Need help choosing the right credit card machine for your small business?

When you’re deciding how to take credit cards, the equipment you purchase is a big decision. In this article, we’ll tackle major brands, popular features, processor compatibility, and more.

Need specifics on particular machines? Be sure to check out our credit card machine directory. You can also request quotes for processing and for purchasing machines right through the directory.

The Best Credit Card Machine for Small Businesses

We say this a lot at CardFellow, but it’s true: the best option for you will depend on your needs and budget.

We often caution against choosing a credit card processor based on “top ten” lists or customer reviews, because there’s no way to know if you’re getting the same pricing and terms as the reviewer. However, that’s not as much of a concern with a credit card machine. Since you’ll get the same product, with the same built-in features, reading reviews of machines can give you a better idea of whether it will satisfy your needs.

That said, there are still some situations where one reviewer’s experience won’t be the same as yours. To help you determine the best fit, let’s go over some basics.

Features

Different models offer different features, but in general, credit card machines provide the limited functions of accepting cards. They do not offer non-payment features, like inventory management or restaurant table management. If you need options like that, you’ll want to consider a full POS system instead.

With a credit card machine, you’ll be able to take credit and debit. (Some models include built-in PIN pads for PIN debit transactions.) Some machines let you take magstripe, EMV chip, and NFC (contactless) payments while others only accept magstripe and EMV. These days, it’s harder to find a magstripe-only machine, and since the technology is outdated and less secure, you shouldn’t purchase a magstripe-only model anyway.

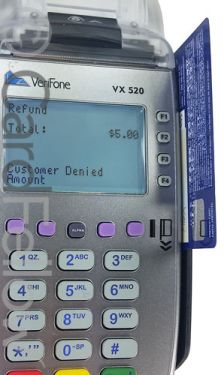

Pictured below is a popular Verifone Vx520 model, which boasts an EMV chip slot on the bottom and a magstripe reader on the side.

On most models, you’ll be able to view limited sales reports, showing transactions from specific periods. You can void transactions and process refunds or returns. Some models also offer an “offline” or “store and forward” mode where you can take cards even when your connection goes down. The machine will “store” them and forward them for processing when a connection is available. Many models have a built-in receipt printer so that you don’t need to connect another machine in order to provide receipts to customers.

Some models are Wifi or 3/4G capable while others connect via phone line. Display screens may be full color or monochrome, and can be touchscreen or traditional key entry.

Universal and Proprietary Terminals

When it comes to credit card machines, there are two “types”: universal and proprietary. Universal machines are what they sound like – they’re machines that the manufacturer doesn’t restrict to a particular processor. Proprietary machines work with one or a handful of processors, restricting your use of that machine to a few companies.

Most businesses wants to know what type of machine they’re buying for one reason: reprogramming capabilities. If you purchase a proprietary machine and want to switch credit card processors in the future, you will need to purchase a new machine. If you purchase a universal machine, you can (usually) sign up with a new processor that can reprogram your existing machine.

Read more: Credit Card Machine Companies

Determining Status

To determine if a machine is universal or proprietary, you can ask directly. (Or check our credit card machine directory, which lists the status of equipment.)

As a loose rule, if the equipment is made by a processing company, it’s likely restricted to that company. If it’s made by an equipment manufacturer, it will be open to multiple processors.

Processing companies like Square offer proprietary terminals – you can only use those machines with Square processing. Equipment manufacturers like Ingenico and Verifone offer universal terminals – you can use them with any processor that supports them.

Somewhere in the middle are machines offered by processors that allow them to be used with any processing company on their platform. For example, Fiserv (a processing company) offers the FD line of processing equipment. Any processing company that runs on Fiserv’s platform can sell you FD terminals and can reprogram them if you already own one. Technically, the terminals aren’t universal (as they can only be used with companies affiliated with Fiserv) but there are many companies that run on the platform and could reprogram FD terminals. That makes them less limited than true proprietary options.

A Note on Clover Systems

The popular Clover Station and smaller Clover machines are a bit of an odd case. They’re First Data (now Fiserv) terminals that any processing company on the platform can use, but they can’t be reprogrammed. Once you purchase a Clover from a processing company, it will only work with that company.

The Clover Flex credit card machine

In that sense, Clovers are much closer to proprietary than universal. Even though many companies can offer them and program them, no company can reprogram them once they’ve been set up.

If you plan to purchase a Clover, be sure you’re comfortable with the processor you purchase from and expect to stick with them for a while.

Popular Brands

There are several brands of machine manufacturers, but a few are more well known than others. Most commonly, you’ll see universal options from Verifone and Ingenico. You may less commonly see universal machines from Dejavoo or PAX. The Poynt smart terminal is also making a name for itself as a credit card machine.

For non-universal machines, the FD and Clover lines (both work with Fiserv processing services) are popular options.

For proprietary systems, you’ll regularly see Square and PayPal equipment.

Credit Card Machines vs. POS Systems

One thing to consider is whether you need a basic credit card machine or a full POS system. Credit card machines are smaller and offer fewer features. Many businesses don’t need or want a full POS system.

POS systems offer both card acceptance and non-payment functions, such as inventory management capabilities, detailed sales reporting, employee timeclocks, payroll, and other features. By contrast, countertop credit card machines are primarily designed for accepting credit and debit cards. They may offer limited reporting, but won’t provide other non-payment business functions. If you just need a machine to handle card payments, a traditional credit card machine will suit your needs.

You can choose to use a credit card machine, a POS system, or both. Some businesses find that using both best suits their needs. It’s common when using POS systems that don’t include integrated card readers or for situations where you want to take payments in multiple locations in a store or restaurant.

Credit Card Machines vs. Mobile Card Readers

In the last few years, mobile card readers have become more popular. The small readers connect to smartphones or tablets via headphone jack or Bluetooth, allowing you to take credit and debit cards without a special machine.

While most people are familiar with Square’s small white reader, these days almost every processor offers a reader. (Either their own or a universal model made by a machine company.)

Each reader works with a processor’s payment app, which you’ll need to download prior to using the reader. The app will enable payment acceptance, and in some cases provided limited functions like adding products to inventory for easier check out.

Credit card machines and mobile card readers offer similar functions, but mobile card readers are designed for use on the go. If you’re taking cards in a store or at a restaurant, you may find it inconvenient to use a smartphone for taking payments, as phones are easier to drop or misplace. Additionally, for brick-and-mortar stores / restaurants, accepting payments using a cell phone reader may have negative customer perception. Customers may (incorrectly) assume that the business is small time or that the transaction will not be secure.

Buy or Lease

Despite what a sales rep might tell you, there’s no good reason to lease a credit card machine. It will cost you significantly more in the long run, and these days, machines are not cost-prohibitive. A basic chip-capable credit card machine starts around $300.

Leases typically involved non-cancellable 3 or 4-year contracts that are separate from your merchant account contract. Even if you close your business, you will still have a contract for your machine. Additionally, some leasing companies aggressively pursue small businesses in court if those businesses attempt to get out of a lease contract.

Save yourself the headache and purchase outright.

Free Credit Card Machines

Some businesses are attracted to offers of free credit card machines. While everyone likes getting things for free, with credit card machines, it’s not truly free. Instead, the cost is built in somewhere else; most often in the form of higher processing fees.

Remember, the machine is a one-time cost. Your processing fees are ongoing. It doesn’t make sense to get a one-time lower fee (the machine) if it means you’ll be paying more for every credit card you accept indefinitely.

In general, if a processor offers competitive pricing, their margins won’t be large enough to provide you with a free machine.

Where to Buy

Once you’ve decided on the machine you’d like to use, the question is where to buy it? You have a few options:

From Your Processor

Purchasing from your processor is the easiest method. When you open a merchant account, the processor will discuss equipment options with you. Most processors have several choices, so you’ll be able to pick the machine that fits your needs.

Processors in CardFellow’s marketplace charge at or near cost for machines, so there won’t be a big markup. Outside of CardFellow, prices can vary greatly. However, be careful about assuming a low online price means that a processor is overcharging for a machine. In some cases, processors will quote low machine prices to entice you, but charge exorbitant processing rates or use hidden fees to make up for it.

Purchasing Online

These days, purchasing items online is popular for convenience and the ability to easily shop around for the best deal. That can apply to purchasing credit card machines online, but be aware of possible issues. While you may be able to get a good deal on a machine that will work with your processor, there are two important considerations:

- Processor compatibility with machines comes down to the serial number level. If you plan to purchase online, be sure to confirm with your processor before purchasing. The last thing you want is a machine that you can’t use with your processor.

- Some machines are listed at very low prices online. Hidden in the fine print is a requirement that you use the seller (a processing company) for processing in order to receive that price. In those cases, you wouldn’t be able to use a lower cost processing company. Even though the machine is less expensive, you’ll make up for it with higher processing fees, negating any savings and costing more in the long run.

If you want to avoid the potential pitfalls of buying online, you can go direct to your processor to purchase a machine. Processors that place quotes in CardFellow’s marketplace sell equipment at or near cost.

From a Friend or Other Business

Another possibility is purchasing a machine from a friend or from another business. As with purchasing online, it’s important to ensure that the machine is compatible with your processor and that it can be reprogrammed. Contact your processor with details about the machine to confirm compatibility before purchasing.

Remember, some machines, such as Clovers, can’t be reprogrammed to work with another processor.

Keep in mind that if you purchase a machine from a friend or from another business, you’ll need to ensure that your business has the merchant account connected to the machine.

Of course, the key to a great processing solution isn’t just the right machine. Be sure you’re getting the best credit card processor for small businesses by familiarizing yourself with rates and fees, terms, and more. Sign up at CardFellow for free assistance.