First Data Global Leasing, or FDGL, is the equipment leasing arm of processing giant First Data, now Fiserv.

If you’ve browsed CardFellow’s blog, you’ll know we’re not big fans of equipment leasing. In most cases, leases are expensive and come with non-cancellable contracts separate from your processing agreement. Unfortunately, that holds true for FDGL.

What is FDGL?

As noted in the introduction, First Data Global Leasing (often called FDGL) is the branch of First Data (now Fiserv) that leases credit card processing equipment. FDGL only provides the equipment and does not act as your credit card processor. You’ll still need a merchant account from a credit card processor in order to take cards with leased equipment.

Just like a car lease, a credit card machine lease means that you pay to use the equipment for a specific period of time and you will not own the equipment at the end of the lease. When your contract term is up, you can either purchase the equipment (for a fee often close to the original price of the equipment), sign a new lease, or return the equipment.

While leases can be as short as 2 years, a typical lease lasts for 4 years and is separate from your processing agreement. (Meaning, even if you terminate your contract with your credit card processor, your FDGL lease is not automatically terminated.)

In the past, the FDGL landing page on First Data’s site was outdated and unhelpful, providing little information and useless links. (Some links lead to 404 ‘page not found’ errors while others simply redirect to the main First Data homepage or to a client login.) Currently, that landing page is not even available anymore. Googling First Data Global Leading brings up a site still claiming to be FDGL, but with CardConnect, a First Data company, Fairmed branding.

First Data / Fiserv have also removed a previously available FAQ page about leases. However, we’ve had the opportunity to see FDGL leases firsthand here at CardFellow, which allows us to provide insight on both leasing in general, and FDGL.

Machines and POS Systems

First Data Global Leasing provides credit card machines and POS systems that run on First Data’s platform. This includes the FD line of countertop terminals and the Clover line for POS systems, smart terminals, and mobile card acceptance.

All of the equipment you can obtain through an FDGL lease is also available for purchase from First Data-compatible processors and processing equipment sellers.

Are leases required?

No. You’re not required to enter into a leasing agreement for credit card processing or to obtain processing equipment. If a processor tells you a lease is required, end discussions and work with another processor.

CardFellow prohibits leases in our credit card processing marketplace. If you’re looking for the lowest costs on credit card processing and equipment, be sure to create a free profile to see pricing tailored to your business.

FDGL Costs

Like most things in credit card processing, there’s no single answer to “how much does FDGL cost?” The company will set pricing and contract terms individually for your business, based on the machine(s) you choose and other factors.

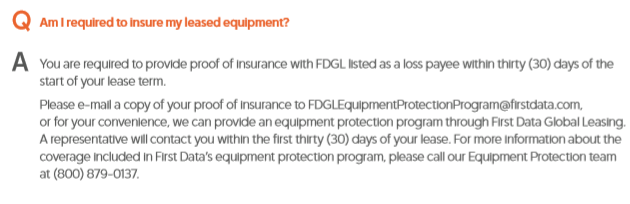

You’ll pay a fixed monthly fee, which is separate from any monthly fees for your merchant account. Additionally, many leasing companies (including FDGL) require you carry insurance on the leased equipment. First Data does not include insurance in its equipment lease rates by default so you’ll need to purchase insurance yourself or opt in to the equipment protection program. The company requires proof of insurance, as noted in this screenshot from the Global Leasing FAQ, no longer available online.

In the cases we’ve seen, FDGL leases are quite expensive. It would be lower cost to purchase a machine outright, even if you need to save up for a couple months to do so. How much more expensive are leases? They’re often double or triple the cost to purchase the same machine outright, but they can be even more expensive in the most egregious cases.

In the cases we’ve seen, FDGL leases are quite expensive. It would be lower cost to purchase a machine outright, even if you need to save up for a couple months to do so. How much more expensive are leases? They’re often double or triple the cost to purchase the same machine outright, but they can be even more expensive in the most egregious cases.

Example

We’ve had the benefit of reviewing FDGL leasing contracts over the years. In one recent example, FDGL offered a Clover Mini at $43.93 per month for 36 months. The lease also included a $150 assignment fee, essentially an application fee.

If this customer opted for the lease, they would pay $1,731.48 for the Mini. That’s $1,581.48 for the 36 monthly payments, plus the $150 initial fee.

On Clover’s own website, the Mini starts around $599.

With the lease totaling $1,731.48 and the machine selling for $599, this customer would pay a whopping $1,132.48 more than if they purchased the Mini outright at the manufacturer’s retail price.

Even worse, Clovers can’t be reprogrammed, so if the customer wants to switch processors, they will not be able to continue using the machine they’re leasing. The customer would essentially be stuck with their processor if they want to use the Clover, or stuck paying for a second machine if they wanted to switch processors.

Are leases ever a good idea?

We haven’t seen one yet.

In theory, if a leasing company offered you a monthly fee low enough that the total of all payments was close to the total to purchase the same equipment outright, it might not be a bad deal. In reality, that’s almost never how it works out. Leases are designed to make money for leasing companies at your expense.

Additionally, since you’ll either return the equipment or pay more at the end of the lease, you’re not really paying toward equipment ownership.

Alternatives to Leasing

Instead of signing an expensive equipment lease, consider purchasing outright or at least finding a fair, low cost rental option.

When you sign up for credit card processing through the CardFellow marketplace, you’ll have the option to purchase equipment from the processor you choose. Within CardFellow, processors offer equipment at or near cost to keep your out-of-pocket expenses low.

In some cases, you may be able to purchase a machine online instead, but be sure to check with the processor about compatibility before doing so. The compatibility with some machines can be very specific, even down to the serial number.

A warning on low online equipment costs: You may see credit card machines for very low prices online, including from some sellers through sites like Amazon. Be aware that in some cases, the seller only offers the machine at that price in exchange for you signing up to process through their company. In those situations, the rates for processing are higher than you’d otherwise pay, leading to a more expensive deal overall.

Purchasing vs. Leasing

When possible, purchasing your equipment outright is the best solution. It will be a one-time purchase instead of ongoing, and you can easily compare prices from different sellers.

With leasing, you’ll need to do the math yourself to determine the final cost of the machine. Don’t be fooled by a “low” monthly payment.

Keep in mind that the monthly cost is not related to the retail cost of the machine. In other words, monthly costs for a lease aren’t the retail cost divided by 48 months. Instead, they’re a monthly payment designed to seem reasonable but add up to a more expensive total cost over time.

In the 36-month Clover Mini lease we discussed above, the machine retails for $599. If the lease broke out the cost into monthly payments, it should have been $16.64/month. Instead, it was $43.93/month, or almost three times as expensive.

Additionally, leases are an easy way for leasing companies to make more money on lower cost equipment, like countertop terminals. A credit card machine may cost less than a POS system to purchase outright, but can be the same (or even more) when leased. Always remember that the monthly cost is not necessarily related to the retail cost of the machine if you purchased it outright. A credit card machine may cost less than a POS system to purchase, but can be the same (or even more) when leased.

Renting vs. Leasing

Some processors offer to rent equipment, often on a rent-to-own basis. This can be okay, depending on the terms of the agreement and the rental fees you pay. The best situations will be ones where you pay close to the wholesale cost of the machine, but simply split up the payments over a number of months.

For example, if a POS system retails for $1,000, a beneficial rental would charge $21/month for 48 months, totaling $1,008 at the end of the rental period.

Getting Out of an FDGL Equipment Lease

Ending equipment leases prior to the end of the contract term can be quite difficult. Leasing companies can pursue you in court for violating contracts if you don’t approach it correctly. If you’re looking to get out of an equipment lease, it’s crucial to contact a licensed attorney to go through your contract. Do not simply close your bank account to cut off payments to the leasing company, as that will not end your contractual obligation, and may lead to late fees, pursuit in court, and other headaches.

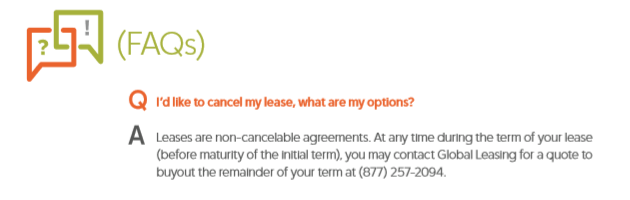

If you just want out and don’t mind paying for it, FDGL will allow you to ‘buy out’ your lease.

As the screenshot from FDGL above explains, you can contact the company before the end of the initial contract term for a quote to buyout the remainder of the contract. Keep in mind that buyouts may not be equal to the amount remaining on your lease.

If possible, avoid leasing in the first place to save yourself the frustration.

Have you used FDGL at your business? Let us know your thoughts by leaving a review in the comments!