Processor Directory > North American Bancard

North American Bancard Review

Based in Michigan, North American Bancard maintains two websites, which can make it a little annoying to find the info you’re looking for. Read on for our review, which brings together all the vital information you need to find out if they’re the right merchant services provider for you.

If you’re looking to know what others think, jump down to the “Reviews” section at the end of this article to get additional insight.

- News

- Overview

- Types of Cards Accepted

- Free Equipment

- Payment Methods

- Rates and Fees

- North American Bancard Reviews

News

In late 2017, North American Bancard announced that it will be acquiring Total Merchant Services.

Overview of North American Bancard

North American Bancard is a merchant account provider. This means it allows you to take payments from customers with debit and credit cards and processes them on your behalf. It then deposits money in your bank account after taking its processing fees. The North American Bancard merchant account is primarily designed for face-to-face retail transactions. Although they do allow ecommerce transactions, face-to-face transactions are what we’ll focus on in this review.

North American Bancard in Their Own Words

“A merchant services account from North American Bancard (NAB) will allow you to accept credit cards at your business. We pride ourselves on offering some of the lowest credit card processing rates in the industry, and our merchant accounts come with a month-to-month service agreement with no cancellation fees.”

NAB — Key facts

- Used by over 250,000 businesses throughout the US.

- Processes over $34 billion in transactions every year.

- Have been a payment provider for over 20 years.

- North American Bancard partners with Wells Fargo bank.

Types of Cards Accepted

NAB allows you to accept the following types of debit and credit cards:

- Mastercard

- Visa

- American Express

- Discover

- PayPal

- Fleet cards (including Voyager and Wright Express)

Some of their payment processing devices also let you accept gift and voucher cards. Their machines can process cards from around the world, as long as they’re on one of the networks listed above.

Related Article: Taking PayPal in Stores.

Other Services

In addition to credit card processing, North American Bancard offers ATM installation onsite (providing the terminal, software, and support) and merchant cash advances. Called Capital for Merchants, the cash advance program offers up to $500,000 per location for approved business expenses.

Free Equipment

NAB claims to provide free point of sale (POS) equipment, including complete card readers, card swipers for taking payments on the go, and several other options:

- Countertop credit card readers.

- EMV and NFC compliant for chip cards and contactless payments.

- A “PayAnywhere” storefront tablet

- A swipe reader that plugs into a mobile phone or tablet

Equipment comes pre-programmed for your specific business, so you can just plug it in and go. NAB recommends connecting your card reader via the internet. If you don’t connect through the internet, you will need a dedicated landline telephone line to process transactions.

NAB has a dynamic app that works with their mobile card readers so you can take payment quickly and easily.

It’s very important to note that although NAB claims that equipment is free, the experiences of their customers vary. For example, some report that NAB charges purchase fees for equipment, or actually leases machines. If you are thinking of signing up with NAB, make sure you understand if you need to pay for equipment, and how much.

Related Article: The Dangers of “Free” Credit Card Machines.

Payment Methods

Most NAB equipment is enabled for various different payment methods. This includes swiping, NFC, and EMV.

- NFC stands for “Near Field Communications.” This technology lets customers make quick, secure payments through a “contactless” method, using special chips embedded in their credit card and the NAB merchant terminal.

- EMV, more commonly known as “Chip and Pin” or “Chip and Signature” is a technology that uses a chip on the front of a customer’s credit card. Customers insert their card into a credit card reader (called dipping) which uses secure encryption to process payment information.

- All NAB card readers can process cards that are “swiped” with their magnetic strip. Although EMV and NFC are becoming more popular payment methods, not all businesses accept EMV payments yet. Non-traditional retail settings (e.g. taking payments via a mobile card reader) aren’t always chip or NFC enabled.

- Naturally, your customers will also have to sign or enter their PIN to authorize payment.

Additionally, North American offers tip adjust for accepting chip credit cards and adjusting the total for tips after the fact. That’s particularly important for restaurants, bars, cafes, hair salons, and any business where tips for employees are a common practice. Here’s NAB’s video on tip adjust:

The ability to adjust for tips is becoming more common on machines capable of accepting EMV chip cards, but if tips are important to your business, it’s a good idea to verify with your potential processor that the machine you use (or are looking to purchase) will allow adjusting for tips. Otherwise, you can still take tips, but you’ll need to ask your customers to enter the tip while their card is still in the machine.

NAB Countertop Credit Card Machines

North American Bancard provides a variety of countertop credit card machines, all of which are fully PCI compliant, using the latest technology to encrypt and securely process transactions.

The currently available selection, listed here with NAB’s suggested ideal use, is included below.

Verifone Vx 520

“A rugged and reliable countertype device that’s built for everyday use.”

See: Vx 520 Features

Verifone Vx680 Wireless

“A portable, handheld device[…]perfect for mobile merchants, delivery services, stadium vendors, and pay-at-the-table restaurants.”

See: Vx680 Features

Ingenico iCT220 CL

“Among the world’s smallest credit card terminal devices and is designed for easy handling and rugged everyday use.”

See: iCT220 Features

Verifone Vx570 DC

“A countertop solution that blends speed and performance and can support value-added applications and EMV chip card transactions.”

See: Vx570 Features

Verifone Vx510

“A space-saving credit card terminal that is easy to install and[…]comes with a high-speed printer that reduces wait times.”

See: Vx 510 Features

Remember to ask whether you’ll be expected to pay for equipment outright or if there is a lease, and double check that your contract says the same thing that you’re told by the sales rep.

Related Article: Is leasing a credit card machine the biggest mistake you can make?

Getting Approved for a North American Bancard Merchant Account

You will need to complete an application form for an NAB account. Accounts are approved within hours and completing basic setup takes fewer than 15 minutes.

Training

North American Bancard provides training for you and your employees on using credit card terminals and reprogramming them if needed. They also have several resources on their website, pictured below.

NAB Payments

You will normally have money transferred to your bank account within two working days of taking payment from your customer. Some merchant accounts can qualify to have funds deposited the next working day. Note that funding times is something that came up in some customer complaints. A few reviewers commented that funds were not always available when promised.

Rates and Fees

This is where things get a little tricky, and a big part of the complaints in North American Bancard reviews. Like all processors, NAB prices its services on a “per business” basis.

If you look back at the screenshot of North American’s homepage, you’ll see that the company claims “low rates” starting at 0.29%. It’s very important to note that this DOES NOT mean that you’ll pay 0.29% to process transactions. “Rates” are only one part of the total cost of credit card processing, and are easily manipulated. Additionally, the starting rates North American publishes indicate a tiered pricing model – an opaque and expensive type of pricing. The second North American website lists rates “starting at” 0.19% so the same caveat applies. You will pay much more than 0.19% of each transaction.

North American Bancard doesn’t disclose full pricing. You can request a full price quote from NAB by using the CardFellow quote request tool. (It’s free, private, and there’s no obligation – Go ahead, it doesn’t hurt to look!) Click here for the quote requester.

NAB states that there are no startup or cancellation fees, no hidden fees, and no long-term contracts. The company may charge for PCI compliance.

It’s worth nothing that although NAB claims the above on their website, the experiences of their customers vary. For example, some report that NAB charges a termination fee and other undisclosed fees. If you need help understanding your pricing from NAB, let us know.

Related Article: How to Read Your Credit Card Processing Statement.

"Cutting Edge" Pricing Program

North American Bancard also offers a surcharge program, the Cutting Edge program, to pass along processing fees to your customers rather than charging you. While the company refers to it as a cash discount program, it's actually a surcharge because a fee is added at the time of purchase if your customer uses a card. (By contrast, a cash discount program is when you provide a discount at the time of purchase if a customer pays with cash.)

In any case, the surcharge program offers flat rate pricing, starting around 3.8%. Confusingly, North American Bancard says that the customer would then be charged 4%, and says that your business would make money on the transactions. However, card brand regulations specify that the cap for surcharges is 4% or the actual cost of processing, whichever is lower. By charging 4% to the customer and only 3.8% to the business, North American is setting your business up to violate card brand agreements. If you're considering North American's Cutting Edge cash discount program, you'll want to clarify this rule discrepancy to protect your business.

Read more about adding a fee to credit card purchases.

Chargeback Fees

Like most processors, NAB imposes a “chargeback fee” if a cardholder disputes a transaction that’s been charged to their card. According to their website, “Reasons for chargebacks include a cardholder dispute or an error in handling on the part of a merchant’s staff. Obtaining proper authorization and adhering to correct processing procedures can minimize chargebacks.”

NAB Clients

North American provides credit and debit card transaction services for brands that are household names including:

But remember, what’s good for one company might not be right for yours. Be sure to carefully review your options before choosing a credit card processor.

Awards and Recognition

- A+ rating with the Better Business Bureau.

- Certified Payment Professional staff.

- 2008 Ernst & Young Entrepreneur of the Year, Detroit Region

North American Bancard Reviews

Take credit card processing reviews with a grain of salt. Processors set pricing and terms on a per-case basis, so the reviews you read from others won’t necessarily be the same as your experience. That said, it can still be helpful to at least get a basic overview of what others think. Here’s a selection of North American Bancard reviews. from around the web.

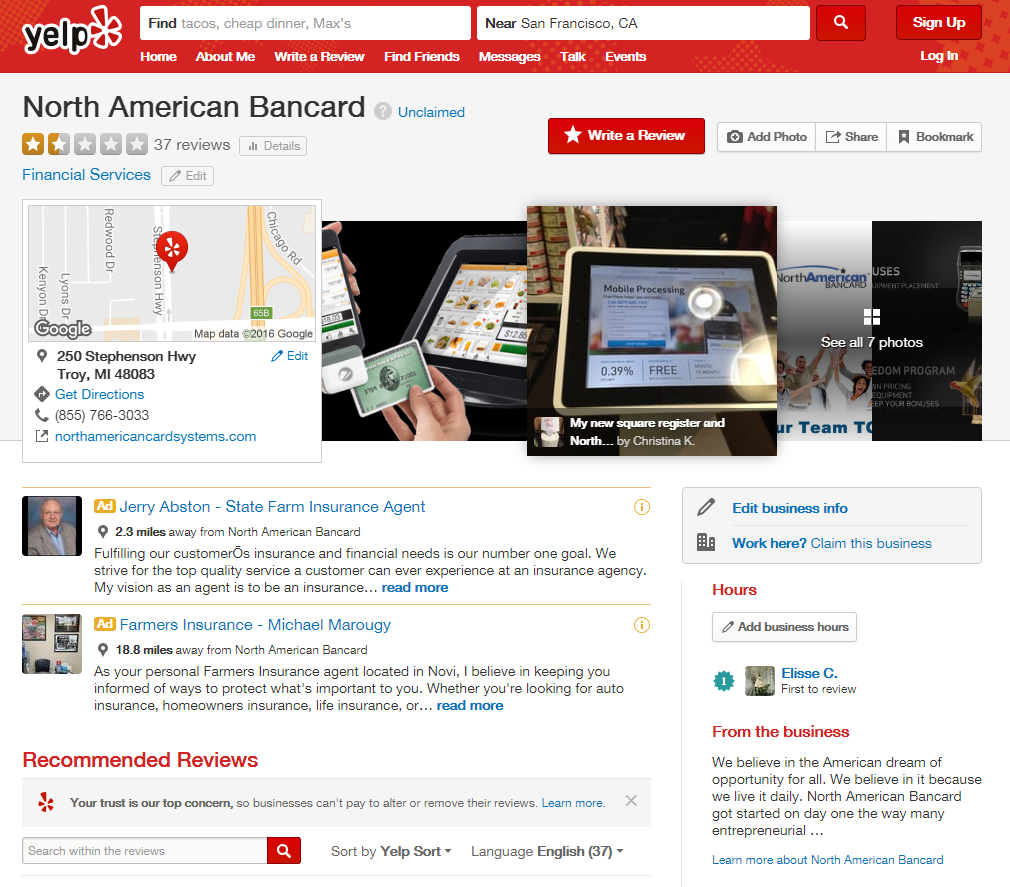

Yelp — 37 reviews, average of 1.5 out of 5 stars

As of autumn 2016

In the Yelp reviews, some accuse the company of being a scam, of needing better training on honesty and transparency, and unexpected fees. One reviewer expresses regret that they didn’t check the reviews before signing up, and have had a negative experience.

Others claim to have had positive experiences, competitive rates, and helpful staff. One reviewer expresses surprise to see so many bad reviews. (This is a classic case of how one business could have good pricing and terms, but not necessarily be representative of what you’ll get.)

Better Business Bureau — A+ rating; 244 complaints in 3 years; 23 Reviews

As of autumn 2016

There’s a lot to dig in to at the Better Business Bureau’s website. North American Bancard has an A+ rating with the BBB, despite 244 complaints in the last 3 years. As you can see from the screenshot below, the majority of the complaints are in the “’Billing/Collection Issues” category, with another big chunk listed as “Problems with Product/Service.”

Curiously, none of the complaints are visible. All 244 are listed as “Complaint Details Unavailable.” In our experience examining hundreds of BBB profiles, we’ve never seen details unavailable for every complaints in a company’s log. The BBB makes no indication of why complaint details aren’t available, so we’re not able to give a reason for that.

Fortunately, details of the 23 customer reviews are available. The one positive review simply says “hi” and therefore offers nothing helpful. The 22 negative reviews express many of the same sentiments as the Yelp reviewers, including hidden or excessive fees and poor customer service. Some reviewers complain about long (2- or 3-year) agreements, monthly service fees, or undisclosed and hefty early termination fees. For that last one, some reviewers state that they were charged $840, $1,000, or $2,000 to cancel. The different amounts indicates a liquidated damages clause, meaning that the earlier you try to cancel, the more you’re likely to end up paying to get out of the contract. Some reviewers also reference difficulty cancelling and claim that NAB continued to debit their accounts after cancellation. Additionally, some reviewers complain that equipment advertised as free was not actually free.

These troubling reviews are in direct contrast to North American Bancard’s claims (on its website) of no long-term contracts and no cancellation fees. Some reviewers on the BBB site warn that some of these details are in the fine print of the contract, so be sure to read it carefully. Remember, the contract you sign will generally trump verbal promises made by sales reps, so don’t assume that you’re covered just because a rep tells you something you want to hear.

In addition to the complaints from current and former clients, some reviews are from businesses that say they didn’t sign up with NAB, but experienced continuous emails or phone calls. Reviewers lamented the unprofessional aggressive sales practices.

Related Article: Don’t be a Sucker About Credit Card Processor Reviews.

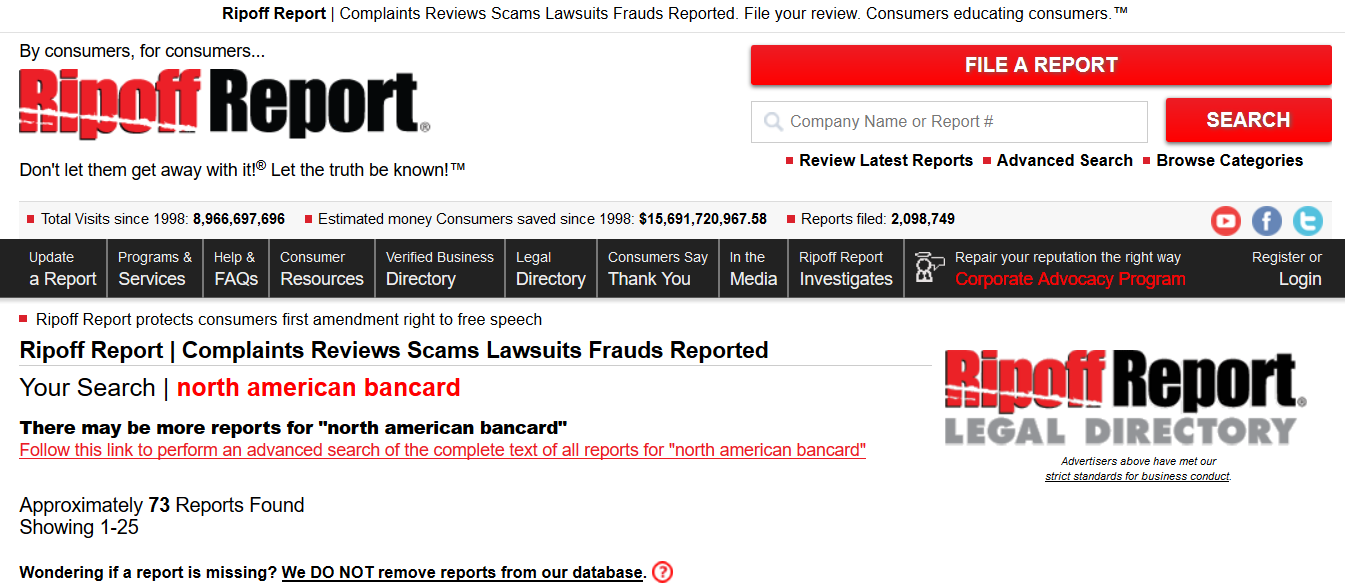

Ripoff Report — 73 Reviews

As of autumn 2016

As the name implies, Ripoff Report provides a space for customers to explain their negative experiences with a business. This is obviously self-selecting, as customers that may be inclined to leave a good review will likely not do so on a site called the Ripoff Report. So, the 73 reports available are from customers that think North American Bancard is a scam, ripoff, or at least not the right company for their needs.

In addition to the comments about NAB as a scam or ripoff, customers complain of hidden and unexpected fees, undisclosed monthly minimums for processing or additional fees will be imposed, unexpected debits from bank accounts years after no activity from NAB, non-working equipment, unauthorized debits, and difficulty cancelling contracts.

Other North American Reviews

People who are angry with a company often go to great lengths to share their experience, which is probably why a Facebook group called Bad Business Practices: PayAnywhere/North American Bancard exists. The page has a few complaints that echo the ones on Yelp and other review sites. The page is not very active, with most recent posts dating back to 2015.

A website called Complaints Board also includes a detailed complaint about North American, which is answered by someone representing the company.

At this time, neither of North American’s websites include any customer testimonials to rebut the abundant negative reviews. We’ll check in with review sites and the company’s website regularly and update this overview if testimonials or additional negative reviews become available.

We hope this has given you a comprehensive overview of what North American Bancard does. Unfortunately, despite the claims on their website, the experiences of their customers (at least those who wrote reviews) does seem negative. Of course, there may be many thousands of customers where there were no issues but we recommend carrying out your own research before making a final decision.

Does your experience with North American Bancard line up with the positives or the negatives? Let us know by leaving your own review!

SATISFACTION

RATES & FEES

CUSTOMER SERVICE

0/5

Unlike general web reviews, verified reviews are posted by businesses that have chosen the processor's quote through CardFellow's marketplace, and CardFellow has confirmed with the processor that the business is using its service. Businesses can update verified reviews at any time to ensure the review accurately reflects the processor's performance over time.

SATISFACTION

RATES & FEES

CUSTOMER SERVICE

1.6/5

Unlike verified reviews which are validated by CardFellow, web reviews can be submitted by anyone viewing this profile. While we validate these reviews as best we can, CardFellow does not verify that a reviewer is using or has used a processor's service.

Do you Know this processor? Write a review about it

Posted by Michael Anerson on Aug 11, 2023

SATISFACTION

RATES & FEES

CUSTOMER SERVICE

1/5

If I Could give them a Zero Star I would! They reached out to my business stating they have a new program for high risk processing of the products peptides that will accept VISA, MASTERCARD, AMERICAN EXPRESS, and DISCOVER.

Posted by Stephen Benton on Feb 11, 2023

SATISFACTION

RATES & FEES

CUSTOMER SERVICE

1/5

I agree with the negative reviews. This company rips you off. They take money out of the account that they never reveal when you initially sign up through Sekure. I got out of a contract without penalty because I was very firm with the agent at Sekure and she handled it. But I've been waiting on N. Am. Bancard over a month for a refund on fees that should not have been charged. They drag their feet, & overcharge as often as possible. Don't give them access to your bank.

Posted by Harvey Wrantz on Feb 14, 2019

SATISFACTION

RATES & FEES

CUSTOMER SERVICE

4.7/5

I got a great deal at only 0.50% above cost and free equipment. Customer service is a little slow sometimes but my agent handles everything for me now.

Posted by Art on Jun 20, 2018

SATISFACTION

RATES & FEES

CUSTOMER SERVICE

0.5/5

This company is a ripoff - I had their processing terminal at my business. Their fees and their charges are high and they love charging your bank account every month. I was held to a contract; I try to get out of it and they told me the buy out was $2,800. I asked the person if the terminal was really worth that much money - they tried to tell me it was worth more. My biggest issue was that we did a transaction and pushed a wrong button. The customer owed me about $675 and the refund button was right next to the sale button and I accidentally hit the refund button, but didn't know it. Customer got a refund of $675. When I finally figured out what happened I called them and told them what happened which was a surprise because they never notified me or even called me or sent me anything in email or anything else. I was told that when you hit a refund they usually ask you, so I told them what happened. They told me to contact the customer. I asked them to run the number through again because I know they have it on their end and they wouldn't. It took me some time to get in touch with the customer and of course by the time I did and told him what happened and asked him to stop by and run the credit card again, he never showed up. I called North American Bancard back told them and they said they can't help me. I'll tell you that's some great customer service, not only did he get a refund for $675, I was never paid so I lost $1,350 and they didn't even act like they care, they didn't do anything for me it was like oh well they basically said there was nothing they could do for me. So chances are - if those terminals are set up the same way it's been a couple years since this happened - if you accidentally hit the refund button they will take the money from your bank account and give it to the customer and you will lose they will not do anything for you because they don't care, the only thing they care about is hitting you with fees and charges every month from your bank account. The joke of this is when my contract ran out they wanted to know why I was switching merchant services and going with somebody else, can you believe that? I wouldn't give them one star.

Posted by Mallory Johnson on Mar 09, 2017

SATISFACTION

RATES & FEES

CUSTOMER SERVICE

1/5

Held a large amount of our money for multiple transactions, even though I was advised the hold was for one single charge. Gave them all paper work, plus months of our bank statements to release, it took them over a week. We are in healthcare so chargebacks never happen yet we were treated like we were a high risk seller. Found hidden fees on my account. Monthly charge for getting my statement and a monthly charge for logging onto the website to retrieve the statement. Statement itself is confusing and they don't pull charges out end of month, they do it per transaction, which makes balancing your accounts incredibly difficult!

Posted by Abraham Romo on Jan 05, 2017

SATISFACTION

RATES & FEES

CUSTOMER SERVICE

1/5

I have called to cancel this service multiple times years ago for a business I no longer have. They would not cancel because I didn't sign a cancellation paper. They did not send me this paper. Finally today (years later) I realized that my old business account was over drawn and they were still charging me. When I called today they said they would cancel the account without me signing anything, and refund 3 months of payments. But they would not refund 3 years of payments taken from my account after I had called multiple times to cancel. They have admitted they can see from their records that I have not used their service in over 4 years and they can also see that I have called multiple times in the past to cancel. Very frustrating.

Posted by CardFellow on Mar 08, 2016

SATISFACTION

RATES & FEES

CUSTOMER SERVICE

2/5

We've seen North American Bancard use every trick in the book from overcharging assessments to charging a discount on return volume. It markets and sells its services directly and through a network of independent sales agents (ISA) and resellers.