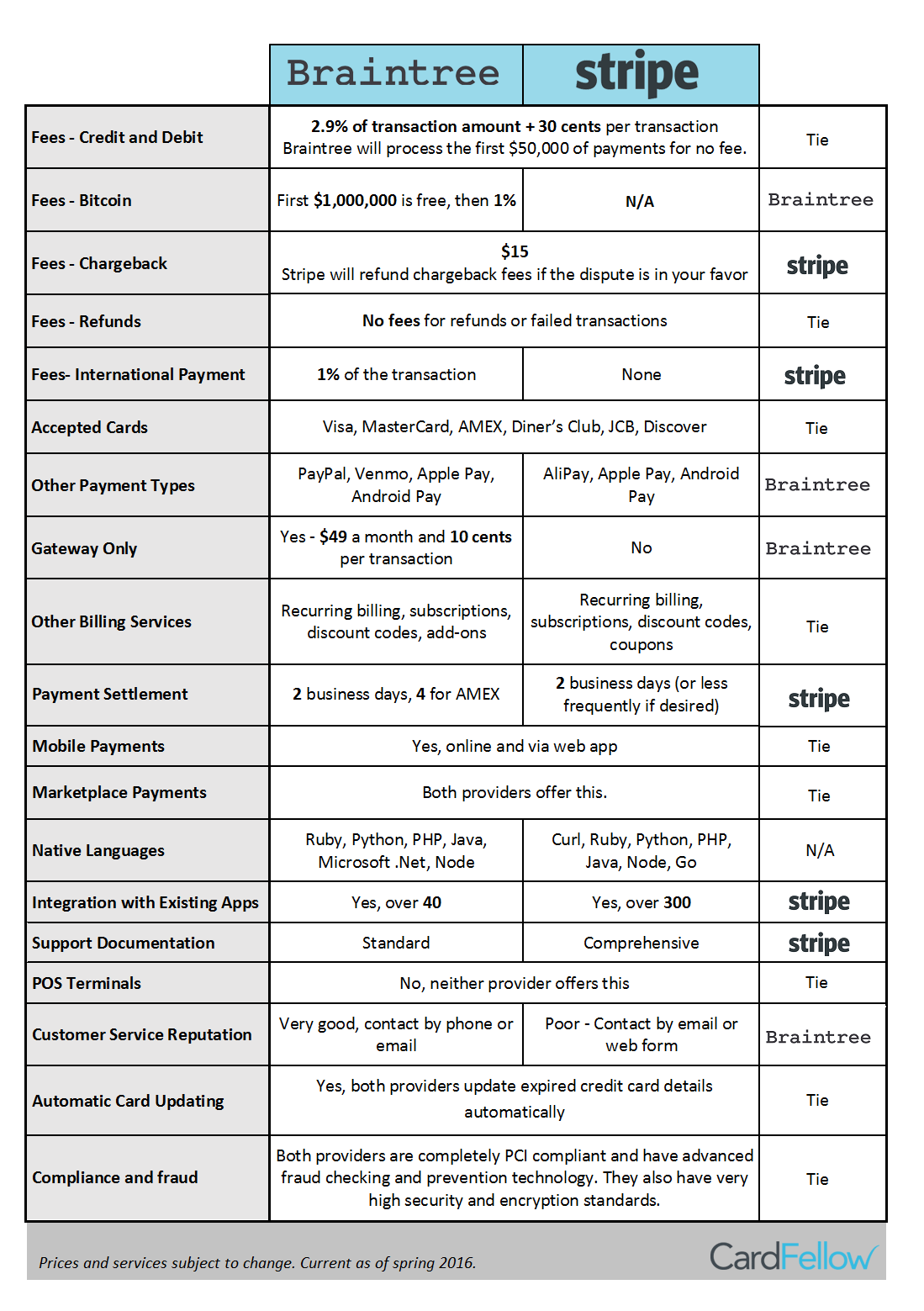

Stripe vs. Braintree: How are they different?

Stripe and Braintree both offer gateways for payment processing. They both allow you to accept multiple payment types. The biggest difference is that you can’t use the Stripe gateway separately from Stripe credit card processing. With Braintree, you have the option to use the gateway only, with a compatible credit card processor. The chart below gives a quick comparison for key areas of service, or this article on Braintree vs. Stripe provides greater detail.

Is it secure?

Stripe is a certified PCI level 1 provider.

Level 1 is the most stringent level of certification available. If you use Stripe’s existing code library you’ll be compliant with PCI requirements. Stripe keeps sensitive data safe, ensuring security for your business and your customers. Still not feeling secure enough? You can also enable two-factor authentication to add another layer of security to accounts. Stripe also continuously monitors charges for suspicious transactions to prevent fraud.

Stripe Radar

In autumn 2016, Stripe announced a new anti-fraud tool called Radar, a machine-learning system designed to "intelligently" fight fraud. Stripe talks broadly about algorithms and scanning transactions for "signals" that a transaction may be fraudulent, but doesn’t include information on what the signals are. The company states that you can review flagged transactions, set custom rules, and take advantage of existing anti-fraud technologies like Address Verification. The company offers an overview video of Stripe Radar:

As of December 2016, Radar does not cost extra and is automatically implemented in Stripe accounts. However, some customers find that Radar is too aggressive, resulting in declined transactions when legitimate customers attempt to make a purchase.

Related Article: How to Use Address Verification Systems.

Reporting

Stripe offers real-time reporting tools to make managing your business and expenses easier. A balance history function allows you to export activity, including payments, refunds, disputes, and more. Activity can be viewed for specific periods of time, or individual transactions can be reviewed. Reporting is available using Stripe’s online dashboard, or information and data can be imported into QuickBooks for easy reconciliation with your existing QuickBooks accounting software. For custom reports, the transaction data is also available through an API, allowing you to customize the information you need to see.

Stripe Fees

Stripe payments acceptance has no setup fee or monthly fee.

You’ll be charged a fee of 2.9% + $0.30 per transaction for each payment you accept online.

The per-transaction rate could be less depending on volume. If you process more than $80,000 month, Stripe suggests getting a personalized quote.

Additional charges may apply if you use optional services, such as Stripe Billing for recurring transactions. Recurring billing starts at 0.4% on top of the costs of card acceptance, but may be waived for the first $1 million of recurring transactions you process.

Stripe’s fees are competitive in certain situations, most notably for businesses with low monthly credit card volume (under a few thousand per month) or small average transactions. If that’s not you, it’s definitely worth comparing the costs of Stripe to other processors. You can request a quote from Stripe directly by signing up for a free CardFellow account to compare with any other processors you want.

Other Fees

In addition to the above costs, the may be other fees that Stripe will only charge you if a transaction triggers the fee. For example, Stripe has a chargeback fee of $15 per chargeback. However, Stripe will refund the chargeback fee if the dispute is found to be in your favor.

If you accept payment in international currencies, conversion fees of 2% on top of other costs may apply.

Getting Your Money

Stripe claims that funds will be transferred to your account on a 2-day rolling basis. The company also boasts no refund costs, but will not return the fees paid on the transaction. For businesses that accept a lot of refunds (such as clothing stores) this may not be an ideal situation. Some processors will return fees paid on a transaction when you refund the customer. In fact, we require that for processors placing certified quotes here at CardFellow.

Read more about fees on refund transactions.

Contract and Cancellation

Stripe has no early termination fee, effectively creating a month-to-month contract that can be cancelled with notice. Be sure to read all the details of your contract for specifics.

What else should I know?

Stripe supports payments in more than 100 currencies. If you have customers from around the world, offering the ability to pay in their own currency provides convenience and may help drive sales. Stripe can also be configured to offer your customers trial periods or provide coupons to goods and services.

Customer Service

Unfortunately, customer service is a common complaint in Stripe reviews. The company doesn’t prominently display phone numbers for customer service and prefers that clients use email or the support FAQ for customer assistance. The Stripe FAQ contains multiple questions under 8 headings: My Account, Subscriptions, Integrating Stripe, International, Transfers and Deposits, Pricing, Disputes and Fraud, and Accounting and Taxes. Know that it may take a little time and effort to get answers if you have a problem with your Stripe account. Some reviews have complained about frustration and wasted time attempting to contact Stripe to resolve problems.

In the summer of 2018, Stripe took measures to improve customer service by implementing 24-hour phone and chat support. You'll need to log in before you can access the support features.

Stripe Reviews from Customers

Now that it has been around for several years, there are more Stripe reviews available online. Unfortunately, many reviews express frustration at certain Stripe policies, including unreliable customer service, lack of contact information, and frozen or held funds. Tracking the response over the past few years has shown an increase in customer dissatisfaction, though there are still good reviews as well. Positive testimonials generally praise the company’s ease of use.

Stripe Payments Reviews with the Better Business Bureau

Stripe, Inc. has been accredited with the Better Business Bureau since 2013 but has had a profile with the BBB for longer than that. In 2016, the company bounced back up to an A+ rating after hovering around B+ during 2015. Confusingly, there has actually be an increase in complaints with the BBB despite the higher grade. The company is up to 350 complaints in the past 3 years, although only 139 are within the past year. The vast majority of complaints fall into the category “Problems with Product/Service.” The category “Billing/Collection Issues” accounts for the next most complaints, with “Delivery Issues” accounting for a handful, “Advertising/Sales Issues” accounting for a few and the remaining 1 complaint in the “Guarantee/Warranty Issues” category.

Complaints allege products purchased were never provided, companies weren’t contacted prior to Stripe refunding customer payments, long wait times for funds to be deposited, unexplained charges, and sudden account closures.

Only 78 complaints are listed as satisfactorily resolved. 1 complaint is listed as unresolved due to Stripe responding but not making a good faith effort to resolve the complaint according to the BBB. The remaining complaints are listed as “answered”, indicating that Stripe responded and attempted to resolve the issue, but that the BBB either didn’t hear back from the original business about the complaint, or the business was not satisfied with Stripe’s proposed resolution.

There are also 25 customer reviews for Stripe on the BBB website, up from 7 in 2015. All 25 reviews are categorized as negative and marked as ‘would not recommend’ the company to family or friends. Reviews complain that Stripe is difficult to get set up, that the company holds funds and accuses businesses of fraud, and that Stripe is difficult to reach. Some reviews go further, accusing Stripe of being a scam or ripoff.

What CardFellow Thinks

At CardFellow, we don’t “rate” processors or offer traditional reviews. We include factual information that we have verified firsthand, such as statement reviews we’ve conducted for current or past Stripe customers. Currently we don’t have additional firsthand information regarding Stripe’s services, pricing and rates, or contracts. As such, we’re not able to offer a Stripe review of our experience.

If you’re considering Stripe, we strongly encourage you to create a free CardFellow profile to request a quote from Stripe directly through your CardFellow account. Requesting a Stripe quote through CardFellow allows our software to show you how the pricing and terms compare to other processors, helping you make an apples to apples comparison so you don’t overpay for processing. You can review your Stripe quote and any other quotes privately without pressure from sales calls.

Are you a current or former Stripe customer? Tell us what you think. Leave a review!