Costco may sell some things at wholesale prices, but it’s not merchant accounts.

In fact, Costco doesn’t even provide credit card processing. Instead, they outsource merchant services to a company called Elavon.

In the past, Costco offered merchant accounts using tiered pricing with bait and switch rates. In short, you will pay through the nose to process credit cards, and you’ll likely be stuck doing it until your multi-year contract expires.

At the time of this update in autumn 2023, Costco still offers its opaque tiered pricing structure, but it also offers two other pricing types: flat rate, and credit card surcharging. We’ll start with the tiered pricing model and then provide details on the other two.

Note: this article focuses only on Costco’s merchant services rates and fees. You can get a full review of Costco’s processing services in our Costco credit card processing review.

Tiered Pricing

Costco’s merchant accounts have traditionally used tiered pricing, and that it still available and promoted readily on its website. On a tiered pricing scheme a processor (in this case Costco’s partner Elavon) groups interchange fees into several tiers called qualified, mid-qualified and non-qualified. By doing so, they’re able to mask the true cost of processing while increasing profits.

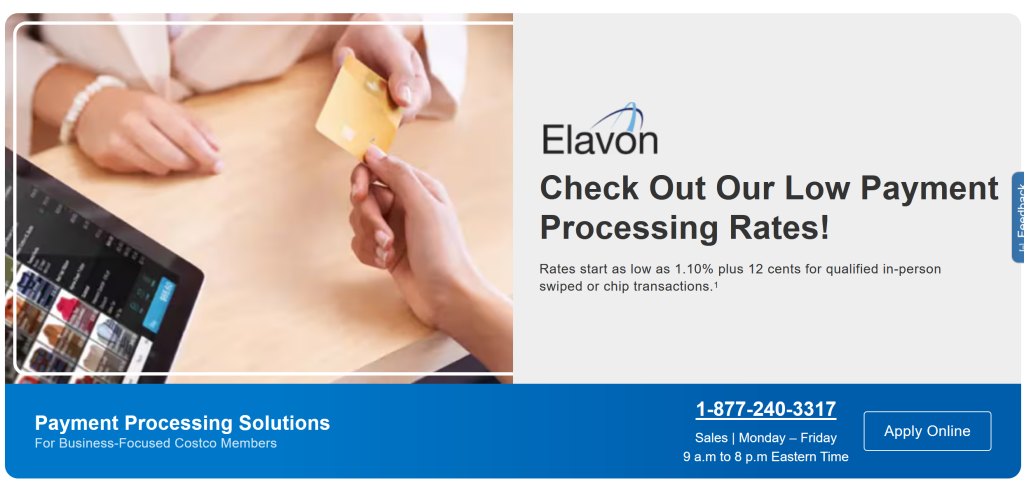

I’ll explain exactly how processors game the system with tiered pricing in just a moment. For now, check out this screenshot taken from Costco’s website and I’ll show you how to spot tiered pricing.

Tiered pricing is always quoted as a percentage and a flat transaction fee, and the qualified rate is typically close to or slightly greater than the lowest credit interchange fee. For example, this screen grab from Costco’s website shows a qualified rate of 1.10% plus $0.12 for in-store transactions. (A subsequent section shows 1.90% + 25 cents for online transactions.)

This leads us to believe that those in-store transactions should be charged a fee of 1.10% plus $0.12. But, as you can guess, it’s not quite that simple. The screenshot also has a “1” at the end of the sentence, directing you to fine print. When you scroll down to find that fine print, it states that the rates are for “qualified” transactions, and mentions “rates and fees may change without notice.” Not a great start.

Inconsistent Buckets

The real sliminess of tiered pricing is showcased in something called inconsistent buckets. Inconsistent buckets is the processing industry’s term that describes why it’s impossible to compare tiered rates among processors.

As the name implies, inconsistent buckets refers to a processor’s ability to route interchange charges to the pricing tier of their choice. In this case, Costco is advertising a “qualified” rate of 1.10%, but they’re not telling you which interchange categories are routed to the “qualified” tier. Costco (or rather, Elavon) won’t consider all of your transactions “qualified.” They can decide which transactions to charge according to the “qualified” rate published and which to charge according to higher, unpublished, “non-qualified” rates.

Let’s pretend that we know Costco’s processor is routing only consumer debit cards to the qualified tier, and all other transactions are being routed to the mid-qualified and non-qualified tiers (the rates for which aren’t disclosed on their website).

Let’s also pretend that we’re considering another processor that’s advertising 1.69% for a qualified rate, but they’re routing consumer debit, credit and rewards card to the qualified tier. Costco’s offer appears to be the better deal superficially, but the second processor would actually be less expensive.

We’ve got an article over here that explains the differences of tiered pricing compared to interchange plus — a more transparent form of pricing.

Costco’s Bait-and-Switch Rates

So, Costco is advertising 1.10% plus a $0.12 transaction fee on their website. This seems too good to be true considering that 1.10% is lower than the rate that banks charge processors (interchange rate). That means that Costco would actually lose money, as they would be charging less than wholesale cost.

Here’s a screenshot of Visa’s interchange fee schedule (the lowest possible credit card processing fees). As you can see, the lowest standard credit interchange fee is 1.54% plus $0.10. Costco is obviously not losing money on every transaction, so how are they able to offer 1.10%?

The answer lies in the fine print (as always) on Costco’s site. As noted earlier, there’s clarification that the rate published is only for qualified transactions and does not specify (as processors typically don’t) which transactions “qualify” for that rate. Let’s dig in to that a little further.

Qualified Transactions

There’s a whole lot of bad stuff going on here, but for now, let’s focus on the sentence that says, “Rates listed are for qualified transactions.”

Okay, so the 1.10% is only for qualified transactions. So where does Costco tell us what’s qualified? And since other cards will be processed at a higher rate, what’s the higher rate? That information is nowhere to be found. This is a pretty important detail when considering that reward cards typically account for 50-60% of total credit card volume.

In the interest of transparency, Costco should have phrased their disclaimer paragraph as such:

“The 1.10% rate used to advertise our merchant accounts makes our processing services look way better than they actually are. Realistically, you will pay a mid and non-qualified rate on many of your transactions. However, we’ve decided not to list those rates because they are a lot higher than the 1.10% qualified rate, and they would make it obvious that we’re using bait-and-switch marketing tactics to take advantage of our customers.”

Doesn’t that read a little more true to form? If you’re still considering Costco for a merchant account after reading this, be sure to ask them what the other rates are before signing any agreements.

Cancellation Fees

Let’s pretend for a moment that, like many people, you signed up for a Costco merchant account before you knew how horrible they are. It’s not a big deal, right? You can just cancel the account and find a processor that offers more reputable rates and interchange plus pricing.

Surprise! You could be locked into a three-year contract with a hefty merchant account cancellation fee. Costco’s partner, Elavon, isn’t stupid. They know they’re selling overpriced processing services, so they need a way to keep people around once they realize they’ve been had.

The perfect solution is a tactic used by many processors — the dreaded cancellation fee. This leaves businesses with two choices — stay and overpay for processing, or leave and pay a hefty cancellation fee. Either way, Elavon profits nicely.

There’s no reason for a processor to impose a cancellation fee if they’re offering honest, competitive rates.

Marketing Tactics

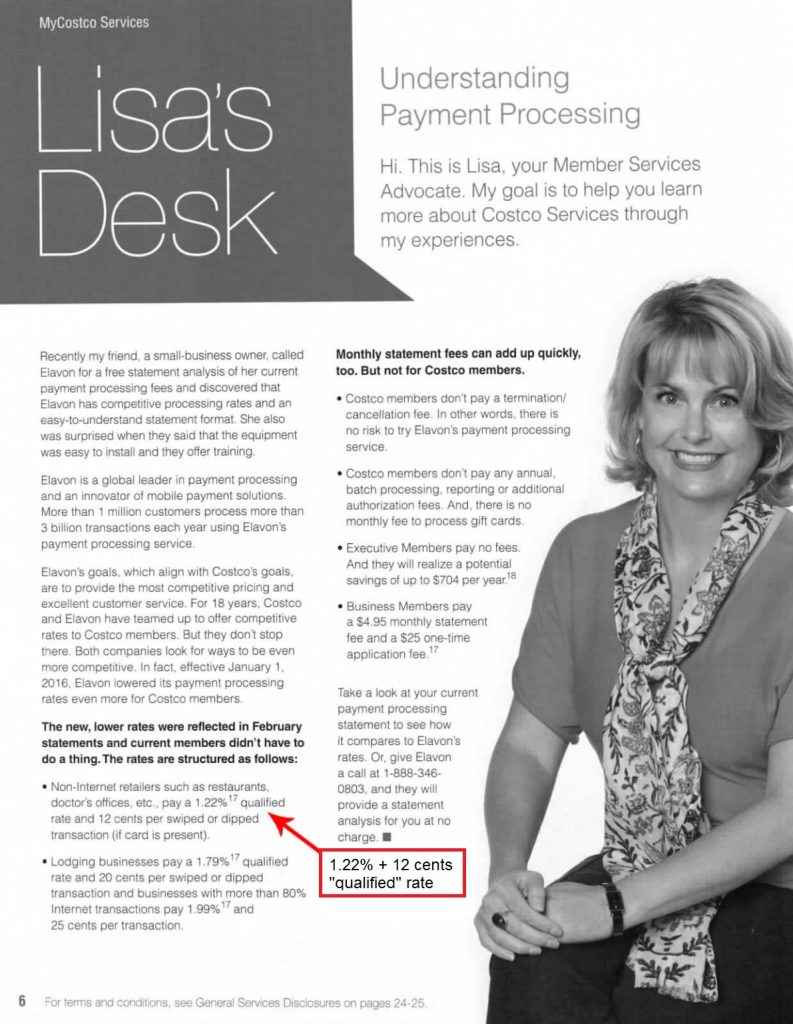

Costco actively pushes its credit card processing, including through its customer magazine. The Spring 2016 issue, pictured, includes a full page ad dedicated to telling you that the pricing is competitive and the service excellent. There’s a nice anecdote about a happy customer, and a smiling Costco rep. It even includes the great news that Costco and Elavon have lowered pricing even further than in the past. The qualified rate quoted is a mere 1.22% + $0.12 per transaction! Since that time, Costco and Elavon have “lowered” the rate even further! But of course, that’s not what you’re going to pay. The fact that the company can continuously “lower” the rate, which was already below the wholesale cost of processing, should indicate just how easy it is to manipulate tiered pricing.

As with disclosures on the website, the ad doesn’t provide details about what transactions “qualify” for that low rate. Since the qualified rate is below cost, it’s safe to assume that very few transactions will ever qualify. Instead, you’ll end up with more expensive “mid-qualified” and “non-qualified” pricing, which is conveniently omitted from the ad and disclosures.

Do yourself a (big) favor and steer clear of Costco’s tiered pricing credit card processing catastrophe. Find the best credit card processing here at CardFellow by getting multiple quotes from reputable processors instantly. No cancellation fees, no “qualified” transactions, just competitive pricing.

Costco Flat Rate Processing

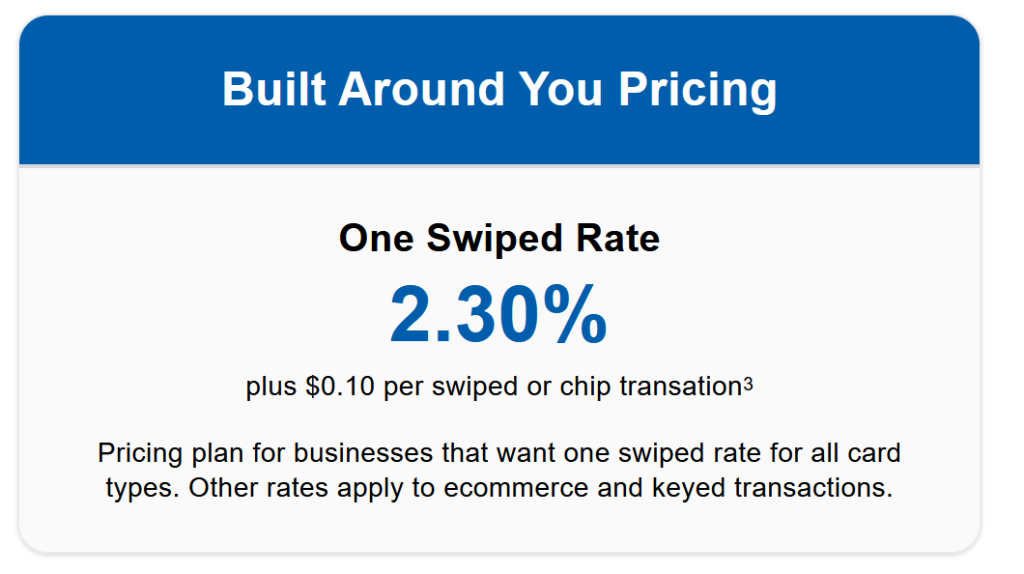

In the past, Costco has only offered the tiered pricing structure discussed above. However, the company now also offers a flat rate option, listed on its website as Built Around You pricing.

The flat rate option shown is 2.30% + 10 cents per transaction. The idea is to eliminate the qualified / mid-qualified / non-qualified “tiers” of its traditional pricing and instead offer one rate for in-person transactions. This type of pricing became popular when companies like Square and Stripe pushed it as a simpler solution. (Note: They’re not wrong. It IS simpler. However, simpler doesn’t automatically mean it is the lowest cost. You can read more about that in this article on flat rate pricing.)

In this case, the “3” indicating fine print is less onerous than it is with the tiered pricing. It provides the details on ecommerce and key-entered transactions, which are 2.60% + 10 cents and 3.20% + 10 cents per transaction, respectively.

Those rates put Costco’s flat rate processing lower than many competitors. (Square is currently 2.60% + 10 cents per transaction for in-person while Stripe’s online transactions come in at 2.9% + 30 cents. Many flat-rate processors charge 3.5% + 15 cents for keyed transactions.)

If you’re looking for the simplicity of flat rate, Costco may be a good option.

Costco Surcharge Processing

Another new plan that Costco offers for credit card processing is a surcharge pricing plan. With this type of pricing, you directly transfer the cost of processing credit cards to your customers. (You still pay for debit card processing.)

Credit card surcharging is legal in almost all states, provided you follow certain rules. One of those rules is a cap on the amount that a customer can be charged. That is currently 4% or the actual cost of processing, whichever is lower. (Note: Visa has recently changed its cap to 3%.) Additionally, businesses are required to inform customers in advance of the surcharge and to list it as a separate line item on receipts.

Costco’s surcharge program simply makes it possible to institute the surcharge directly through your processing equipment. Currently, the surcharge rate is 3% – that is, when your customers pay using a credit card, they will incur an additional 3% charge to their bill. This amount keeps you within Visa’s cap.

Surcharges are not permitted by law on debit card transactions. However, debit cards still incur processing fees. On a surcharge pricing plan, you’ll pay for debit transactions. Costco charges 1% + 25 cents per transaction to process debit transactions.

In some cases, businesses have found consumer disapproval of surcharges. Be sure to consider any impacts on your customers and whether they have easy alternatives with companies that haven’t implemented surcharges. You can read more in our article on credit card surcharging.

Still not sure which pricing model or processor is right for you? CardFellow can help. Give us a call or sign up for free at cardfellow.com!