Two businesses have filed a lawsuit against Colorado-based Mercury Payment Systems, claiming the company adds hidden fees when charging businesses for credit card processing.

If that sounds familiar, it’s because it’s the same thing that Mercury was sued for by Heartland Payment Systems in 2014.

Note: Also in 2014, Mercury Payments was acquired by Vantiv, which has itself since been acquired by Worldpay. The practices that Mercury was allegedly engaged in and sued for may not be the same practices that are currently utilized by Vantiv or Worldpay. We’re leaving this article for historical context, but it may not be relevant to current Mercury customers.

Archer’s Barbeque v. Mercury Payment Systems

The lawsuit, filed by Archer’s Barbeque and WokChow Development, claims that Mercury Payment Systems adds fees to a business’s processing bill while disguising them as either interchange or assessment fees that are required.

The case was terminated in 2015 with little information publicly available.

Heartland Payment Systems v. Mercury Payment Systems

In 2014, Heartland Payment Systems sued Mercury Payment Systems for “deceptive pricing.” Heartland claims Mercury utilized deceptive tactics to steal clients. The federal lawsuit accused Mercury Payment Systems of false advertising and unfair competition.

Mercury Payment Systems’ Reply

In response to the Heartland Payment Systems lawsuit, Mercury Payment Systems said that the charges are erroneous and stated that they would fight the lawsuit. Mercury has not made a public comment on the Archer’s Barbeque lawsuit.

Are these lawsuits accurate?

The lawsuit brought by Heartland Payment Systems may have the feel of a fight between bitter competitors, but in our experience with Mercury statements, the arguments have some validity. While we can’t speculate on the legality of Mercury Payment Systems’ practices, we can confirm that we’ve seen misleading and deceptive pricing when reviewing Mercury statements for CardFellow clients.

How Mercury Payment Systems Adds Hidden Fees

In the statements we’ve reviewed (screenshots below) the way that Mercury added fees was to increase the cost of assessments required by the card brands (Visa, Mastercard, and Discover.) That means that Mercury charged a fee that’s part of their true cost, but instead of charging only as much as they had to, they added more money to the fee. Basically, they inflated the true cost.

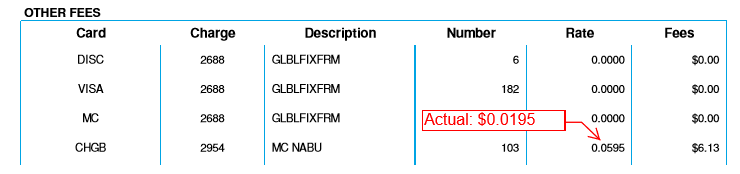

In the example below, the assessment called MC NABU is an assessment charge from MasterCard. Mercury Payment Systems charged this business $0.0595. However, MasterCard’s charge is $0.0195. Mercury added 4 cents to keep as their profit, but disguised it as a Mastercard assessment charge.

4 cents might not seem like a lot, but these assessment fees are charged for every transaction. That means Mercury Payment Systems charged businesses more than disclosed on every sale.

Note: CardFellow recently reviewed an October 2015 application for processing through Mercury Payment Systems, and the assessment fees listed are correct. Mercury may now be charging assessments at actual cost.

Do other processors add hidden fees?

Unfortunately, opaque and deceptive pricing is still a common practice in the processing industry. Inflating assessments is only one way that processors can charge you more. You can overpay on a number of pricing models and in a variety of ways. Unless you’re a processing expert, it’s easy to miss small fees that add up quickly. The Archer’s Barbeque lawsuit points out that fees are often difficult for businesses to find since they can be tiny amounts that only add up over time, or are easily disguised as legitimate fees.

I’m on an interchange-plus model, so I’m safe, right?

Not necessarily.

You may think that interchange-plus pricing is the ticket to low cost. But Mercury Payment Systems technically offers interchange-plus pricing, illustrating that by itself, interchange-plus it not a silver bullet. Interchange-plus pricing is simply a model that separates interchange and assessments from the processor’s markup. There’s no guarantee that you’re getting the interchange and assessments at the actual cost. In fact, you can get gouged on interchange-plus just as easily as other pricing models if you’re not careful. What you really need is true pass-through pricing, where your processor passes fees to you at cost.

Avoid Being Overcharged

The easiest way to avoid being overcharged is to create a free CardFellow account to find a processor that offers true pass-through pricing and is bound by CardFellow’s legal agreement to keep your rate locked for life.

And just to be sure you’re getting a fair deal, we’ll monitor your account for you to make sure there’s nothing fishy going on. We’ll catch any problems so you can focus on running your business.

I use Mercury Payment Systems. How do I know if I’m paying too much?

If you use Mercury Payment Systems and are worried you might be paying too much for processing, create a free profile at CardFellow to receive instant quotes and then send us your statement. We’re not a processor, so we don’t try to sell you on a particular solution. We’ll check out your costs to see if you’re overpaying, and educate you so that you can make informed choices about what’s best for your business.