You know the drill. Your monthly processing statement comes in, and your processor is raising your rates. How do you stop it?

Credit card processing isn’t cheap. But it doesn’t have to be as expensive as many business owners think. In this article, I’ll cover the different types of price increases, which ones are avoidable, and how to stop them.

Types of Price Increases

When your processing rates go up, it could be because Visa and Mastercard raised rates, your processor raised rates, or both. When Visa and Mastercard raise rates, there’s nothing you (or your processor) can do to lower them again. However, processor rate increases are avoidable. There are two ways to avoid them.

The Easy Way

Join CardFellow’s wholesale credit card processing club. Our members enjoy contractually-secured rate locks on the processor’s markup, so your processor can’t increase rates over time. We stick around to monitor your pricing and ensure you pay as little as possible for processing.

Did I mention membership is free? CardFellow receives a commission from processors when you choose one through our system; you never pay us directly.

Simply put: Once you’ve secured a low processor’s markup through CardFellow, you won’t have to deal with rate increases from your processor again.

The Hard Way

Learn about the different ways that processors may apply price increases, and watch your statements. You’ll need to compare the interchange rates listed on your monthly statement to the published interchange rates on Visa and Mastercard’s websites in order to determine if interchange is passed to you at true cost. You’ll also need to be able to determine price increases that are in your processor’s control and ones that aren’t, and be prepared to argue against the avoidable increases with your processor.

The rest of this article will cover what you’ll need to know and do if you want to do this the hard way.

Determine the Source of the Increase

In credit card processing, an increase can be the result of a few different things, some of which are in your processors control and some of which aren’t. You’ll need to first determine if the increase was your processor’s doing, or Visa / Mastercard’s.

Visa and Mastercard may increase interchange rates or assessment fees. If they do, there’s nothing your processor can do to lower those fees. (However, your processor could add to it, making it a greater increase than necessary. I’ll address that later in this article.)

If Visa and Mastercard raised fees, you’ll need to confirm that you’re receiving the increases at cost, without additional charges. To do that, you can compare your interchange rates from a monthly statement to Visa’s and Mastercard’s published interchange rates. Keep in mind that there’s no standardization to interchange category descriptions in processing statements. What Visa or Mastercard call an interchange category might not be how your processor lists it on your statement. You can check CardFellow’s blog for specific interchange categories and view our list of known aliases for each category.

CardFellow members – we’ll do this for you. Processors within CardFellow are required to pass interchange fees to you at true cost, but we keep an eye on things to make sure that they do. Log in to your member dashboard and upload a recent statement for an audit.

Is it true that my processor didn’t raise the rates, Visa and Mastercard did?

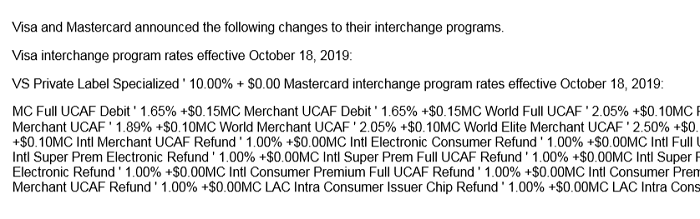

Processors may tell you that your processing costs went up because Visa and Mastercard raised pricing.

This is sometimes the case, but not always. Keep in mind that your processor will include notices about price icnreases on your monthly statement. In some cases, the notice will simply state an impending rate change. In other cases, it may list the interchange categories and rates that changed. For example, here’s a statement that lists interchange rate increases from the card brands that occurred in October 2019. (Statement has been enlarged, not all categories shown.)

However, even when Visa and Mastercard do raise rates, processors may raise your pricing more than Visa / Mastercard did.

To understand how that happens, it’s important to understand the different rates and fees that make up your total processing cost.

Parts of Processing Fees

We’ve covered the components of processing costs thoroughly in our article about credit card processing rates and fees, but for a quick recap:

Interchange: Typically, the largest part of processing costs. Interchange fees go to the banks that issue cards to your customers.

Assessments: Fees that go to the card brands (Visa, Mastercard) themselves.

Markup: The rates and fees that go to your processor.

When your processor charges you for processing, it includes all three of these components in one way or another. It may list them separately or bundle them together, but all three pieces are always part of the total cost.

There are hundreds of different interchange “categories” but the rates are almost always a percentage and a cents fee. (E.g. 1.65% + $0.10.) Several assessments can apply to a single transaction. Assessments include both percentages and cents fees.

Your processor doesn’t control interchange or assessments. If Visa decides to raise its interchange fees, your processor can’t do anything about that. The processor will pass along the fee increase to you.

The processor only controls their markup, which is in addition to interchange and assessments. They can charge a percentage, cents fees, monthly fees, or some combination. Most processors charge a combination, but there are exceptions. (For example, subscription-style processors like Payment Depot charge 0% markup, but have higher cents fees and monthly “subscription” fees.)

So, when Visa or Mastercard raise the interchange rates or assessment fees, your costs do go up and your processor doesn’t control that. However, what the processor does control is whether it passes the increase to you at cost or if it “pads” the fee, and whether it raises its own part of the rates, i.e. the markup, at the same time.

Additionally, your processor can raise your markup at any point even if Visa and Mastercard don’t raise their rates.

Let’s take a look at how price increases happen on different pricing models.

Interchange Plus Price Increases

On interchange plus pricing, the processor will pass along the interchange cost and the assessments, adding their markup on top of that. Because of this, interchange plus monthly statements are often long and look confusing, but it’s the most transparent way to show your processing charges.

With this type of pricing, you can see which interchange categories applied, and the costs you were charged for those categories.

Legitimate Interchange Rate Increases vs. Padded Interchange

With true pass-through interchange plus pricing, your processor will charge you the “true” cost of interchange and assessments. If you were to compare your interchange charges from a monthly statement to the published interchange charges, they would match.

If Visa or Mastercard raise interchange rates, those new rates will be reflected in their published interchange tables.

However, if the interchange rates don’t match your monthly statement’s interchange charges, your processor is “padding” the interchange fees set by Visa and Mastercard. That’s one way a processor can raise your rates while pretending the cost is out of their control. Remember, processors can’t lower the interchange rates, but they can raise them. If they simply make those interchange rates higher, they can say interchange is out of their control without telling you that they padded the true cost of the interchange fee.

Let’s look at this with examples.

Visa’s rate for a basic consumer credit card is 1.65% + 10 cents per transaction. If this interchange category is listed on your monthly statement with higher percentages or cents than that, the processor padded the interchange fee.

It can be tricky to spot this sort of thing on your own. If you suspect your processor is padding interchange, I’d strongly suggest confirming it with an expert and then switching processors.

Tiered Price Increases

Also called “bundled” pricing, tiered pricing is a model in which processors create “tiers” and then route different transactions to different tiers. A common bundled pricing model uses three tiers – called qualified, mid-qualified, and non-qualified – but processors can use more or fewer tiers at their discretion. The processor will apply a rate to each tier. Then, the processor will charge multiple interchange categories under one of their tiers. This means that the interchange rates that Visa and Mastercard set are essentially irrelevant to you, in a bad way. If Visa’s interchange rate for a particular card is 1.65%, but your processor decides to route it to a tier that it sets at 2.25%, you pay the 2.25%, not 1.65%.

Additionally, processors can change which transactions route to which tier, and they can adjust the rates for each tier as often as they like. Whether Mastercard or Visa raised a rate or not, the processor can decide to move some of your transactions to a higher mid-qualified or non-qualified rate whenever they feel like it.

When it comes to rate increases, if you’re on tiered pricing, it’s going to be a neverending shell game. Rather than trying to find out where the increase came from and if it can be reversed, you’ll save yourself time (and money) by switching to a more competitive and transparent interchange plus processor.

Flat Rate Price Increases

Technically, flat rate pricing is a form of tiered pricing, but for the purposes of rate increases, it’s different enough to warrant its own section.

Flat rate pricing is the kind offered by companies like Square. There’s one rate for swiped transactions and one rate for keyed transactions. With flat rate, all three components of cost (interchange, assessments, and markup) are lumped together. There’s no way to determine what portion is paying interchange, what portion is paying assessments, and what portion goes to markup.

This also means that it’s impossible to separate interchange price increases or markup price increases. Flat rate processing statements don’t show interchange detail, meaning you won’t know which interchange categories applied to your transactions. Since the costs are lumped together, only the processing company knows how much they make vs. how much goes to interchange and assessments. It also means that they have to price high enough to cover more expensive interchange categories.

The bottom line: if a flat rate processor increases your rates, there’s no real way to determine if they’re increasing them because of interchange increases, because they wanted to make more money through a higher markup, or both.

Things like this are why we always point out that flat rate is the least transparent pricing model. Without the ability to see interchange detail, it’s very difficult to see what you’re paying to whom. Speaking of flat rate…

Square Rate Increase

In November 2019, Square announced that it was changing its rates from a flat 2.75% to 2.6% with a 10-cent transaction fee. Understandably, many business owners were upset at the change, as it resulted in a large increase in processing costs for smaller transactions. Many people in the industry saw it as inevitable, as Square’s original pricing was a money-loser for the processor.

What can I do about Square raising my rates?

If Square raised your rates, the first thing to do is determine whether you fit the profile of a business that will pay less when using a flat rate processor.

You’ll typically pay less with a flat rate processor if:

- Your average transaction is low (~$10)

-OR-

- You process $5,000/month or less in credit cards.

You’ll typically pay more when using flat rate if:

- Your average transaction is over $10

-AND-

- You process more than $5,000/month in credit cards.

When Flat Rate is a Good Fit

If you fit the first description of a business that should use flat rate, your options are unfortunately more limited. Believe it or not, Square was actually losing money on many small transactions. Consumers use debit cards more often than credit for small transactions, and with the current pricing for some debit transactions, Square’s 2.75% fee wasn’t covering all of the costs of interchange / assessments for debit.

Unfortunately, businesses with small transactions are a big chunk of Square’s business. That includes coffee shops, bakeries, and others with low individual sales.

Square adjusted its pricing model as a way to plug its money leak. In other words, it wanted to stop losing money on small transactions, and the only way to do that was to raise prices. The reason that you won’t easily be able to find a cheaper replacement is that other processors aren’t in the habit of losing money, either. Previously, other processors were much higher than Square for small transactions. Now, they’re about the same. That’s not because those other processors were necessarily overcharging – it’s because Square was undercharging.

If you’re with Square and want to switch, just be aware that you’re unlikely to find the same low pricing you had before.

When Flat Rate Isn’t a Good Fit

But let’s say you don’t fit into the description of a good candidate for flat rate processing. Perhaps you just chose Square when you started out because it seemed easy, or because someone recommended it. However, if your average transactions are higher than $10 and you’re processing more than $5,000/month in cards, chances are you can do better than Square. So, how do you do that?

Join a wholesale processing club.

Wholesale credit card processing clubs, like CardFellow, let you take advantage of strength in numbers. Members get access to exclusive low rates, plus a range of membership benefits like a lifetime rate lock. That’s right – you won’t have to deal with rate hikes.

You’ll also get true pass-through pricing (no padded interchange!) and ongoing statement monitoring to ensure you pay as little as possible to process cards.

Or, once again, you can do it the hard way – call up processors, get quotes in writing, try to compare them despite the different formats, and then keep an eye on the rates and fees yourself. If you want to go that route, I strongly recommend reading our credit card processing guide first.

Ending Price Increases

You can’t completely eliminate increases in processing costs. When Visa and Mastercard raise rates, your costs will go up. However, what you CAN do is make sure that your costs only go up as much as Visa and Mastercard say. In other words, you can eliminate the unnecessary processor markup increases and sneaky interchange padding.

How? Secure true pass-through pricing and a lifetime rate lock.

While it’s not common in the open market, it’s a core benefit of CardFellow membership. In our contracts with processors, we require a lock on the processor’s markup for as long as you’re with the processor through us. Even better, we stick around to monitor your statements and ensure you’re paying as little as possible for processing.

70% – 80% of CardFellow clients find us after they’ve begun processing and are unhappy with their current processor. Rate increases and other negative experiences lead them to seek a better processing solution. If you’re in the same boat, you can stop the frustration of constant rate hikes and shopping for processing once and for all.

Get your free CardFellow membership today!