Learn how to navigate the credit card processing maze to secure the most competitive pricing and solution for your dental practice.

As a dentist, orthodontist, oral surgeon, or dental professional, you know that accepting credit and debit cards is convenient for patients and can eliminate the time and expense of sending invoices to collect payment.

But many practices overpay for credit card processing, either by choosing practice management systems that lock them into higher rates or not knowing how to get lower costs that remain competitive over the long term.

To complicate things further, practices have to consider factors that other businesses don’t have to deal with – things like HIPAA compliance, accepting HSA and FSA cards, and integrating with practice management systems.

We’ve got you covered.

This complete guide to credit card processing for dental practices tells you everything you need to know about credit card processing. By the end, you’ll be able to confidently navigate processing and learn how to choose a credit card processing solution that fits your needs and your budget.

There are several terms we’ll use throughout this guide.

- Interchange

The portion of credit card processing fees that go to the banks that issue credit cards to your patients.

Assessments

The portion of credit card processing fees that go to the credit card brands.

- Credit Card Processor / Processor

The company that facilitates credit and debit transactions for your practice.

- Markup

The portion of credit card processing fees that go to your credit card processor.

- Virtual Terminal

A secure method of accepting credit cards using a computer and a swiper instead of a dedicated credit card machine.

What is CardFellow?

Who are we, and why you should take our advice about credit card processing? Good question!

CardFellow is the leading resource for businesses looking for the right credit card processing solution. We help in two ways: through our educational blog where we post unbiased, accurate information about credit card processing without the sales jargon, and with our powerful free quote engine that allows you to quickly and easily compare pricing details from multiple credit card processors.

Check out CardFellow’s blog for a ton of comprehensive articles on all aspects of taking credit cards. When you’re ready to see real numbers for your practice, check out our quote comparison tool. It’s fast, free, and we don’t share your contact information.

CardFellow has been helping practices like yours find the right processor since 2006. Our comparison marketplace features CardFellow-certified quotes backed by a legal agreement with processors. We require a lifetime rate lock, no cancellation fee, transparent pricing models, and more. We also provide free ongoing statement audits to ensure your pricing never increases.

Think of us as your independent experts, here to answer questions without the usual sales spin. We’ll help you find the right processor so you can get back to focusing on what matters most: your patients.

Credit Card Processing for Dentists: The Basics

When accepting credit cards, the basics stay the same whether it’s a retail store, restaurant, or your dental practice. To take credit cards, you’ll need what’s called a merchant account with a credit card processing company. Every time you take a card for payment, you’ll owe a portion of that transaction to the credit card processor, who in turn will pay the banks and card brands.

Don’t think of credit card processing cost in terms of “rates,” and don’t compare processors based on “savings,” or even based on total estimated cost. As we’ll explain below, the key to properly conceptualizing processing cost is to follow the money.

There are three components of credit card processing costs: interchange, assessments, and markup. As noted in the glossary, the interchange charges go to the bank that issues credit cards to your patients. The assessment fees go to the card brands, such as Visa and MasterCard. The markup is what your processor charges for facilitating the credit card transaction for you.

Interchange and assessments are non-negotiable. They’re also the same for every processor. For those reasons, you can think of interchange and assessments as the “wholesale” cost of credit card processing. As with anything, the company selling services to you (in this, case a credit card processor) adds a “markup” to the wholesale cost so that they can make money.

Your goal in finding the most competitive processing solution is to pay as close to wholesale as possible. In other words, to pay the lowest markup over cost. Processor markup is the only component of pricing that you can negotiate.

Cost, Markup, and Pricing Models

The key to a competitive credit card processing solution is to secure the lowest markup over wholesale cost. In order to do that, you’ll need to be able to see the wholesale cost and processor markup broken out separately. That’s where pricing model comes in.

There are two main types of pricing model, though each have variations.

The two types of pricing models are “interchange plus” (or “pass through”) and “tiered” or “bundled” pricing. The model your processor uses greatly affects whether you receive competitive pricing.

Interchange Plus Pricing

Interchange plus is by far the most transparent pricing model, and the one we require processors to use within CardFellow. It also sets the stage for competitive total costs, as it clearly breaks out cost and markup.

On interchange plus pricing, your processor will pass interchange and assessments to you and then add a small markup separately. A monthly processing statement will typically be several pages long, as it lists fees as individual line items.

However, it’s not required that a processor pass interchange and assessments to you at cost. If the processor “pads” those fees, you’ll end up paying more even though it looks like the processor has a competitive markup.

When looking to secure the lowest processing costs, interchange plus can help greatly, but it’s not a silver bullet. You’ll still need to ensure that interchange and assessments are passed to you at cost, and that you have a low markup. CardFellow makes that process easy by requiring (through a legal agreement) that processors pass interchange and assessments to you at cost. We’re also on hand to help you compare markups to determine the best solution for your practice.

Variations on interchange plus pricing include “subscription“ style or “0%” processing.

Tiered Pricing

Tiered pricing or bundled pricing is much more opaque. Rather than showing individual fees, the processor will “bundle” many different rates into “tiers.” Processors commonly use a three-tier model but can use more or fewer tiers.

On a three-tier model, the processor creates tiers for “qualified,” “mid-qualified,” and “non-qualified” transactions. It then decides which transactions will be charged according to which tier. The “qualified” tier has the lowest rate while the “non-qualified” rates are the highest.

With tiered pricing, your processor can change your transaction qualifications at any time, without notice to you. Transaction types that previously received lower “qualified” rates can be changed to receive higher “mid-qualified” or “non-qualified” rates at any time, leaving you paying more as your processor profits.

Despite what some processors may say, which transactions are “qualified” and “non-qualified” are NOT set by Visa or Mastercard. It’s completely up to your processor to decide to which tier it will route your transactions.

Variations on tiered pricing include “flat rate” processing.

We strongly suggest avoiding tiered pricing with qualified and not qualified rates. It’s never in your best interest, no matter what a smooth-talking salesperson might say.

Flat rate pricing can be a reasonable option, but for dental practices, it’s almost never the least costly. The primary exception is for newer practices that only accept a few thousand dollars/month in credit cards. Some businesses think that flat rate is lower cost because it looks simpler, but the reality is that you’re paying more for that simplicity.

A Note on Rates and Fees

It’s important to note that credit card processors set pricing and terms on a per-business basis. Theoretically, the same processor can offer different rates and fees to every dental practice it serves. That’s important, because it means that reviews and recommendations aren’t as helpful as they may be in aiding purchasing decisions for other types of products or services that are more consistent.

A colleague could get a great deal with Processor A and recommend them to your practice and then you could sign up with the same processor and get a not-so-great deal. This is also true of dental association recommendations, which we’ll address in depth a little later.

For now, just keep in mind that processors set pricing on a case-by-case basis, so finding the right solution is highly practice-specific.

That was the quick overview of rates, fees, and pricing models. For a more in-depth explanation, check out our comprehensive credit card processing guide.

What’s different about accepting credit cards at a dentist’s office?

There are several possible differences between card acceptance in a retail environment and accepting credit cards in a specialty environment such as your dental office. These differences include costs, equipment, and specialty needs such as HIPAA compliance and practice management integration.

Costs

On the cost side, dental practices have very few chargebacks and are considered low risk, which means your practice can enjoy lower costs than some other types of businesses. Additionally, dental practices can benefit from lower wholesale rates for some payments, like those made with American Express cards.

However, you’ll only benefit from those reduced wholesale costs if you’re on an interchange plus pricing model. On a tiered pricing model, your processor controls your cost by lumping wholesale and markup together, and might not pass along the savings from lower interchange.

Equipment

You may also have advantages when it comes to processing equipment. Unlike a retail store, your practice doesn’t need the features of a full POS system, like barcode scanners or scales. This allows you to save on equipment costs while still securely processing cards. You can choose a low-cost countertop credit card machine or opt for a virtual terminal that uses an existing computer with an internet connection.

We’ll talk more about these options a little later in this guide.

Specialty Considerations

Some dentists or orthodontists also look for the ability to integrate credit card payments with their practice management systems, such as Dentrix.

Additionally, dental practices frequently want the ability to accept cards that other establishments don’t need to (or can’t) accept, such as Health Savings Account (HSA) and Flexible Spending Account (FSA) cards.

Lastly, dental practices need to work with processors that are either HIPAA compliant or outside of HIPAA scope.

Credit Card Processing and HIPAA for Dentists

While many practices worry about HIPAA compliance when setting up credit card processing, the good news is that the basic functions of accepting cards usually falls outside of HIPAA compliance requirements.

For the purposes of HIPAA, there are two categories of business. The first is “covered entities,” meaning the business that directly handles patient info. In discussing processing for dentists, your practice is the covered entity.

The second is “business associates,” meaning third-party vendors that work with the covered entity, such as IT companies. In some cases, business associates are required to sign an agreement regarding responsibilities for safeguarding patient information.

Credit card processing companies are often exempt from the third-party business associate requirement, as they don’t have access to sensitive patient data and are considered to be performing normal banking functions. The Health and Human Services website explains the exemption in a paragraph specifically relating to credit card processing:

Exceptions to the Exception

However, it’s important to note that if your processing company performs functions for your practice beyond simple transaction processing, the above exemption may not apply. For example, if your processing company also handles invoicing and billing, accounting services, or patient management, you may need a business agreement with that company.

Securitymetrics, a leader in HIPAA compliance, explains that the distinction is whether the company is performing services on behalf of the patient or on behalf of your practice.

Ryan Marshall, Manager of HIPAA Fulfillment for Securitymetrics, says, “If the financial institution is processing a payment the consumer is making for, or related to health care or health plan premiums, they are not viewed as acting on behalf of the Covered Entity.” This statement means that they aren’t acting on behalf of your practice, but rather the patient.

Marshall continues, “Even though the payment is originating from the Covered Entity’s processing account, they are viewed as acting on behalf of the consumer and would not be a Business Associate. If the financial institution is operating an accounts payable or other back office system for a Covered Entity, they are viewed as acting on behalf of the Covered Entity and would be a Business Associate.”

Before choosing a processor, verify that the company is outside of HIPAA scope by only providing normal processing functions.

Personal Health Information

It’s imperative that your practice not include personal health information (PHI) or detailed patient information in communications with your processor. For example, if there is a “comments” or “notes” field in an online payment form or your virtual terminal, you should not use that space to include details of the patient’s visit, follow ups, or treatment.

Even an Explanation of Benefits should not go to a processing company, as they don’t need that information in order to successfully process a transaction for your practice.

Receipts

Another important note is that your processor cannot send a receipt to your patients using a non-secured method, such as text message or unencrypted email. While most processors will give you the option to provide paper receipts at the time of checkout, some companies, like Square, come with email receipts enabled by default.

When you sign up with a new processor, it’s important to check with them on how receipts will be provided, then double check default settings for any equipment and change those settings if necessary.

If you’re not sure whether a particular processor complies with HIPAA requirements, ask them directly. If the processor is unsure or can’t provide good answers, you may want to consider a company more familiar with HIPAA and processing for dental practices.

CardFellow works with several processors that can provide processing services in a HIPAA compliant manner.

PCI Compliance for Dental Practices

Payment Card Industry Data Security Standards, often abbreviated to PCI-DSS or just PCI, refers to security standards every business must meet when accepting credit cards.

PCI compliance is separate from HIPAA compliance, and both apply to dental practices. Some processors charge a monthly PCI fee while others do not. Regardless of whether the processor imposes a fee, the compliance requirements still apply.

PCI compliance is split into 6 requirement categories. For compliance, you must:

- Have a secure card processing network

- Protect all cardholder information and data

- Protect your systems against malware

- Put strong access control measures in place

- Monitor and test your networks

- Create and maintain an information Security Policy

Additionally, you’ll need to complete a yearly PCI compliance questionnaire. Your processor can help you with the questionnaire and with meeting compliance requirements.

Note that some processors impose a PCI non-compliance fee in the event that you don’t complete the questionnaire and validate PCI compliance. Most processors impose the fee for each month that you’re not compliant, making it an expensive reminder. However, the fee will stop once you become compliant. A non-compliance fee is avoidable, so it’s best not to waste money paying it when you can instead take steps to become compliant.

How do I take cards at my practice?

There are two pieces to accepting credit cards. You’ll need a processor (the company that handles the transaction) and a way to take credit cards.

Finding or Switching Processors

The easiest way to find a competitive credit card processor is to sign up for free at CardFellow. After entering basic information about your processing needs, you’ll receive instant quotes from leading processors, backed by CardFellow’s protections such as a lifetime rate lock and no cancellation fees.

You can also request a quote from any processor you want and CardFellow’s software will show you how it compares to the other offers you’ve received. This ensures you’re able to see how all pricing options stack up so you can make an informed decision and secure the most competitive option.

We work with several processors that can help you accept cards in a HIPAA-compliant manner. We’ve also been featured in an article in Dentistry IQ written by a Fellow of the American Association of Dental Office Managers (FAADOM) and are mentioned in industry sources such as Dental Town. Ask around! We’re confident you’ll hear good things about us from your colleagues.

If You’re Not Currently Accepting Cards…

Practices that aren’t currently accepting cards are in a great position to find a competitive credit card processor. Following the tips in this guide can help you avoid some of the most common pitfalls, such as signing up with processors that utilize tiered pricing.

Be sure to read our articles on processing and don’t get sucked in by reviews.

If You’re Currently Accepting Cards…

Practices that already accept cards will first need to check contract terms. Is there a cancellation fee to end your contract? In some cases, we find that practices are overpaying by so much that switching to a more competitive processor still saves money even after paying a cancellation fee.

Be aware that some processors will offer to “beat” or “match” rates if you find a better quote. However, the “match” doesn’t usually last long. Be sure to read our article about promises of money if a processor can’t beat your rates.

Accepting Health Savings Account and Flexible Spending Account Cards

Every business that sets up a merchant account to accept credit cards will be assigned a merchant category code (MCC), designating the type of business. Only certain MCCs are eligible for HSA / FSA acceptance. Both specialists and generalists in the dental profession can be set up to accept HSA /FSA cards. If you’re looking to accept these cards, you’ll need to be set up under one of the following MCCs:

Note that some HSA and FSA cards still have limits on types of allowed purchases, even if you’re set up with the correct MCC. Your patient should always check with their plan prior to treatment to determine if a particular treatment or service will be covered.

Additionally, HSA and FSA card will be declined just like a regular card if your patient doesn’t have the funds available to cover the transaction.

Choosing Equipment

Virtual Terminal

A virtual terminal is a method of accepting credit cards using a computer instead of a dedicated credit card processing machine. With a virtual terminal, you’ll enter credit card details into a secure online form provided by your processor.

Cards can be hand-keyed or swiped using optional card readers that connect via USB port or Bluetooth, such as the Magtek EMV reader, pictured.

In most cases, swiping cards is faster, more secure, and results in lower processing fees than manually entering cards.

Virtual terminals are a great option for practices that don’t need or want dedicated credit card machines.

Credit Card Equipment

If you’d prefer to use traditional credit card equipment, such as countertop machines and PIN pads, you can accept credit cards using any equipment that your processor supports.

If you’re choosing a processor through CardFellow, you’ll be able to easily browse supported equipment and add it to your quote. You can view available credit card machines in CardFellow’s product directory.

We recommend choosing universal equipment, such as Verifone, Ingenico, or PAX terminals, so that you’ll have the flexibility to change processors in the future without having to purchase a new machine.

Integrated Solution

For taking credit cards using an integrated solution, such as Dentrix or Open Dental, you’ll need to know if the equipment or software requires a specific processor. If so, you’ll need to have a merchant account with that processor in order to accept credit and debit cards through that system. We’ll look at the processing options through a few popular systems a little later.

Credit Cards on File

Some practices prefer to keep credit cards on file to charge as needed. While this practice is HIPAA compliant when done correctly, you should still take steps to ensure that patients are aware of transactions before they’re processed.

Additionally, keeping credit cards on file does not mean you can simply write down the patients’ card details or keep them in a document on your computer. Rather, you’ll need to store the information securely, meeting PCI compliance requirements.

Fortunately, many credit card processors offer secure “card vaults” that can help you securely store cards while also staying on the right side of PCI requirements. Card vaults commonly utilize encryption and tokenization, masking the card details but allowing you to process the cards as needed

Practice Management Solution

Many dental practices currently use or plan to use a practice management solution to help with office needs. The specific features available vary by system, but often include maintaining patient files, charting, and processing insurance claims. Some systems also offer integrated credit card processing or full billing solutions. In this section, we’ll examine your payment processing options for 3 popular systems:

Dentrix

The market leader, Dentrix is the practice management solution that more than 35,000 dental offices use regularly. If your office is one of them, you may be wondering if you should accept credit cards through Dentrix.

For most offices, the answer is, “It depends.”

Is taking credit cards with Dentrix right for my practice?

If you’re a dentist or orthodontist who already uses Dentrix software for practice management and patient records, you can choose to accept credit cards through the system or externally.

Accepting cards Through Dentrix

To accept credit cards through Dentrix, your office will go through the Dentrix Pay service or will need to open a merchant account with a company called PowerPay, who processes through another company called Moneris Solutions.

There are no other options for processing credit cards directly through Dentrix.

While working with PowerPay will allow you to integrate credit card processing with your Dentrix system, be aware that limiting yourself to one specific processor often results in higher costs to accept credit cards. If low processing costs are a priority for your dental practice, you don’t want to use PowerPay for Dentrix.

Instead, you should weigh the difference in cost and convenience using a a non-integrated credit card processing solution.

Limitations of PowerPay for Dentrix

Accepting cards with PowerPay for Dentrix is not for you if:

- Keeping processing costs low is a priority

- You accept or want to accept American Express or Discover

If low-cost credit card processing is your priority, accepting credit cards with PowerPay for Dentrix is not your best option. The reason is that you have no bargaining power to negotiate competitive pricing. When you get quotes from multiple processors, you have the ability to choose the lowest option. If you choose a processor through CardFellow, you’ll also benefit from a lifetime rate lock, meaning the markup charged by your processor will never go up.

If you accept or want to accept American Express or Discover Cards, PowerPay for Dentrix isn’t the right fit. PowerPay allows practices to accept Visa and MasterCard credit cards, flexible spending account cards, and debit cards processed as Visa cards.

Benefits of PowerPay for Dentrix

With PowerPay or Dentrix Pay, payments are automatically posted to the Dentrix ledger instead of requiring manual entry. Additionally, the companies securely encrypt and store patient credit card information so that you can set up recurring payments or process payments after insurance reimbursements.

You’ll enter patient and card details, and then set the recurrence schedule. The system then stores the card securely for recurring payments.

However, it’s worth noting that secure encryption technology and recurring billing options are also available with other processors, so that is not a function unique to the Dentrix system. You would still be able to set up secure recurring billing externally using a virtual terminal.

PowerPay for Dentrix promises competitive transaction fees and a rate match guarantee, but promising to match rates isn’t a sign of good pricing.

If you absolutely need transaction details to sync automatically, Dentrix Pay or PowerPay for Dentrix is a good choice. However, you can save money and accept more types of cards by working with other processors.

External Processing

Just because PowerPay is the only processor that directly integrates with Dentrix doesn’t mean you can’t use Dentrix and also use an external system to process credit cards. You would still be able to take cards with a virtual terminal or credit card machine.

Limitations of External Processing

As mentioned above, if you wanted to include transaction and payment details with patients’ files in Dentrix, you would need to enter or import that information manually.

Essentially, you would open a merchant account with the processor of your choice, use a credit card machine or virtual terminal to complete the transaction, and manually make any notes (such as paid status) in the patient’s file in Dentrix. It will be lower cost, but adds an extra step.

Benefits of External Processing

The primary benefit to using a non-integrated solution is cost savings. When a processor has an exclusive relationship with a practice management system, they have no competition and thus no incentive to negotiate with you or to lower prices.

When you choose a processor from a larger pool, you have competitive leverage. Those processors must compete with each other to earn your business, which results in lower costs. The ultimate advantage comes in the form of a blind auction, where processors place their best possible quotes for you without knowing what other processors have bid. That’s the format we use at CardFellow to help our clients secure the lowest possible processing costs.

Additionally, external processing allows you to accept a wider range of cards. If you have a lot of patients that wish to use American Express, for example, you’ll better serve them by accepting their preferred card. American Express also has special pricing for healthcare professionals, which keeps costs down.

Dentrix Summary

Whether integrating credit card payments with Dentrix is right for you depends on your specific needs and priorities. To determine if PowerPay or an external processing solution is right for your dental practice, consider the following:

- Is saving money and cutting expenses a top priority?

- Do you want to accept American Express and Discover cards

- Do you need transactions to automatically sync with your patient records or can staff enter the payments?

If cost to accept credit cards is not a factor for your practice, accepting credit cards through the Dentrix integration is a good idea.

If securing low costs to accept credit cards is important to your practice, or if you want to take Amex and Discover, you’ll want to accept credit cards through a non-integrated method. With this method, you can still use Dentrix for other patient functions.

Open Dental

Unfortunately, like Dentrix, Open Dental’s options for integrated credit card processing are very limited. Furthermore, a statement on the company’s website indicates that they are not pursuing any additional processing relationships.

The statement reads, “If you are a representative from a payment processing company, and you wish to directly integrate your software with Open Dental, the answer is currently “no.”

Is taking credit cards with Open Dental right for my practice?

The three companies you can use with Open Dental are X-Charge (a subsidiary of Open Edge), Pay Simple, and PayConnect.

Open Dental’s website references the ability to securely store cards for recurring use, which is available with either processor. Open Dental states that the companies use a process called tokenization, where sensitive credit card details are replaced by a “token” that you can save. Cards stored through tokens will not show card numbers.

However, it’s worth noting that many processors offer tokenization and can provide a secure card storage vault.

Curiously, Open Dental also has an option that allows you to store untokenized, unencrypted card details – a big security no-no. The company’s website includes the statement: “Always uncheck ‘Allow storing credit card numbers (this is a security risk).’ When enabled, this preference will store credit cards in Open Dental without tokens. Card numbers will not be masked and are not encrypted in the database. This is a security risk, violates credit card security guidelines, and is not recommended.”

Given that it’s a security risk, violates card security guidelines, and isn’t recommended, we’re not sure why Open Dental allows that option at all. It seems that the company simultaneously wants to give your practice a way to non-securely store cards while absolving themselves of liability if you do.

We strongly recommend not storing cards unless you do so in a secure manner. Utilizing tokenization and a secure card vault from an external processor are secure options.

As with Dentrix, if you chose to use a non-integrated processor, you would not use the payment functions within Open Dental but rather a credit card machine or virtual terminal.

Open Dental and PCI Compliance

Open Dental’s website includes a few odd statements about PCI compliance, most notably that, “Many merchants may determine that the cost of the non-compliance fees are less than the cost of compliance” and, “The non-compliance fees are essentially a slush fund that the industry uses to pay out fraud claims.”

PCI compliance should not be cost-prohibitive. Additionally, this statement does not take into account the costs of a data breach, which can be significant. A monthly non-compliance fee will be the least of your costs if your data is compromised and you were determined to be non-compliant. You could be on the hook for tens of thousands of dollars (or more) depending on the extent of the breach, have to pay card replacement costs, and more. Even if a processor were to pay a fraud claim from a “slush fund” of non-compliance fees, the processor can still pursue your practice for costs associated with data breaches and fraud.

While some practices may decide to take that risk, we don’t recommend a cavalier attitude to credit card security and would not suggest foregoing compliance.

To make matters worse, PCI non-compliance fees are often assessed for every month that you’re not compliant. That means that you’ll pay an unnecessary monthly penalty fee that could be avoided by achieving compliance. If you’re looking to keep costs down, it doesn’t make sense to pay an avoidable monthly fee.

Your processor should be able to assist you in ensuring compliance.

Benefits of Integrated Processing with Open Dental

The benefit of using X-Charge, Pay Simple, or PayConnect is that your patient management and payment functions are all completed through one system. You’ll be able to accept cards directly within Open Dental and won’t need to do any manual ledger entry.

Limitations of Integrated Processing with Open Dental

As with Dentrix, the main limitation is your lack of choice in processors. Since you can only pick three, you won’t be able to shop around for the most competitive pricing and you’ll have limited room for negotiation.

Open Dental Summary

If your main priority is low cost, consider an external processor for accepting payments and use Open Dental only as your patient management system.

If costs are not a factor, integrating through Open Dental is convenient.

Carestream Dental

While not as well-known as Dentrix, Carestream Dental offers a full practice management solution that includes dental imaging, electronic health records, patient scheduling, billing, and more. The system also allows for integrated credit card processing, though, again, only through one processor.

Credit Card Processing with Carestream Dental

Carestream Dental’s integrated credit card processing is through a company called TSYS. While TSYS is a member of CardFellow’s marketplace and places certified quotes through our system, Carestream Dental requires that you go through its channel to get set up for integrated processing and not through alternate sales channels like CardFellow. In many cases, companies that have set up revenue shares and affiliate partnerships require that sort of structure. It benefits them, but doesn’t help you.

Unfortunately, it also means that you will not be eligible for the CardFellow protections that accompany TSYS quotes in our marketplace (such as our lifetime rate lock) if you choose the integrated processing method for Carestream.

The integrated payment processing option for Carestream Dental offers several helpful features, including recurring billing so that you can set up a payment plan for patients. You can also accept one-time payments, such as copays.

TSYS offers this video about its integration with Carestream Dental:

External Processing

If you’d prefer external processing, you can still do that. External processing affords you the opportunity to negotiate the lowest possible rates and to secure added protections such as lifetime rate locks and no cancellation fees. You can start the search for the right processor by signing up for a free account to compare pricing.

As with other systems, if you choose an external processing solution, it will not automatically update payment records in your patient files. However, you can manually record payments in the practice management system.

Carestream Integrated vs. Non-Integrated Processing

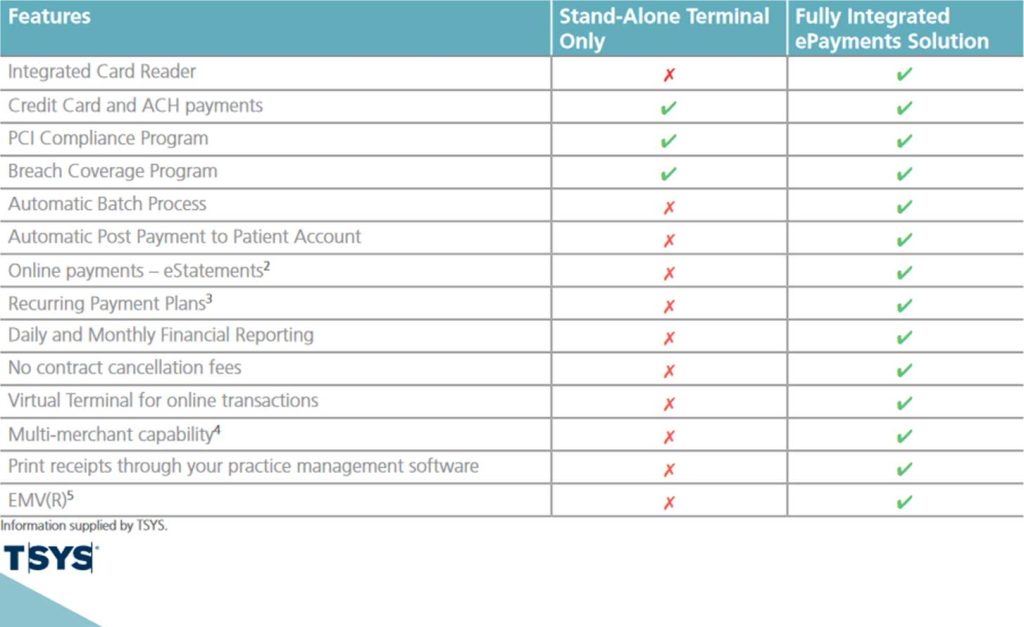

This chart from Carestream Dental’s website shows the capabilities for integrated and non-integrated processing.

However, some of the X’s in the “stand-alone terminal” column don’t provide the full picture. For example, “virtual terminal for online transactions” is marked with an X. That’s technically true – countertop credit card terminals are not virtual terminals. However, almost every processor can set you up with a virtual terminal.

Additionally, “recurring payment plans” receives an X. Once again, that’s only true in the most technical sense – countertop / stand-alone terminals can’t handle recurring payments, but virtual terminals can.

The column is carefully constructed to highlight the features a stand-alone terminal cannot support without mentioning that a virtual terminal solution would provide those functions.

Carestream Summary

As with other practice management systems, if low cost is your highest priority, select a non-integrated processor and use a countertop credit card machine or a virtual terminal to process payments.

If you don’t mind paying more, integrated processing offers the convenience of automatically syncing payments to patient files.

Contact us for assistance evaluating your credit card processing options!

Tips for Evaluating Recommendations

You don’t need to immediately disregard recommendations from dental associations, but take them with a grain of salt. Remember, credit card processors set pricing and terms individually for each practice, so what’s right for another office may not be right for yours.

Here are some things to consider when evaluating recommendations from dental associations.

Know the Motivation for the Recommendation

Why is the Association recommending a specific processor? Do they receive money if you sign up? That type of partnership is not inherently bad – in fact, that’s how we make money at CardFellow – but it’s important to know if and how the recommendation benefits the organization.

In an ideal world, professional associations would only recommend processing companies to their members if the recommendation provides as much or more benefit to the member. Unfortunately, in reality, many credit card processing recommendations end up benefitting the association (and the processor) more than you.

Closely Examine Special Pricing

Some processors will offer “special pricing” to members of a professional organization. While it may be lower than what they offer to non-members, that doesn’t automatically guarantee it’s competitive. Consider the following:

It can be difficult to easily compare quotes when looking at applications or pricing schedules, so if you need help, try CardFellow’s free quote comparison tool and give us a call. We’ll walk you through it and answer questions as your independent processing experts.

Recommendation from other Practices

If the recommendation comes from a colleague or other practice instead of an association, it’s still important to check out the details. Any number of factors could affect whether you receive a good deal with a processor, and a recommendation from a colleague doesn’t mean you’ll get the exact same deal. For example, a colleague may accept cards differently than you do, may have higher volume, or accept a greater amount of debit cards, all of which can have an effect on the overall costs.

Conclusion and Resources

You made it! Now that you’re an expert on credit card processing for your dental practice, you’re in a great position to get the right solution for your business. Come see just how competitive quotes through CardFellow’s marketplace really are.

Sign up for an account to see pricing instantly – it’s free, and only takes 2 minutes.

Try Cardfellow Now!