Daily and monthly discount refer to when a credit card processor deducts fees from your business checking account for processing your credit card transactions. There’s a big difference between the two, so give careful thought to which method is best for your business.

Some processors only offer daily discounting, while others offer a choice. If you open a merchant account that lets you choose, monthly discount is usually the better option. Let’s look at the differences between daily and monthly discount.

- Difference Between Daily and Monthly Discount

- Monthly Discount

- Daily Discount

- How to Tell Which Discount Method You Have

Difference Between Daily and Monthly Discount

The names give it away. With monthly discount, your processor deducts fees from your account in one lump sum once a month. With daily discount, your processor deducts fees daily throughout the month as well as at the end of the month.

Which discount method is best? Well, that’s for you to decide. However, we can tell you that most businesses prefer monthly discount because it’s easier to reconcile and it creates a more positive cash flow.

We allow processors to use either discount method here at CardFellow, but all processors offer monthly discount by default. Processors only switch their quote to daily discount if a business specifically requests that they do so.

It’s important to note that discount method is independent of pricing model. Any pricing model can utilize either monthly or daily discount.

Read more about credit card processing pricing models.

Monthly Discount

With monthly discount, a processor tallies all charges for a month and deducts fees in one lump sum at the beginning of the following month.

The processor pays interchange fees throughout the month on behalf of the business in what amounts to a micro loan of sorts. This is because a business’ processing bank (acquirer) pays interchange fees to a cardholder’s issuing bank when settling the transaction, so it happens more frequently than once per month.

By fronting the money to pay interchange fees, the processor makes it possible for your business to receive gross deposits from sales throughout the month.

Easier to Reconcile, Better Cash Flow

Monthly discount makes reconciling processing charges easier since the processor deducts all fees at once. It also creates a more positive cash flow by allowing for the receipt of gross deposits from sales. Many businesses prefer monthly discounting for those two reasons.

Daily Discount

With daily discount, a processor deducts the qualified rate or interchange plus markup throughout the month and then deducts all other fees at the end of the month.

Businesses billed via daily discount receive net deposits from sales because the processor deducts their fees from batch totals at settlement. The result is that the business receives deposits from sales less the processor’s rate.

For example, a business with a qualified rate of 1.69% that settles a batch for $100 will receive a deposit of $98.31 ($100 – $1.69).

The processor charges only the qualified rate or interchange markup prior to deposit. Any other fees such as mid-qualified rates, non-qualified rates, transaction fees, and monthly fees are deducted in one lump sum at the being of the following month.

Harder to Reconcile, Hurts Cash Flow

Processors deducting fees throughout the month and at the end of the month makes it more difficult for you to reconcile. Receiving deposits in net rather than gross hurts cash flow.

Disguises Total Cost of Processing

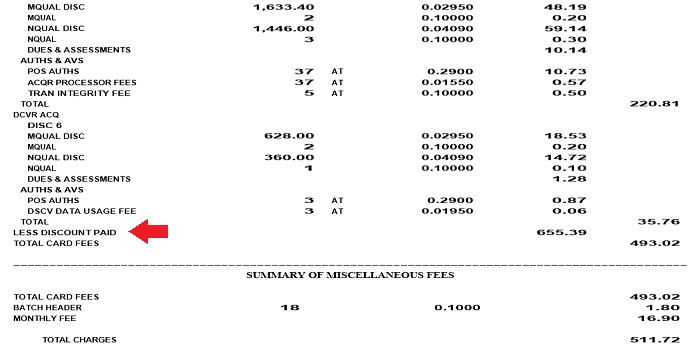

Daily discount also disguises the total cost of processing by breaking total charges into “discount paid” and “discount due” subtotals. In order to realize how much a business paid in credit card processing fees, charges assessed throughout the month must be added to charges assessed at the end of the month.

In the statement above, the line “less discount paid” next to the red arrow shows fees already paid; however, this amount is not included “total card fees” summary line or the “total charges” line, making it look like the business ultimately paid less in fees. In order to see the actual costs for processing, add the “total charges” amount and the “less discount paid” amount. The business didn’t only pay $511.72 in fees. It paid $1,167.11.

Statements often misleadingly make it appear that total charges are only those that the processor deducted at the end of the month. This can lead some businesses to think they’re paying less than they actually are.

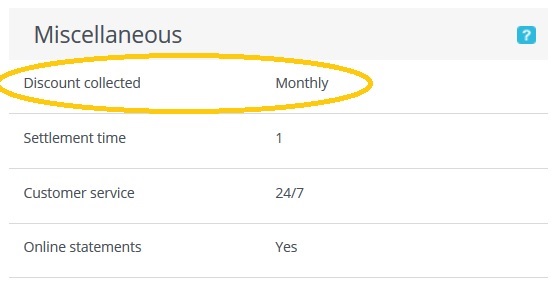

How to Tell Which Discount Method You Have

If you’re reviewing credit card processing quotes here at CardFellow, simply click the “view rates and fees” button in any quote. Scroll down to the “miscellaneous” section as shown.

We require processors to fully disclose all quotes, including the discount method.

If you’re already processing, it’s pretty easy to tell which discount method your current processor is utilizing. You will be receiving net deposits from sales or gross. From that, you can easily determine the discount method. You can also check your monthly processing statement.

If you see phrases on your statement such as “Less Discount Paid” or “Discount Paid” you are being assessed charges via daily discount.

Another statement indicator of daily discount is batches being shown as gross and net. Statements will have a column indicating total sales (gross), and then they’ll have another column showing what was actually deposited (net).

Ultimately, there’s no “right” answer when choosing between daily and monthly discounting. However, if you’re like most businesses and want to improve cash flow and simplify financial reconciliation, monthly discounting is the way to go.

These articles are great, thank you. What are your professional thoughts on Intrepid Payment Processing? Tiered, or pass through? Monthly, or daily? Professional or shady?

Hi Anthony,

Intrepid Payment Processing isn’t one of the providers who places certified quotes through us, so we can’t guarantee anything about what it offers. Processors can (and do) set rates and terms on a per-case basis, so it can vary business to business. Some companies exclusively offer one pricing model or the other but others offer both, depending on the customer.

That said, it appears that Intrepid uses tiered pricing, and overall it doesn’t have a great reputation. You can read more about it in our Intrepid Payment Processing Review and Profile.

It appears our processor, BBVA, is charging daily discount as we are only receiving the net amounts. On our statements only the interchange fees are shown. I have verified the rates match the Visa and Mastercard interchange tables. What I’m not seeing is any additional fees or charges from the prior month and am therefore unable to determine what we are actually being charged. Are these fees ever listed on a separate statement or could they just be deducted from our bank?

Hi Kevin,

The discounting method used by a processor and its reporting method are two entirely separate things. It’s tough to answer your questions without being able to review the statement in its entirety. There are many ways a processor can build its markup into what appear to be interchange and assessments. It’s rare, but we’ve also seen processors report interchange and assessment costs on a separate statement from its markups. I wish I could provide a better answer, but I’m limited by what I can’t see.

I’d suggest you create a free profile here at CardFellow. Once you get your instant quotes, give us a call and send along a statement for comparison. We’ll let you know exactly what’s going on with your current processor, and how things stack up to your quotes.